How long does underwriting take?

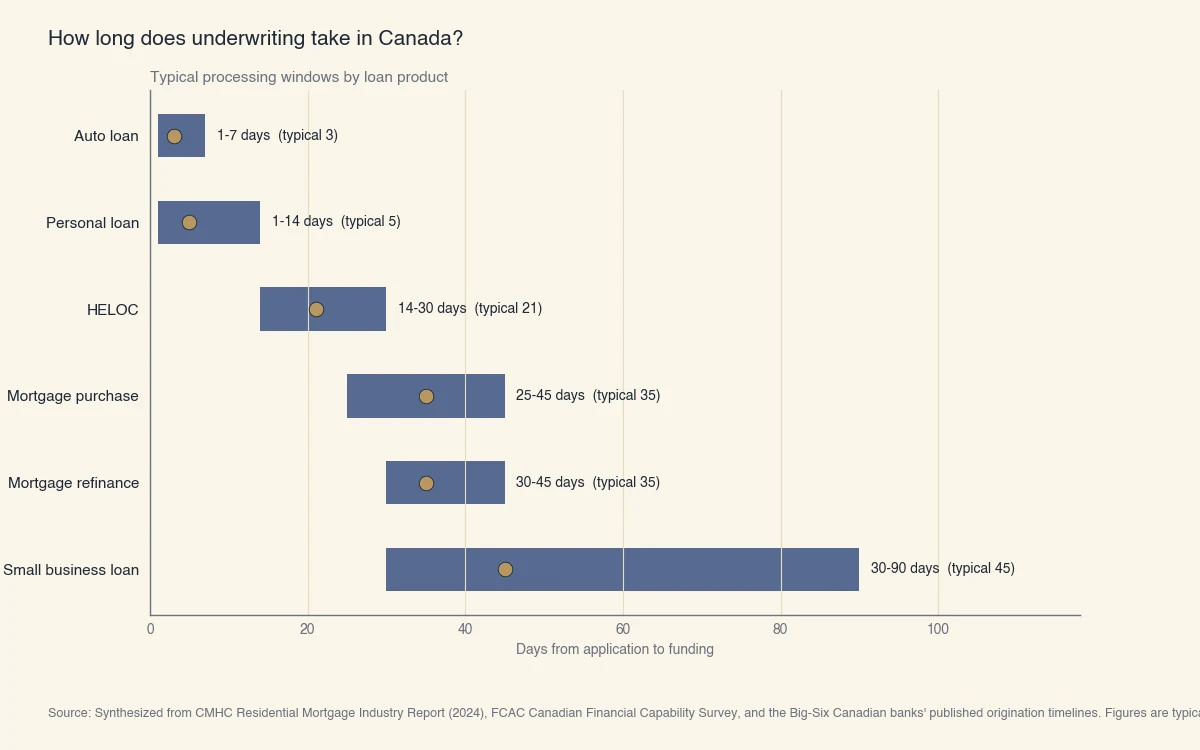

Mortgage underwriting in Canada typically takes 25 to 45 days from application to funding, with the underwriter's actual review usually completing within 5 to 10 business days once the file is complete. Auto loans close in 1 to 7 days, personal loans in 1 to 14 days, and small business loans in 30 to 90 days. The total timeline depends less on the underwriter and more on how quickly the borrower, appraiser, lawyer, and back-office can deliver each piece of the file (CMHC).

Underwriting is the lender's risk-assessment process: someone reviews your income, debts, credit history, and (for secured loans) the collateral, then decides whether to fund the loan, at what rate, and on what terms. The underwriter does not make a single instant decision. They issue a conditional approval first, request supporting documents, and only sign off on a final approval once every condition clears.

Why timing matters in practice: purchase mortgages in Canada run on a tight closing calendar set by the agreement of purchase and sale. A delay of even three business days can break the closing date, trigger penalties, and in some cases unwind the deal. Refinances and HELOCs are more forgiving on calendar but borrowers still feel the cost in carrying interest on the existing facility.

What slows underwriting down?

The four common bottlenecks are missing or late documents (income proofs, side-account statements, gift letters), appraisal scheduling and review, employment verification call-backs, and credit-file changes during the underwriting window. The single largest variable is documentation completeness on day one.

How long does mortgage underwriting take in Canada?

A typical Canadian purchase mortgage closes 25 to 45 days from application, with the underwriting decision itself usually arriving 5 to 10 business days into that window. OSFI Guideline B-20 sets the residential underwriting standards every federally-regulated lender must follow (OSFI), which means the workflow looks similar across the Big Six banks, the credit unions, and the monoline lenders.

The chart below shows the typical processing window by loan product. The dot marks the typical center of the range; the bar shows the min-to-max band most borrowers fall inside.

Source: Synthesized from CMHC Residential Mortgage Industry Report (2024), FCAC Canadian Financial Capability Survey, and the Big-Six Canadian banks' published origination timelines. Figures are typical ranges, not guarantees.

The mortgage timeline breaks into three phases:

| Phase | What happens | Typical duration |

|---|---|---|

| 1. Application + initial review | Borrower submits application; lender pulls credit; broker collects income docs | 1-3 business days |

| 2. Underwriting + conditional approval | Underwriter reviews file, issues conditional approval with a list of conditions | 3-7 business days |

| 3. Conditions + appraisal + final approval | Borrower clears conditions; appraiser inspects; lender signs off | 5-15 business days |

| 4. Lawyer + funding | Borrower's lawyer prepares closing documents; funds released on closing date | 5-10 business days |

The underwriter is only actively working on the file in phases 2 and 3. The other phases are dominated by document gathering and external steps.

How long does final underwriting take?

Final underwriting, the stage where the underwriter clears every outstanding condition and signs off, usually takes 2 to 7 business days once the borrower has submitted every requested document. A "clean" file with no last-minute changes can clear in two days; a file with a missing pay stub or a credit inquiry triggered during the underwriting window can stretch a week.

This is the stage where borrowers most often sabotage their own timeline. Common late-stage mistakes that restart the conditions clock:

- Applying for new credit (a car loan, a credit card, even a soft-pull comparison tool that triggers a hard inquiry)

- Changing jobs or transitioning from employed to self-employed

- Moving large sums between accounts without an explanation memo

- Letting the appraisal report expire before closing

OSFI explicitly requires lenders to re-verify income and credit if the file ages beyond 90 days, so any delay past that window restarts most of the underwriting work.

How long does an underwriter take to make a decision?

An underwriter typically takes 1 to 5 business days to review a complete file and issue an initial decision; complex files take longer because each non-standard component must be verified independently. A salaried employee with two pay stubs, a clean credit file, and a standard property type can clear initial underwriting in a day. A self-employed borrower with three years of personal and business tax returns, two corporate accounts, and a rental property can take a week.

Complexity drivers, in approximate order of impact:

- Self-employed or commission-based income. Lenders typically average two years of net income from T1 General returns and require Notice of Assessments to verify the numbers were filed.

- Non-standard property type. Rural property, leasehold, mixed-use, or atypical zoning needs an additional underwriting review.

- Multiple income sources. Each source needs independent verification: payroll, contract letters, pension statements.

- Recent credit-file activity. A new tradeline or a recent missed payment requires the underwriter to revisit the credit decision.

- Down-payment source. Gift letters, sale-of-property proceeds, or RRSP-Home-Buyers'-Plan withdrawals each require their own paper trail.

A clean file is fast not because the underwriter rushes, but because the lender's automated systems pre-clear most of the boxes. The underwriter only reviews the exceptions.

What's the difference between conditional and final approval?

Conditional approval is the underwriter's commitment to fund the loan IF a list of remaining conditions are met; final approval comes only after every condition clears. A conditional approval is not a guarantee. The lender can still decline at the final-approval stage if any of the conditions fail to clear.

Typical conditions on a Canadian mortgage approval letter:

- Satisfactory property appraisal (the lender orders this; the borrower pays)

- Confirmation of down payment with 90-day account statements

- Most recent year's Notice of Assessment for self-employed borrowers

- Solicitor information (the lender will not fund without a registered Canadian lawyer's information)

- A gift letter, if any portion of the down payment is a gift

- Property insurance binder effective the closing date

- Default insurance (CMHC, Sagen, or Canada Guaranty) if the down payment is below 20%

Each condition is a small task with a clear deliverable. The borrower's job is to clear the easy ones (Notice of Assessment, account statements) immediately and chase the slow ones (solicitor, property insurance) in parallel.

What about FHA and VA loans?

FHA and VA loans are US federal mortgage programs that do not exist in Canada. Canadian buyers using a default-insured mortgage instead work with CMHC, Sagen, or Canada Guaranty, which act as the high-ratio insurance layer behind the lender. Default insurance adds 1 to 5 business days to the timeline because the insurer must approve the file in addition to the lender's underwriter.

For US-style FHA / VA underwriting timelines, see the lender's published origination guide. The Canadian equivalent (default-insured high-ratio mortgage) runs slightly slower than a conventional mortgage but is still typically inside the 25-to-45-day window.

How can a borrower speed up underwriting?

The single biggest accelerator is having a complete file ready on day one: every income document, every account statement, the property purchase agreement, and the lawyer's information. Most underwriting delays are document-gathering delays, not lender delays. Borrowers who arrive at application with everything pre-collected typically clear underwriting in the bottom half of the typical range.

A practical pre-application checklist for a Canadian mortgage:

- Income proof for the past 24 months. Pay stubs (last two), Notices of Assessment (last two), and an employment letter dated within 30 days of application. Self-employed borrowers add T1 General returns and corporate financial statements.

- Down-payment paper trail. Ninety days of statements for every account that holds the down payment, plus signed gift letters for any portion that is gifted.

- Property documentation. The signed agreement of purchase and sale, the listing sheet, and the property tax bill. The lender orders the appraisal, but borrowers should confirm property access for the appraiser the same day.

- Lawyer information. Many borrowers wait to hire a lawyer until after conditional approval. Hiring early lets the lender send instructions immediately and shaves three to five days off the closing window.

- Banking history. A consolidated 90-day deposit history showing income coming in and large transfers explained.

The Bank of Canada's Financial Stability Report has consistently flagged that mortgage origination volumes spike in March-June, which lengthens every step of the process. Closing in the off-peak window (October through January) often saves a full week. For the broader mechanics of what underwriting actually is, see what is underwriting. To model how your specific scenario translates into a monthly payment while the file is being reviewed, run the numbers through the mortgage payment calculator.

A second accelerator is using a mortgage broker who pre-qualifies the file before sending it to the lender. Broker pre-qualification trades 1 to 3 days of upfront work for what is often a much shorter underwriting cycle, because the broker has already collected and checked the documents the lender's underwriter would have requested.