Is APR the same as interest rate?

No. The interest rate is the cost of borrowing the principal, expressed as an annual percentage; the APR (annual percentage rate) is the total cost of credit including the interest rate plus most upfront fees, also expressed as an annual percentage. APR is always equal to or greater than the interest rate. The two numbers are required to be disclosed side by side on every consumer credit document under federal Regulation Z, the Truth in Lending Act's implementation rule (CFPB).

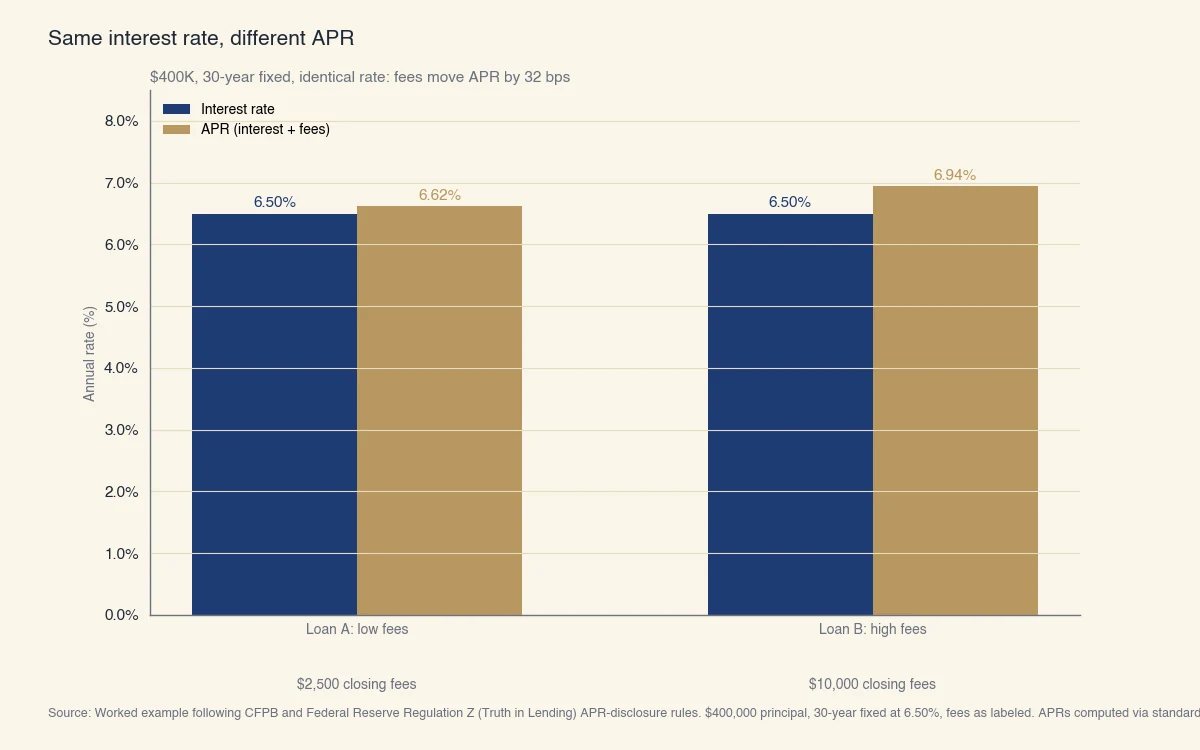

The difference matters in dollars. Two loans with the same interest rate but different fee packages produce different APRs and different total costs. The chart below shows two $400,000 30-year mortgages, both at 6.50% interest, with different closing-fee structures:

Source: Worked example following CFPB and Federal Reserve Regulation Z (Truth in Lending) APR-disclosure rules. $400,000 principal, 30-year fixed at 6.50%, fees as labeled. APRs computed via standard amortization.

Why the distinction matters in practice: the rate quoted in advertising, on rate-shopping sites, and on the lender's first-call rate sheet is the interest rate, not the APR. Two lenders advertising "6.50% mortgage rate" can quote APRs of 6.62% and 6.94% on otherwise identical loans because of the fee gap. APR is the apples-to-apples number. Whether that headline mortgage rate is itself rising or falling is a separate question, covered in whether mortgage interest rates are going down.

What is the interest rate exactly?

The interest rate is the percentage of the loan principal a lender charges per year for borrowing. On a $400,000 mortgage at 6.50%, the borrower pays roughly $26,000 in interest in the first full year, calculated on the outstanding balance each month. The interest rate determines the monthly principal-and-interest payment; it does not include closing costs, mortgage insurance, or anything paid upfront.

What is APR exactly?

The annual percentage rate (APR) is the rate that, when applied to the loan principal over the loan term, produces the same total cost as the actual stream of payments including the upfront fees. APR effectively spreads the upfront fees across the full loan term and re-expresses the result as an annual rate. Regulation Z requires lenders to disclose APR to a precision of one-eighth of one percentage point or better (Federal Reserve Regulation Z).

Why is the APR usually higher than the interest rate?

APR is higher than the interest rate whenever the loan has any upfront fees that count as prepaid finance charges, because APR averages those fees across the loan term while the interest rate ignores them entirely. A loan with zero upfront fees produces an APR equal to its interest rate. A loan with large upfront fees produces a meaningfully higher APR.

The fees that move APR upward fall into a few standard categories:

- Origination charges. What the lender charges to set up the loan, typically 0.5% to 1% of the loan amount.

- Discount points. Optional upfront payments to lower the interest rate. Each point is 1% of the loan amount and typically lowers the rate by 0.20 to 0.25 percentage points. Points raise APR.

- Mortgage broker fees. When a broker arranges the loan, broker compensation either gets paid by the lender (raising the interest rate) or by the borrower upfront (raising APR).

- Mortgage insurance premiums. FHA's upfront MIP and the lifetime annual MIP both flow into APR. Conventional private mortgage insurance (PMI) on loans with less than 20% down also flows in.

- Prepaid interest. Per-diem interest from the closing date to the end of the closing month.

Fees that do NOT move APR (under Regulation Z):

- Appraisal fee

- Credit report fee

- Title insurance and title search

- Recording fees and transfer taxes

- Property tax escrows and homeowners insurance escrows

- Notary and attorney fees the lender does not require

The distinction is not arbitrary: APR-includable fees are charges the lender controls. Excluded fees are third-party charges the lender passes through. The boundary is set in Regulation Z and explained in the CFPB's TILA-RESPA Integrated Disclosure (TRID) rule.

What is APR for a credit card?

Credit-card APR is conceptually different from loan APR. Cards do not have upfront fees the way mortgages do, so card APR is essentially the interest rate plus a few minor fees. The complication is that cards typically disclose multiple APRs: a purchase APR, a balance-transfer APR, a cash-advance APR, and (sometimes) a penalty APR that activates after a missed payment. Each applies to a specific balance bucket within the card.

The other quirk: most cards carry a grace period that means you pay no interest at all on purchases if you pay the statement balance in full each month. The advertised purchase APR only applies if you carry a balance.

Which matters more when comparing loans, APR or interest rate?

APR is the better single-number comparison if you plan to hold the loan to maturity (or close to it); interest rate is more meaningful if you plan to refinance, sell, or pay off the loan well before the full term. APR amortizes the upfront fees across the projected loan life. If your actual life is shorter, you pay the full fees against a smaller interest base, and your effective rate over your real holding period is higher than the disclosed APR.

A practical decision rule for mortgages:

| Holding period | Better cost compass |

|---|---|

| Plan to hold full term | APR |

| Plan to refinance in 3 to 5 years | Interest rate, then back-of-envelope on the fees |

| Plan to sell within 2 to 3 years | Interest rate dominates; high-fee / low-rate "buydown" loans almost always lose |

| Variable-rate loan | Interest rate today + the rate caps; APR estimates assume current index forever |

The CFPB's "Loan Estimate" form, which every mortgage applicant must receive within 3 business days of application, places interest rate and APR on the same page so the comparison is direct. Look at both and run the math for your own holding plan.

What about adjustable-rate mortgages?

For an adjustable-rate mortgage (ARM), the disclosed APR uses a fully-indexed rate computed from the current value of the underlying index plus the margin. This is a snapshot of what the rate would be if the index never moved again. Real APR on an ARM depends on which way the index moves over the loan's life, which is by definition unknown. The CFPB requires lenders to disclose the rate caps and the worst-case payment scenario alongside the APR for ARMs (CFPB).

For ARMs more than for fixed-rate loans, treat APR as a directional comparison rather than an exact cost prediction. The interest rate, the index, the margin, and the rate caps together determine your real cost.

How is APR calculated?

APR is the rate that makes the present value of the borrower's full payment stream (principal, interest, and APR-includable fees) equal to the loan amount disbursed at closing. Lenders solve for it iteratively using formulas published in Federal Reserve Regulation Z. The CFPB provides an APR calculator and worked examples on its consumer-tools website.

The intuition: imagine paying $10,000 in upfront fees on a $400,000 mortgage at a 6.50% interest rate. Effectively, you only borrow $390,000 net (the $400K loan minus $10K of fees you immediately pay back to the lender), but you owe interest and amortization on the full $400,000. Solving for the rate that makes the disbursed-vs-paid math balance gives you the APR (about 6.94% in that example).

Why APR uses 30 years (or whatever the original loan term) rather than your expected holding period: federal disclosure rules require a single standardized comparison number, and the only number that does not depend on borrower-specific assumptions is the full original term. This is why APR works best for held-to-term loans and gets less accurate as the actual holding period shortens.

Common APR mistakes when comparing loans

The two most common APR mistakes are comparing APR across products of different terms (a 15-year and a 30-year mortgage are not directly comparable), and treating APR as a fixed truth on adjustable-rate loans where the underlying index will move. Each mistake quietly biases the borrower toward the wrong loan choice.

The mistakes worth recognizing:

- Comparing 15-year and 30-year APRs directly. A 15-year mortgage at a lower interest rate may show a higher APR than a 30-year at a higher interest rate because the same upfront fees get amortized over half as much time. Compare 15-year-to-15-year, 30-year-to-30-year.

- Comparing fixed and adjustable APRs. Fixed-rate APR is exact; ARM APR is a snapshot using today's index. The two are not comparable on equal footing for held-to-term plans.

- Ignoring third-party fees. APR excludes appraisal, title, and recording costs. A loan with the lowest APR can still cost more if its third-party fees are higher. Always look at the full Loan Estimate, not just the APR line.

- Using APR for loans you'll refinance. APR amortizes upfront fees over the full original term. If you'll refinance in 4 years, your real cost is the interest rate plus the prepaid fees as a one-time hit, not the APR.

- Trusting the advertised APR. Mortgage rate-shopping sites often quote APRs based on "best-case" assumptions: 740 FICO, 25% down, primary residence, no broker fee. For the score thresholds behind that 740 figure, see the credit score you need to buy a house. The rate sheet you actually receive will reflect your real file. Get a Loan Estimate, not a rate-shopping quote, before deciding.

The CFPB publishes a free side-by-side Loan Estimate comparison tool that lines up APR, interest rate, monthly payment, total interest paid, and the third-party fees in one view. This is the right place to compare two real offers (CFPB). For the underlying math, see how to calculate an interest rate. If a discount-point buydown is part of your comparison, how much it costs to buy down a rate walks through the breakeven math.

A practical workflow: get Loan Estimates from at least three lenders, lay them side by side, look at APR for the comparison signal, and look at the "Total Loan Costs" and "Total Other Costs" columns for the full bill. The lowest APR is usually the right loan. The exception is when one lender's third-party fee package is meaningfully different, in which case the headline APR can mislead.