What is underwriting?

Underwriting is a lender's process of assessing the risk of lending money to a specific borrower for a specific purpose, then deciding whether to fund the loan, at what interest rate, and on what terms. The underwriter reviews income, debt, credit history, and (for secured loans) the collateral. The output is a yes / no / conditional decision, plus the rate and the conditions if approved. Every regulated Canadian lender follows OSFI's Guideline B-20 for residential mortgages and the equivalent prudential standards for other product lines (OSFI).

The word itself comes from a 17th-century Lloyd's of London marine-insurance practice: brokers wrote each underwriter's name UNDER a description of the risk being insured, signaling the share each was willing to take. The mechanic transferred easily to lending in the 19th and 20th centuries, where "underwriting" became shorthand for any disciplined risk assessment that ends in a price and a decision.

Why underwriting matters in practice: the rate you receive, the products you can access, and even the products you'll be denied are all outputs of an underwriting decision. Two borrowers with the same income and same credit score can receive different decisions because their files trip different conditions in the lender's policy. Understanding what the underwriter is looking at is the borrower's leverage in the conversation.

Who is the underwriter?

The underwriter is either a person or an automated system. Large banks employ teams of human underwriters specialized by product (residential mortgage, commercial credit, consumer auto, business). For lower-risk loans, the bank's automated decision engine handles most of the file and a human reviews only exceptions. For high-stakes commercial loans, an entire credit committee reviews the file before the senior underwriter signs. If the role itself interests you, see how to become a mortgage underwriter.

What does an underwriter do?

An underwriter verifies the application data, checks each item against the lender's credit policy and the regulator's standards, calculates the risk metrics (debt-to-income, loan-to-value, debt service coverage), and issues a decision. The underwriter is the final authority on whether to approve the loan, at what rate, and with what conditions.

A typical underwriter's work on a residential mortgage file:

- Verify the income. Match pay stubs to the most recent Notice of Assessment, look for income-trend issues, identify any non-recurring items (signing bonus, one-time RRSP withdrawal) that should not count.

- Pull and read the credit bureau report. Look at scores from Equifax and TransUnion, but also at the underlying tradelines: how many open accounts, how much each is being used, any late payments or collections.

- Calculate the qualifying ratios. Gross Debt Service (GDS) and Total Debt Service (TDS) under OSFI's guidance, applying the federal qualifying-rate stress test to make sure the borrower can pay even if rates rise.

- Review the property. The appraisal report, the property's age, location, condition, and any non-standard features. The collateral has to be saleable in a worst-case scenario.

- Check the down-payment source. Ninety days of bank statements, gift letters where applicable, sale-of-home proceeds where applicable.

- Make the decision. Approve, decline, conditional-approve with a list of items to clear, or counter-offer with revised terms.

Underwriters do not invent the rules. They apply the lender's credit policy, which itself is shaped by OSFI's prudential standards, the Bank of Canada's Financial Stability Report observations, and the lender's own loss experience over time (Bank of Canada).

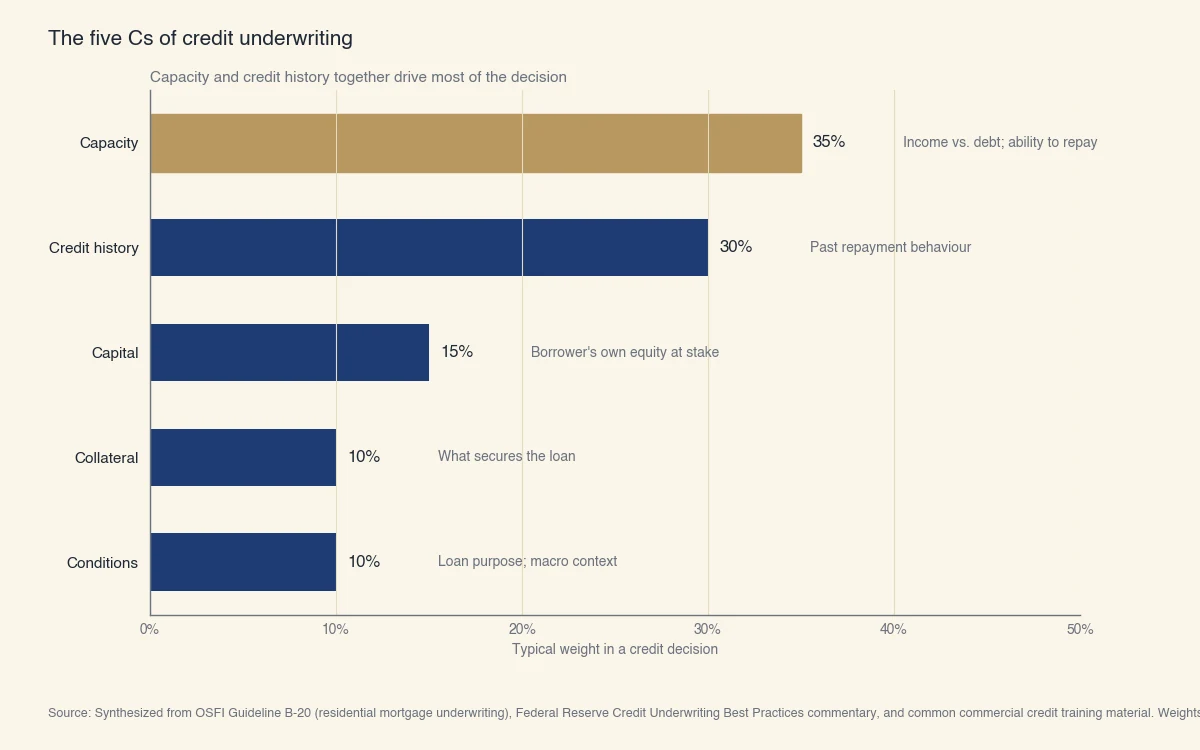

What are the 5 Cs of credit underwriting?

The five factors every credit underwriter weighs are Capacity (income vs. debt), Credit history, Capital (the borrower's own equity), Collateral (what secures the loan), and Conditions (loan purpose and macro context). The "5 Cs" framework appears in every commercial credit-training program and underlies the credit policies of most Canadian banks, even when those policies don't use the exact letters.

The chart below shows the typical weighting of each C in a credit decision. Capacity dominates because if a borrower can't actually afford the payments, nothing else matters; credit history runs second because past behaviour is the strongest available predictor of future behaviour.

Source: Synthesized from OSFI Guideline B-20 (residential mortgage underwriting), Federal Reserve Credit Underwriting Best Practices commentary, and common commercial credit training material. Weights are illustrative.

What each C looks like in a real underwriter's review:

| The C | What's measured | Typical metric |

|---|---|---|

| Capacity | Can you make the payment? | GDS ≤ 39%, TDS ≤ 44% (CMHC default-insured) |

| Credit history | Have you paid back before? | 660+ for prime; 720+ for best-rate prime |

| Capital | What's your skin in the game? | 5%+ down payment for high-ratio; 20%+ for conventional |

| Collateral | What can the lender recover if you default? | Loan-to-value ratio + property quality |

| Conditions | Is the loan purpose sound? | Owner-occupied vs. rental, primary vs. second home |

The weights vary by product. A small business loan weights Capacity (cash flow) and Conditions (industry health) more than a mortgage. An auto loan weights Capacity and Collateral; credit history matters but is partially offset by the resale value of the vehicle. The framework adapts; the five buckets stay the same.

What is automated underwriting vs. manual underwriting?

Automated underwriting runs the file through a rules engine that returns a decision in minutes. The two North American giants are Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA); Canadian banks use internal scorecard equivalents. Automated underwriting handles the majority of clean files (salaried borrower, standard property, prime credit) without a human ever opening the folder.

Manual underwriting puts a human underwriter on the file. Manual review is triggered when the file falls outside the automated system's tolerances:

- Self-employed or commission-based income that needs analysis

- Credit score below the lender's automated minimum

- Non-standard property (rural, leasehold, mixed-use)

- High debt-to-income ratios that need compensating factors

- Past credit events (bankruptcy, foreclosure, collections) within the look-back window

Manual underwriting takes longer and approves a wider range of files. The trade-off is the underwriter's judgment, which can swing decisions either way at the margin.

What is mortgage underwriting in Canada?

Mortgage underwriting in Canada operates under OSFI Guideline B-20 for federally regulated lenders, which sets the qualifying-rate stress test, the documentation standards, and the prudential limits on loan-to-value and debt-service ratios. Provincially regulated lenders (most credit unions) apply equivalent rules, and the default insurers (CMHC, Sagen, Canada Guaranty) layer their own standards on top for high-ratio mortgages (OSFI).

The Canadian mortgage underwriting workflow has four uniquely Canadian elements:

- The qualifying-rate stress test. Borrowers must qualify at the higher of (a) the contract rate plus 2 percentage points or (b) the Bank of Canada's published qualifying rate (currently 5.25%). The test exists to ensure the borrower can still afford payments if rates rise.

- GDS and TDS ratios. Gross Debt Service (housing costs / income) capped at 39% and Total Debt Service (all debt costs / income) capped at 44% for default-insured mortgages.

- Default insurance for high-ratio mortgages. Down payments below 20% require insurance from CMHC, Sagen, or Canada Guaranty. The insurer underwrites the file in addition to the lender.

- The 90-day file aging rule. Income, credit, and property documents older than 90 days must be re-verified. This is what makes drawn-out closings restart underwriting work.

The Bank of Canada's Financial Stability Report has consistently called Canadian mortgage underwriting "tighter than US standards" since the 2008-2010 reforms, citing the stress test and GDS/TDS caps as the key differences (Bank of Canada).

What is underwriting in business development?

In business and commercial banking, "underwriting" typically refers to commercial credit underwriting: the process of deciding whether to lend to a company. The 5 Cs framework still applies, but the metrics shift:

- Capacity is measured by Debt Service Coverage Ratio (DSCR), calculated as net operating income divided by debt service. A DSCR ≥ 1.25 is the typical commercial-loan minimum.

- Capital is the owner's equity in the business, measured from the most recent balance sheet.

- Collateral can be receivables, inventory, equipment, real estate, or all of the above.

- Conditions weighs the industry, the local economy, and the loan purpose more heavily than in retail.

Commercial underwriting is also more bespoke. Each loan is a custom analysis rather than a scorecard score, which is why commercial files take 30 to 90 days to underwrite versus 5 to 10 for a retail mortgage. The underwriter's judgment, plus the credit committee's review on larger files, drives the outcome.

How is underwriting evolving with AI?

Modern underwriting increasingly combines traditional 5-C analysis with machine-learning models that ingest alternative data: bank-account cash-flow patterns, utility payment history, rent reporting, and behavioural signals. The goal is not to replace human underwriters but to give them better information on the borrowers who fall outside the automated system's tolerances, exactly the borrowers who are most expensive to underwrite manually today.

Three developments are reshaping the field:

- Cash-flow underwriting. Reviewing 12-24 months of bank-account transactions instead of (or alongside) the credit bureau report. The CFPB has issued guidance noting that cash-flow data better predicts repayment for thin-file borrowers than traditional credit scores alone.

- Alternative-data scoring. Adding utility payments, rent, telecom, and BNPL repayment history to the file expands the population that can be scored at all.

- AI-augmented review. Machine-learning models pre-screen files, flag risk patterns, and surface the specific items the human underwriter should focus on. Used well, the borrower gets a faster decision and the underwriter spends time on the questions that actually matter.

The regulator's lens has been cautiously supportive. OSFI's recent commentary frames automation and AI as tools for consistency, provided the lender can explain every decision and demonstrate the model is fair across protected groups. The Financial Consumer Agency of Canada has issued similar guidance for consumer-facing credit (FCAC). For the specific role of an underwriter inside a mortgage transaction, see what a mortgage underwriter does. Borrowers asking about timing should also check how long mortgage underwriting takes.

The underlying job stays the same: decide whether to lend, at what rate, on what terms. The toolkit is widening; the framework (Capacity, Credit history, Capital, Collateral, Conditions) has not changed.