What is a good credit score in Canada?

A good credit score in Canada is 660 or higher on the 300-900 scale used by Equifax and TransUnion, with 760+ considered excellent and 800+ near-perfect. This range is what most Canadian banks, credit unions, and prime lenders look for when deciding whether to approve a loan application and at what interest rate (Equifax Canada).

Your credit score is a three-digit number generated from the information in your credit report, which tracks your borrowing and repayment history with banks, credit-card issuers, telecom providers, and other lenders. Two credit bureaus, Equifax Canada and TransUnion Canada, each maintain their own version of your file and produce their own score from it.

The score itself is not a measure of your wealth, your income, or your overall financial health. It measures one specific thing: your historical pattern of repaying credit obligations on time and in full. A high score means lenders trust you to pay back what you borrow. A low score means they expect a higher chance of late payment or default.

Why the threshold matters in practice: at 660+ you can usually qualify for prime credit-card rewards, an unsecured personal loan from a major bank, and most insured mortgage products, though the exact credit rating you need for a mortgage varies by lender and insurance status. Below 660 you may still get approved, but at higher rates or with a co-signer or larger down payment (FCAC). Even a serious setback like a consumer proposal is not an automatic no; you can still get a mortgage with an R7 credit rating through a B-lender or private lender.

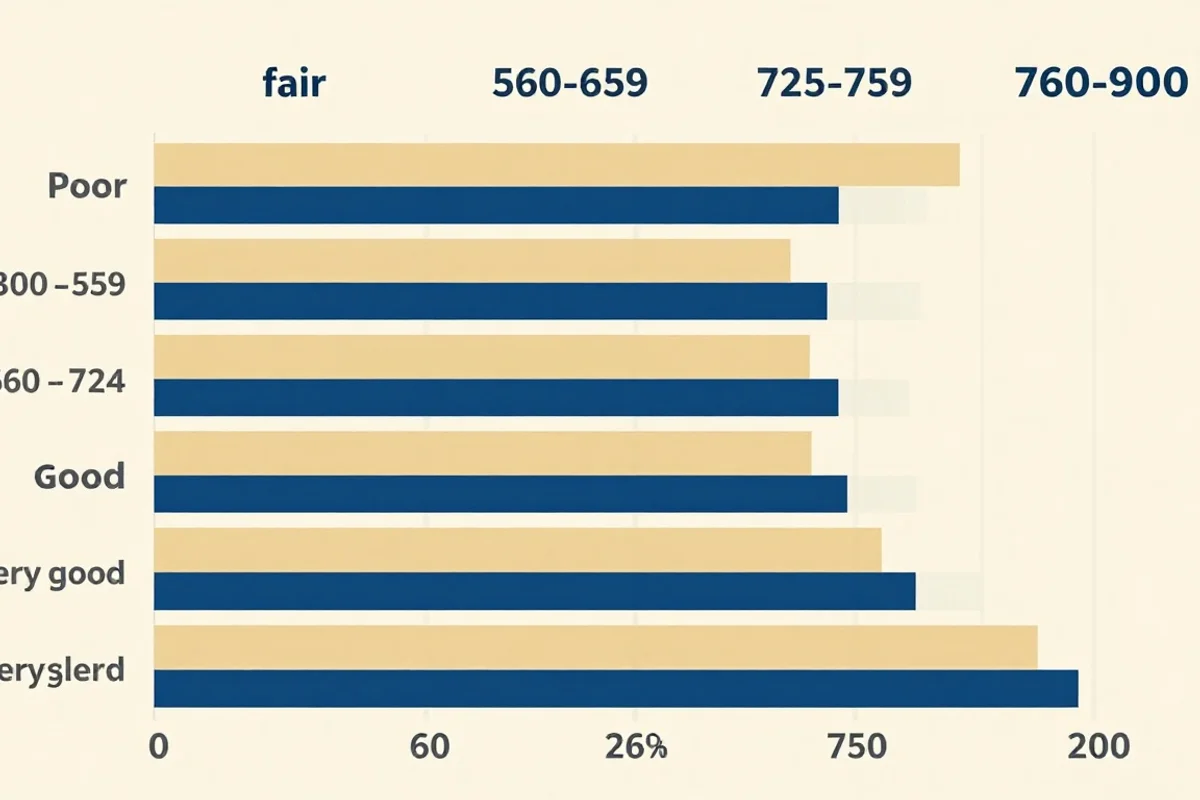

What range counts as "good" vs. "excellent"?

Canadian lenders use these informal bands. The exact thresholds vary by lender and product, but this table reflects the consensus from Equifax Canada, TransUnion Canada, and the major banks.

| Range | Label | What it typically means |

|---|---|---|

| 760 - 900 | Excellent | Best advertised rates available; pre-approval is straightforward |

| 725 - 759 | Very good | Most prime products available with minimal friction |

| 660 - 724 | Good | Mainstream qualification range; solid mortgage and loan options |

| 560 - 659 | Fair | Limited prime options; alternative lenders likely; higher rates |

| 300 - 559 | Poor | Subprime or secured products only; rebuilding required |

If you are tracking your score in a free app like Borrowell or Credit Karma, the same scale applies. Some apps display your TransUnion score, others display your Equifax score, and the two can differ by 20 to 50 points because each bureau has slightly different data. If your score recently moved without explanation, see why credit scores fall and how to diagnose the cause.

Source: Tier thresholds from Equifax Canada. Averages from Borrowell 2024 consumer data (672 overall) and Equifax Canada 2024 (765 for Canadians with a mortgage).

How does Canada's 300-900 scale compare to the US?

Canada uses the 300-900 range. The United States most commonly uses the 300-850 FICO scale. The band labels are similar, but the cutoff numbers differ. A 720 in Canada is "very good", while a 720 in the US sits at the bottom of "very good". If you are reading US-based credit advice, mentally adjust upward by about 50 points before applying it to your Canadian file.

How is a credit score calculated?

Credit bureaus weight five factors when generating your score, and payment history alone accounts for roughly 35% of the total. The remaining weight is split across credit utilization, length of credit history, credit mix, and new credit (Fair Isaac).

The exact formulas Equifax and TransUnion use in Canada are proprietary, but both rely on variants of the FICO and VantageScore models, which weight the five factors approximately as follows:

- Payment history (35%): every on-time, late, or missed payment over the past 6 to 7 years. A single 30-day late payment can drop your score by 60 to 110 points.

- Credit utilization (30%): how much of your available credit you currently use. Below 30% is generally safe; below 10% is ideal. If you have a $10,000 credit-card limit, keeping the balance under $1,000 helps your score.

- Length of credit history (15%): average age of all your accounts. Closing your oldest credit card lowers this average and can reduce your score even if you owe nothing.

- Credit mix (10%): having a healthy mix of revolving credit (cards, lines of credit) and installment credit (loans, mortgages). All cards and no installment loans is a thinner file.

- New credit (10%): recent applications and newly opened accounts. Applying for several products in a short window signals risk.

Newer financing options complicate the "new credit" picture. Buy-now-pay-later services are a common example, and many Canadians ask whether using Klarna affects their credit score.

Why payment history weighs the most

Statistical research on consumer-credit data consistently finds that past repayment behaviour is the single strongest predictor of future default. Lenders care less about how much credit you have and more about whether you actually pay what you owe, on time, every time. That is why one missed payment hurts your score more than carrying a high balance.

The good news is that payment history is also the lever you can move fastest. Setting up automatic minimum payments on every credit account stops new late marks from appearing, and existing on-time payments accumulate week over week.

What does NOT affect your credit score

A common source of confusion: several pieces of information that lenders see do not actually affect your score. Equifax Canada and TransUnion Canada both confirm the following are excluded:

- Your income, salary, or employment status

- Your job title or employer

- Your race, religion, or marital status

- Your medical history

- Your savings or chequing account balances

- Soft inquiries (when you check your own score, or a lender pre-qualifies you without a hard pull)

Lenders may consider these factors separately when underwriting a loan, but they are not part of the score itself.

How do you reach a good credit score?

The fastest path to a 660+ score is paying every bill on time, keeping credit-card balances below 30% of your limit, and avoiding new credit applications for at least six months. These three habits address the three highest-weighted factors in the scoring formula and can move a 580 score to 660+ within 12 to 18 months.

If you are starting from scratch (no credit history)

Anyone new to Canadian credit, including students, recent immigrants, and adults who have never borrowed, faces the same problem: you cannot prove repayment behaviour without first having credit. Two reliable starter products solve this:

- Secured credit card. You deposit a small amount (typically $200 to $500) as collateral, and the bank issues you a card with that limit. Use it for a small recurring expense, pay it in full each month, and after 6 to 12 months you will usually qualify for an unsecured card.

- Credit-builder loan. Some Canadian credit unions and online lenders offer small installment loans (often $500 to $2,000) where the funds are held in a savings account and released to you only after you complete the payments. Each on-time payment is reported to the bureaus.

After 6 to 12 months on a starter product, most new Canadian credit profiles reach the 600-660 range. Reaching 700+ typically takes 18 to 24 months of consistent activity.

If you are recovering from a low score

Three steps in priority order:

- Stop new damage. Set up automatic payments on every account, even if only the minimum. This freezes the bleeding from new late marks.

- Pay down high-utilization cards. A credit card at 90% utilization is dragging your score 50 to 100 points below where it would otherwise be. Bringing it under 30% is the fastest single move.

- Wait out the negative items. Most negative information stays on your Canadian credit report for 6 years from the date of the missed payment or default. Bankruptcy stays 6 years (first discharge) or 14 years (second). You cannot remove accurate negative information by disputing it; you can only outwait it.

A common myth is that closing old credit cards helps. It does not. Closing an old card reduces both your length-of-history average and your total available credit, which raises your utilization ratio. Keep old cards open with a small recurring charge if possible.

How long does it actually take?

Realistic timelines, measured from a clean monthly payment schedule:

| Starting point | Target | Typical timeline |

|---|---|---|

| 0 (no credit) | 600+ | 6 - 12 months |

| 0 (no credit) | 660+ (good) | 12 - 18 months |

| 580 | 660+ | 9 - 15 months |

| 660 | 760+ (excellent) | 18 - 36 months |

| Recovering from a missed payment | Pre-miss level | 3 - 6 months |

| Recovering from bankruptcy discharge | 660+ | 24 - 48 months |

These ranges assume no new negative items appear during the rebuild. A second missed payment resets the clock on most categories.

Why your score matters beyond loans

Your credit score affects more than whether you get approved for a mortgage or credit card. It also touches:

- Rental applications. Most Canadian landlords pull a soft credit check before approving a lease. A score under 660 can require a co-signer or larger deposit.

- Insurance premiums. Several provinces allow auto and home insurers to use credit-based insurance scoring, which can change your premium by 10 to 30%.

- Utility deposits. Bell, Rogers, Hydro One, and other utility providers may require a security deposit when your score is below their threshold.

- Employer background checks. Some financial-services and government roles include a credit check as part of hiring. The employer cannot see your score, but they can see negative items on your report with your written consent.

The score is not destiny. It can be rebuilt. But at any given moment it acts as a gatekeeper to almost every form of credit and many adjacent decisions, so understanding the threshold and the three-lever path to a good score is one of the highest-return pieces of personal-finance knowledge a Canadian can have.