What is private credit?

Private credit is lending done by non-bank funds directly to mid-sized companies, outside of public bond markets and bank syndicated loans, with the lender holding the loan to maturity in exchange for higher all-in yields than comparable public debt. The borrower is usually a private-equity-backed company with $10 million to $1 billion in revenue; the lender is a fund organized as a limited partnership, a business development company, or an interval fund (Federal Reserve FEDS Notes, August 2024).

The asset class includes several sub-strategies: direct lending (the largest, around 80% of the market), mezzanine (subordinated debt with equity-like upside), distressed credit (loans to companies in or near default), and opportunistic credit (specialized situations like asset-based lending or rescue financing). Most of the recent growth and most of the regulatory attention is on direct lending.

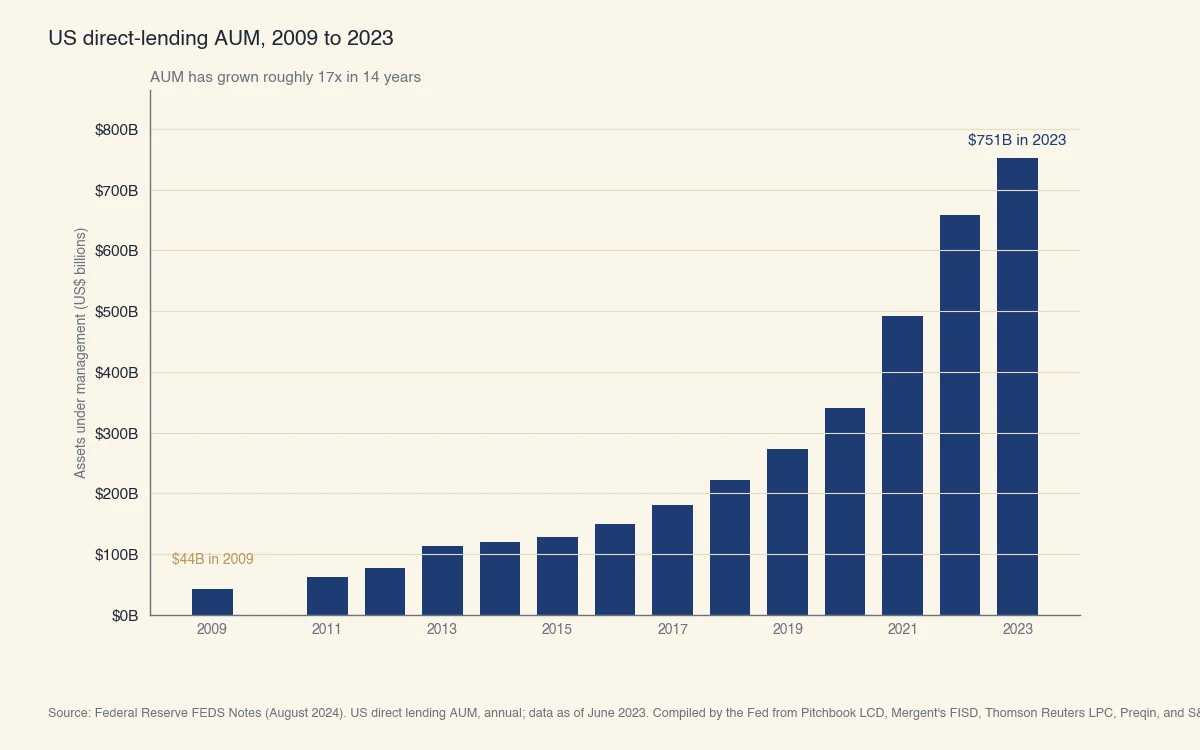

Why the asset class matters: US direct-lending AUM has grown from $44 billion in 2009 to $751 billion as of mid-2023, a 17-fold expansion in 14 years. Globally, including dry powder waiting to be deployed, private credit reached approximately $2.1 trillion in 2023 according to data summarized in the IMF Global Financial Stability Report (IMF GFSR April 2024). That is roughly the size of the US high-yield bond market and a meaningful share of all corporate debt.

What does "private" mean here?

The term "private" describes how the loan is originated and traded, not who borrows. The loan is negotiated bilaterally between a single fund and a single borrower, never registered with the SEC, and rarely sold to third parties before maturity. There is no daily mark-to-market price the way there is for public bonds. Most private credit loans never appear on a public exchange and are reported only in aggregate by data providers.

How does a private credit fund work?

A private credit fund pools capital from institutional limited partners on a 7-to-10-year lock-up, deploys it into 30 to 100 senior secured floating-rate loans, and returns interest income plus principal repayments over the life of the fund. The general partner manages the portfolio and earns a management fee (typically 1% to 1.5% of committed capital) plus a performance fee on returns above a hurdle rate (typically 6% to 8%).

The fund's economics are simple in outline:

| Step | What happens | Who is involved |

|---|---|---|

| 1. Capital raise | Fund manager solicits commitments from pensions, insurers, endowments, family offices | GP + LPs |

| 2. Origination | PE sponsor brings a deal; fund underwrites, structures terms, signs the loan agreement | Fund + sponsor + borrower |

| 3. Funding | Fund draws committed capital from LPs as deals close | Fund + LPs |

| 4. Servicing | Fund collects monthly interest, monitors covenants, reports to LPs | Fund + borrower |

| 5. Repayment / refinancing | Borrower repays at maturity (typically 5-7 years) or refinances earlier | Fund + borrower |

| 6. Distribution | Principal and interest flow back to LPs net of fees | Fund + LPs |

The covenants and structure usually look like this: a senior secured first-lien position, floating rate (usually SOFR + 5% to 7%), 5-to-7-year term, mid-single-digit annual amortization, and one or two financial-maintenance covenants tested quarterly. Compared to a syndicated leveraged loan, private credit loans are typically smaller (median around $100 million), more bespoke, and more covenant-heavy.

Who invests in private credit funds?

The investor base is heavily institutional. The IMF GFSR April 2024 reports that pensions, insurance companies, and sovereign wealth funds together account for the majority of private credit limited-partner commitments globally, with high-net-worth and family offices making up most of the rest. Retail access exists through business development companies (BDCs), which are publicly-traded closed-end funds regulated under the Investment Company Act of 1940 (SEC Investor Bulletin). Newer interval funds and registered closed-end funds offer a middle path between fully private LP funds and publicly-traded BDCs.

How big is the private credit market and why is it growing?

US direct-lending AUM grew from $44 billion in 2009 to $751 billion by mid-2023, a 17-fold expansion that absorbed much of the mid-market lending business banks pulled back from after the 2008 financial crisis. The growth concentrated in three windows: the post-2010 buildout, the 2020-2021 surge as PE deal volume rebounded, and the 2022-2023 acceleration when higher base rates made floating-rate loans dramatically more attractive on a relative basis.

Source: Federal Reserve FEDS Notes (August 2024). US direct lending AUM, annual; data as of June 2023. Compiled by the Fed from Pitchbook LCD, Mergent's FISD, Thomson Reuters LPC, Preqin, and S&P Capital IQ.

Three forces drove the rise:

- Bank retreat from mid-market lending. After the 2008 financial crisis, Basel III and Dodd-Frank capital rules made mid-market floating-rate lending uneconomic for many banks. Banks shifted toward larger, syndicated, investment-grade exposures and ceded the mid-market to non-bank lenders.

- Search for yield with low public correlation. Pension and insurance allocators, facing low public-market yields through 2010-2021, expanded private-credit allocations from low single digits to 5% to 10% of total assets. Private credit's floating-rate structure also offered protection against rising rates.

- Speed and certainty for PE sponsors. A private credit fund can close a unitranche loan in 4 to 6 weeks with a single counterparty, versus 8 to 12 weeks for a bank-syndicated process with multiple lenders. For PE sponsors competing on auction timelines, that certainty is worth a higher coupon.

After 2022, when SOFR rose sharply, every floating-rate private credit loan repriced upward automatically, lifting yields across existing portfolios. That windfall accelerated capital raising in 2023 and 2024.

How does private credit compare to a bank loan or a public bond?

The three financing channels overlap but serve different needs. The table below summarizes the main differences for a hypothetical $200 million senior secured loan to a private mid-market company:

| Dimension | Bank loan (syndicated) | Public high-yield bond | Private credit (direct lending) |

|---|---|---|---|

| Typical lender | Bank syndicate (5-30 lenders) | Bond mutual funds, insurers | One fund or club of 2-4 funds |

| Pricing | SOFR + 3% to 5% | Fixed coupon, traded daily | SOFR + 5% to 7% |

| Covenants | Few (cov-lite is now standard) | Few | Several maintenance covenants |

| Time to close | 8 to 12 weeks | 6 to 10 weeks | 4 to 6 weeks |

| Who can hold the loan | Banks, CLOs, mutual funds | Anyone via public markets | Fund LPs only |

The private credit pricing premium (typically 100 to 300 basis points over comparable syndicated debt) compensates the lender for the lack of secondary-market liquidity and the bespoke underwriting work.

What are the risks of private credit?

The IMF's April 2024 Global Financial Stability Report identified five interlocking vulnerabilities: relatively fragile borrowers, growing semi-liquid retail vehicles, layers of leverage at fund and borrower levels, partially subjective valuations, and unclear interconnections among participants. Default rates have been low through the recent rate cycle, but the asset class as currently structured has not yet been tested by a recession of meaningful depth.

The main risks worth understanding:

- Borrower fragility. Private credit borrowers are typically smaller and more leveraged than public-bond issuers. Many run with debt-to-EBITDA above 6x and would struggle to refinance in a credit-market shock. Around 40% of borrowers had interest coverage ratios below 1x in early 2024 according to IMF analysis.

- Valuation lag. Private credit loans are marked quarterly, often using fund-internal models with limited external price discovery. In a downturn, marks can lag actual deterioration by one or two quarters, masking losses temporarily.

- Layered leverage. A typical chain looks like: highly leveraged borrower → leveraged fund (some funds use 1x to 1.5x leverage on top of the borrower's debt) → leveraged investor (a BDC may borrow at the fund level too). A small drawdown can compound through these layers.

- Retail vehicle mismatches. Newer non-traded BDCs and interval funds offer monthly or quarterly liquidity to retail investors against an illiquid loan portfolio. Forced selling in a stress event could disrupt valuations across the asset class.

- Interconnection opacity. Banks fund private credit lenders through revolvers and warehouse lines, recreating bank exposure to mid-market loans through a different channel. Regulators have less visibility into these exposures than they would for a directly-held bank loan.

The 2023 IMF assessment is that systemic risk is "currently contained" but warrants closer monitoring as the asset class scales.

What is "private credit crisis" search interest about?

Search volume for "private credit crisis" climbs whenever a high-profile borrower defaults or a major fund posts an unusual mark-down. None of the events to date have triggered a systemic event, but they highlight that the asset class is large enough now that single-fund problems can move headlines. The Federal Reserve's August 2024 FEDS Note concluded that private credit "now rivals other major credit markets in size" and called for improved data collection. Closer regulator attention is the most likely path forward, not a crisis in the conventional sense.