An extension of your underwriting team, on demand

Send us a borrower file when you need extra diligence. We verify income, employment, education, assets, debts, identity, and business existence. AI-first, with a human reviewer on every case that calls for judgment.

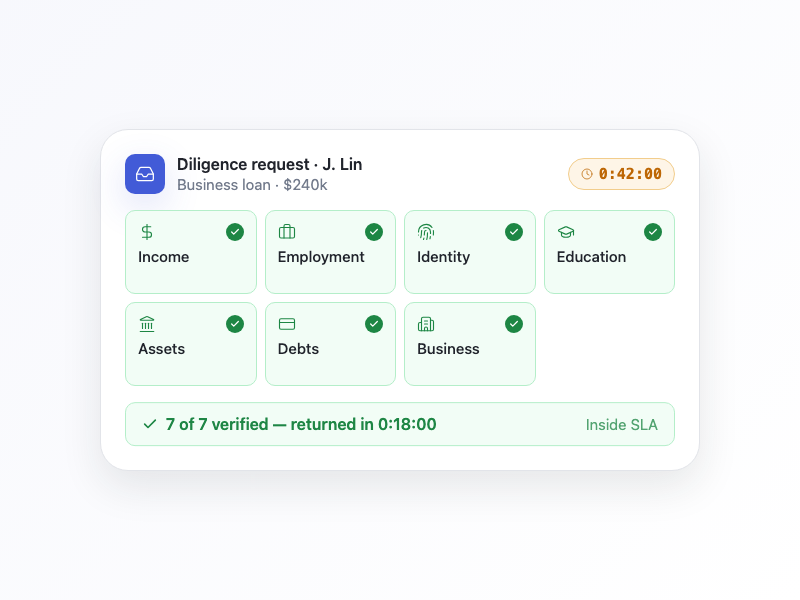

Diligence on every borrower you want a closer look at

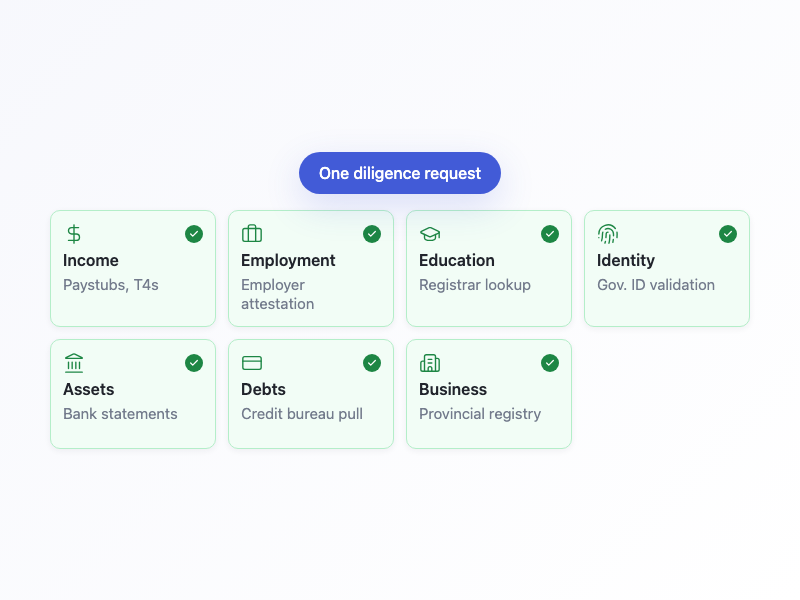

Seven verifications, one intake form

Income, employment, and education

Paystubs, employer attestations, school registrar lookups, T4s, and self-employment cashflow. We capture the document trail and resolve discrepancies between sources before the report goes back.

Identity, assets, debts, and business existence

Government ID validation, bank-statement asset confirmation, credit and registry debt pulls, and operating-status checks against provincial registries and corporate filings.

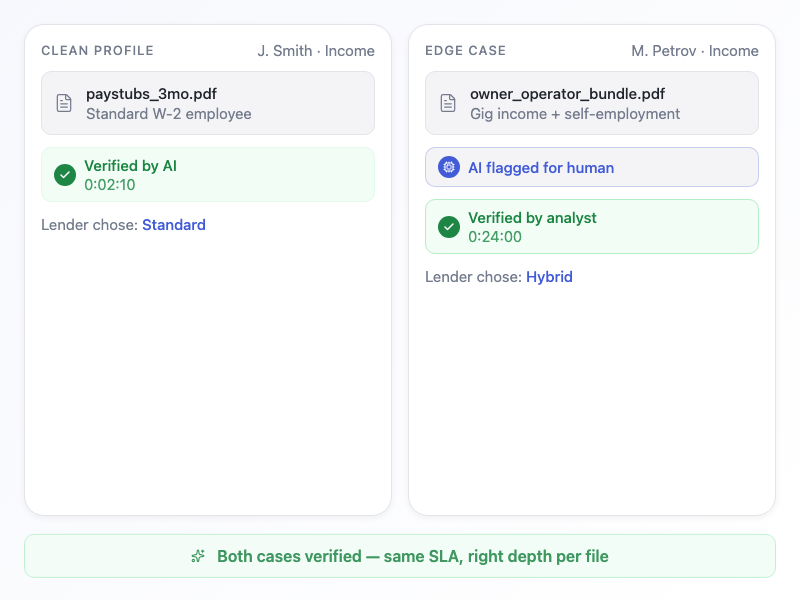

AI-first, human-deepened where it matters

Pick the depth per request

Standard diligence runs through automated checks for cases that fit a clean profile. Hybrid diligence routes complex files (gig income, foreign documents, owner-operator businesses) to a human reviewer before the result returns.

Every flagged case lands with a human reviewer

If the AI surfaces a contradiction, an unreadable document, or an edge case outside its training distribution, a credit analyst takes over. You see the result, not the handoff.

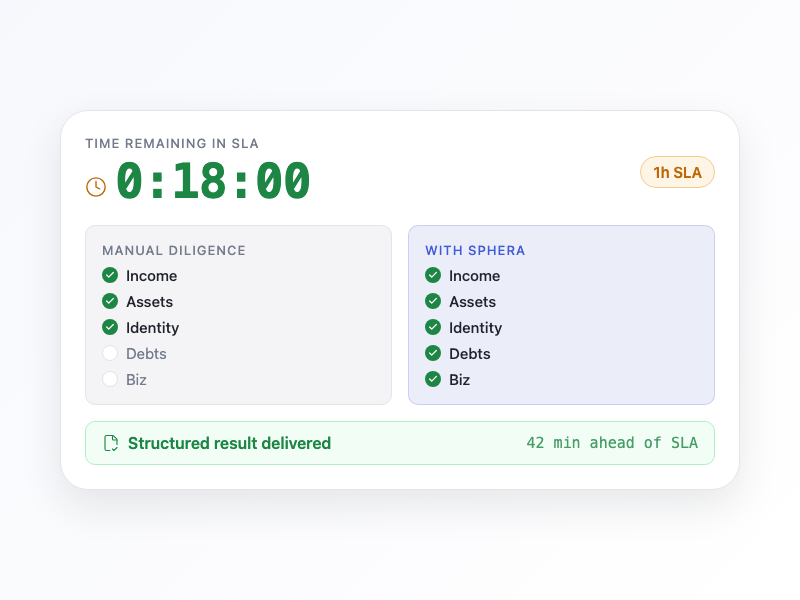

Diligence inside the deadline you set

Pick the SLA when you ship the request

1-hour, 12-hour, or 24-hour deadlines on every file. We run the diligence in parallel to your own underwriter and return the report inside the window. Your decision timeline doesn't change.

Structured results, not a PDF

Each verification returns a result code (verified, partial, contradicted, unverifiable) and the underlying evidence. Your underwriting system ingests it the way it would your own data.

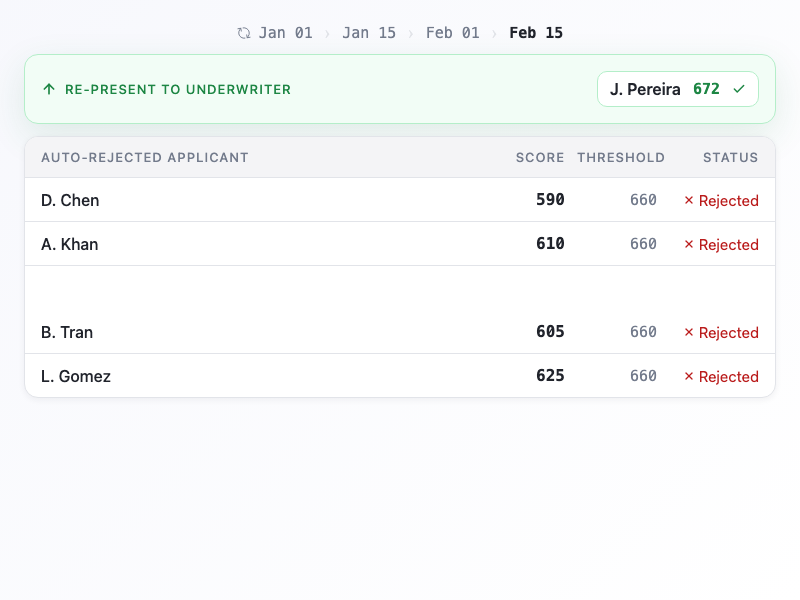

Re-qualify the borrowers your filters auto-rejected

Continuous monitoring of the auto-reject pool

We watch the variables your auto-rejection rules depend on (credit score, time in business, declared revenue) and surface borrowers whose profiles have moved into your credit box since they applied.

Re-verify the data points that gated the decision

When a borrower self-reports $90k in revenue against a $100k threshold, we re-verify against bank statements and tax filings. If the actual number qualifies, the file comes back to you with the corrected data.

How much revenue is sitting in your auto-reject pool?

Plug in your numbers. We'll show what re-qualifying a slice of your auto-rejects would mean for annual originations and net interest margin.

Applications auto-rejected per month

Add Sphera to your diligence stack

We start with a sample of your active applications or auto-reject pool, return verified files within your SLA, and benchmark accuracy against your existing process.