What is asset-based lending?

Asset-based lending (ABL) is a form of secured business credit where the loan amount is derived from the appraised value of specific company assets, typically accounts receivable and inventory, rather than from projected cash flow. The lender extends credit equal to a percentage (the advance rate) of the eligible collateral value, and the borrower's available credit moves up and down as those assets fluctuate. The Office of the Comptroller of the Currency's ABL handbook is the authoritative US reference for how regulated banks structure these facilities (OCC).

ABL exists because not every business has a clean cash-flow story. A manufacturer with a $50 million inventory of finished goods might have lumpy cash flow but very high collateral value; a distributor with $30 million in invoices outstanding might have a thin margin but excellent receivables quality. Cash-flow underwriting underprices both. Asset-based underwriting prices them correctly by lending against what the borrower actually owns and can pledge.

Why the distinction matters in practice: ABL is the dominant credit form for mid-market US companies in inventory-heavy or receivables-heavy industries. The Secured Finance Network's annual market sizing report tracks roughly $4.5 trillion in committed ABL facility limits across thousands of US borrowers, with new commitments running near $400 billion a year (SFNet).

What does "secured by assets" actually mean?

The lender takes a first-priority security interest in the named collateral, perfected through UCC-1 financing-statement filings (and through possession or control for certain asset types). If the borrower defaults, the lender can take the collateral and liquidate it. ABL lenders structure facilities to ensure the loan amount never exceeds what they could realistically recover from a forced sale of the collateral within 6 to 12 months.

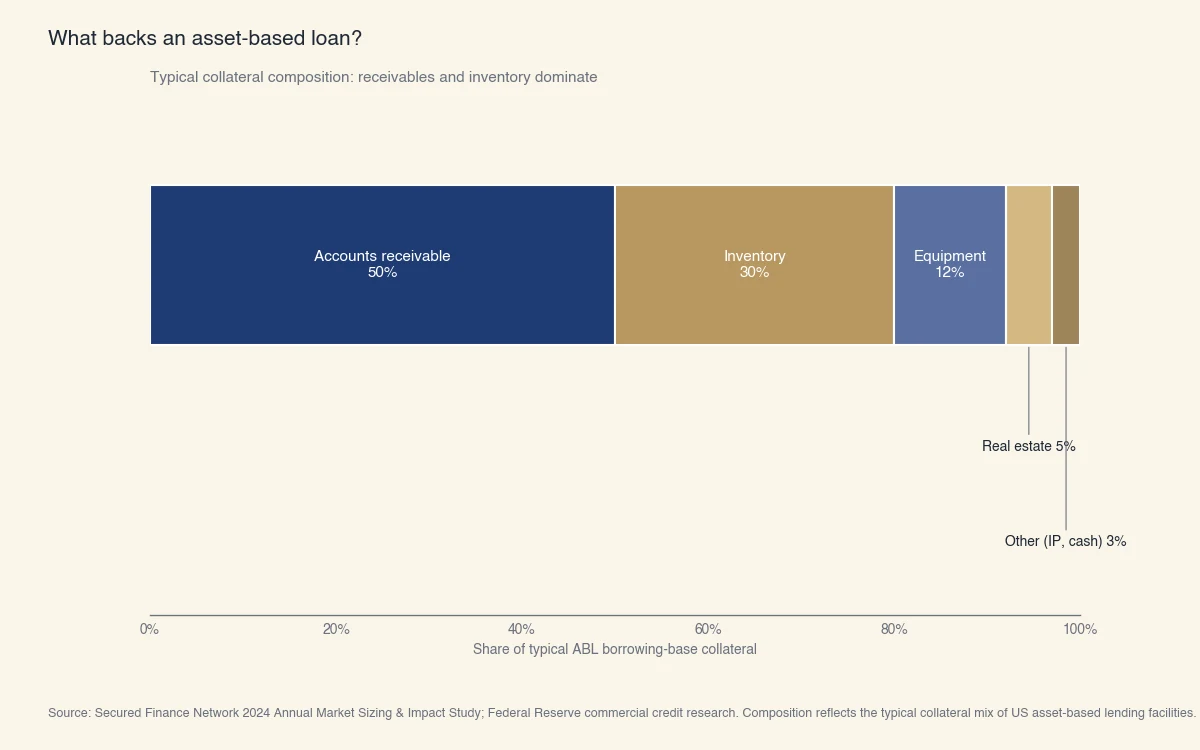

What backs an asset-based loan?

The typical ABL collateral mix is dominated by accounts receivable (around 50%) and inventory (around 30%), with equipment, real estate, and other assets making up the remainder. The composition reflects which assets are easiest to value, monitor, and liquidate.

Source: Secured Finance Network 2024 Annual Market Sizing & Impact Study; Federal Reserve commercial credit research. Composition reflects the typical collateral mix of US asset-based lending facilities.

Each collateral type comes with its own advance rate and monitoring requirements:

| Collateral type | Typical advance rate | What the lender monitors |

|---|---|---|

| Accounts receivable | 80-90% of eligible | Aging report; concentrations; dilution |

| Inventory (raw materials) | 30-50% of cost | Turnover; seasonality; obsolescence |

| Inventory (finished goods) | 50-65% of net orderly liquidation value | Days-on-hand; aging |

| Equipment | 70-80% of NOLV | Annual or biennial appraisal |

| Real estate | 60-75% of appraised value | Annual valuation; tax / lien status |

Eligible is doing a lot of work in those advance rates. ABL agreements specify exactly which receivables count: not those over 90 days old, not those owed by an affiliated party, not those concentrated above a percentage cap, not those owed by a government entity unless properly assigned. Inventory has parallel exclusions: no obsolete stock, no consigned goods, no inventory at non-permitted locations.

What is the borrowing base?

The borrowing base is the dynamic credit limit calculated by applying the advance rates to the current eligible collateral. The borrower reports the borrowing base to the lender weekly (sometimes daily for very large facilities, monthly for smaller ones) on a borrowing-base certificate. Available credit equals the borrowing base minus the outstanding loan balance and any reserves.

A typical mid-market borrowing-base formula on a $50 million ABL facility:

- 85% of $25 million eligible receivables = $21.25 million

- 50% of $30 million eligible inventory = $15 million

- Subtotal = $36.25 million

- Less: $2 million reserve (unpaid taxes, rent, dilution) = $34.25 million

The facility is committed to $50 million but the borrower can only draw $34.25 million today. As receivables collected reduce the outstanding balance and new sales build new receivables, the available borrowing capacity rolls forward.

How does asset-based lending differ from cash-flow lending?

Cash-flow lending sizes a loan from projected EBITDA (typically 3 to 6 times); asset-based lending sizes from the present value of pledged collateral (typically 50 to 90% of eligible). The two are different products serving different borrowers, with different reporting, different pricing, and different default behavior.

The structural differences:

| Dimension | Cash-flow loan | Asset-based loan |

|---|---|---|

| Sizing basis | Projected EBITDA × leverage multiple | Eligible collateral × advance rate |

| Typical price | SOFR + 4-7% (mid-market) | SOFR + 2.5-4.5% |

| Reporting | Quarterly financials | Weekly or monthly borrowing base |

| Covenants | Financial maintenance (DSCR, leverage) | Springing covenants only when availability drops below threshold |

| Best for | Stable cash flows, EBITDA visibility | Inventory / receivables-heavy operations |

| Stress behavior | Covenants tighten as EBITDA falls | Borrowing base contracts with assets |

The most important practical difference is what happens in a downturn. A cash-flow loan's leverage covenant tightens precisely when the borrower's EBITDA falls, exactly when the borrower needs flexibility most. An ABL's borrowing base contracts in proportion to the collateral, but does not have a financial-maintenance covenant unless availability drops below a threshold (typically 10 to 15% of the facility limit). Many companies move from cash-flow facilities to ABL during periods of EBITDA volatility and back when stability returns.

Pricing: what does an ABL facility cost?

Pricing carries three components:

- Spread: SOFR plus 2.50 to 4.50%, depending on credit quality and collateral mix. Higher-quality receivables (investment-grade obligors, low concentrations) and well-monitored inventory get tighter spreads.

- Unused-line fee: 0.25 to 0.50% on the undrawn portion. ABL lenders earn the unused fee whether the borrower draws or not.

- Upfront fee + monitoring fee: A 0.50 to 1.00% upfront fee at closing plus a $50,000 to $150,000 annual collateral monitoring fee.

ABL is typically cheaper than mezzanine debt or unsecured cash-flow credit for mid-market borrowers, but more expensive than investment-grade syndicated revolvers. The trade-off is the heavier reporting burden.

Who uses asset-based lending and why?

ABL serves mid-market companies in inventory-heavy or receivables-heavy industries (manufacturers, distributors, retailers, staffing firms), companies in transition (post-acquisition, turnaround), and rapid-growth firms whose financing need outpaces cash-flow lending capacity. The OCC's handbook lists these as the canonical ABL profiles, and the SFNet's industry data confirms manufacturers and distributors together account for over half of US ABL facility volume.

The four most common reasons a borrower chooses ABL over alternatives:

- Sizing. A receivables- or inventory-heavy company often gets a meaningfully larger facility from ABL than from cash-flow lending. A $30 million EBITDA distributor with $80 million of working-capital assets might qualify for $90 to $150 million ABL versus $90 to $180 million cash-flow, but the ABL covenants sit much lighter on the business.

- Covenant flexibility. ABL's springing financial covenants only test when availability is low. A cash-flow loan's maintenance covenants test every quarter regardless of liquidity.

- Counter-cyclical capacity. During downturns, ABL availability contracts with collateral but does not trigger leverage-covenant resets. Many borrowers refinance from cash-flow to ABL when EBITDA softens.

- Acquisition financing. ABL is the standard structure for leveraged acquisitions where the target's working-capital assets fund a meaningful share of the purchase price.

What does ABL look like in a downturn?

During the 2008-2009 financial crisis and the 2020 pandemic, ABL facilities held up notably better than cash-flow leveraged loans on a default-rate basis. Two structural reasons: borrowing-base contraction is automatic and self-limiting (you cannot over-extend on collateral that no longer exists), and ABL lenders are typically banks with relationship orientation rather than CLO managers under tranche pressure.

The Federal Reserve's Senior Loan Officer Opinion Survey shows ABL terms generally tighten less than cash-flow terms during stress periods, and recover faster (Federal Reserve). This is a structural feature of how the product is sized, not a discretionary credit decision.

How is an ABL facility structured?

A typical ABL facility documents three core elements: the credit agreement (defining the facility, advance rates, eligibility, covenants), the security agreement (perfecting the lien on each asset class), and the operating agreement with the lender's collateral monitoring team. SEC filings of public-company ABL credit agreements give the standard market template (SEC EDGAR).

The closing-to-funding workflow:

- Field exam. Before closing, the lender hires a third-party field examiner to verify receivable aging, inventory existence and condition, and the borrower's accounting controls. The exam costs $30,000 to $80,000 and takes 3 to 6 weeks.

- Appraisal. Inventory NOLV appraisal (and equipment NOLV if equipment is in the borrowing base). Independent appraisers from firms like Hilco, Tiger Capital, or Gordon Brothers.

- Credit agreement negotiation. Sizing the advance rates, defining eligibility, setting the unused-line fee, the spring-test threshold, and the covenant package. Typically 30 to 60 days from term sheet to closing.

- Security perfection. UCC-1 filings on receivables and inventory (state-by-state for companies with multi-state operations), control agreements on lockbox accounts, mortgages on any included real estate, equipment titles where applicable.

- Funding. First borrowing-base certificate establishes initial availability; the borrower draws against it.

The ongoing operating cycle: weekly or monthly borrowing-base report, daily lockbox sweep of receivable collections, quarterly collateral exam, annual NOLV appraisal refresh.

What's a "lockbox" in ABL?

A lockbox is a bank account in the lender's name (or the borrower's name with the lender having sole control) where customer payments are deposited. The lender sweeps the lockbox daily to pay down the borrower's outstanding ABL balance, then the borrower re-borrows as needed for operations. This control mechanism is what gives the ABL lender confidence that receivable collections actually reduce the loan rather than fund other uses.

A "springing lockbox" sits dormant until availability drops below a threshold, at which point the lender activates daily sweep and tighter controls. This is the mid-market market standard; full lockbox from day one is more common for distressed or higher-risk credits.

What are the risks of asset-based lending?

The two most cited risks for ABL borrowers are reporting burden and dilution risk on receivables; the two most cited risks for lenders are inventory obsolescence and concentration in single industries. Both sets of risks are well-understood and priced into the product, but they are real.

For borrowers:

- Reporting load. Weekly or monthly borrowing-base certificates require accurate, current sub-ledgers. A company without good accounting infrastructure can fail to deliver clean reports and find its facility frozen.

- Dilution. When customers dispute, return, or short-pay invoices, the lender deducts the dilution from eligible receivables. High-dilution industries (consumer goods, software with refunds) get tighter advance rates.

- Lockbox cash management. The borrower no longer has direct access to receivable collections; cash flows through the lender's account first. Treasury operations need to be designed around this.

- Field exam costs. The lender's annual field exam (typically $20,000 to $60,000) is a cost the borrower pays. For an adjacent commercial-credit category that also operates outside the traditional bank rails, see what is private credit.

For lenders, the OCC's ABL handbook flags inventory obsolescence and customer concentration as the two largest historical loss drivers in ABL portfolios, alongside fraud (false invoices, double-pledged inventory). The product's structural strength is collateral-based recovery, but recovery only works if the collateral is real and unencumbered.