What is the max credit score?

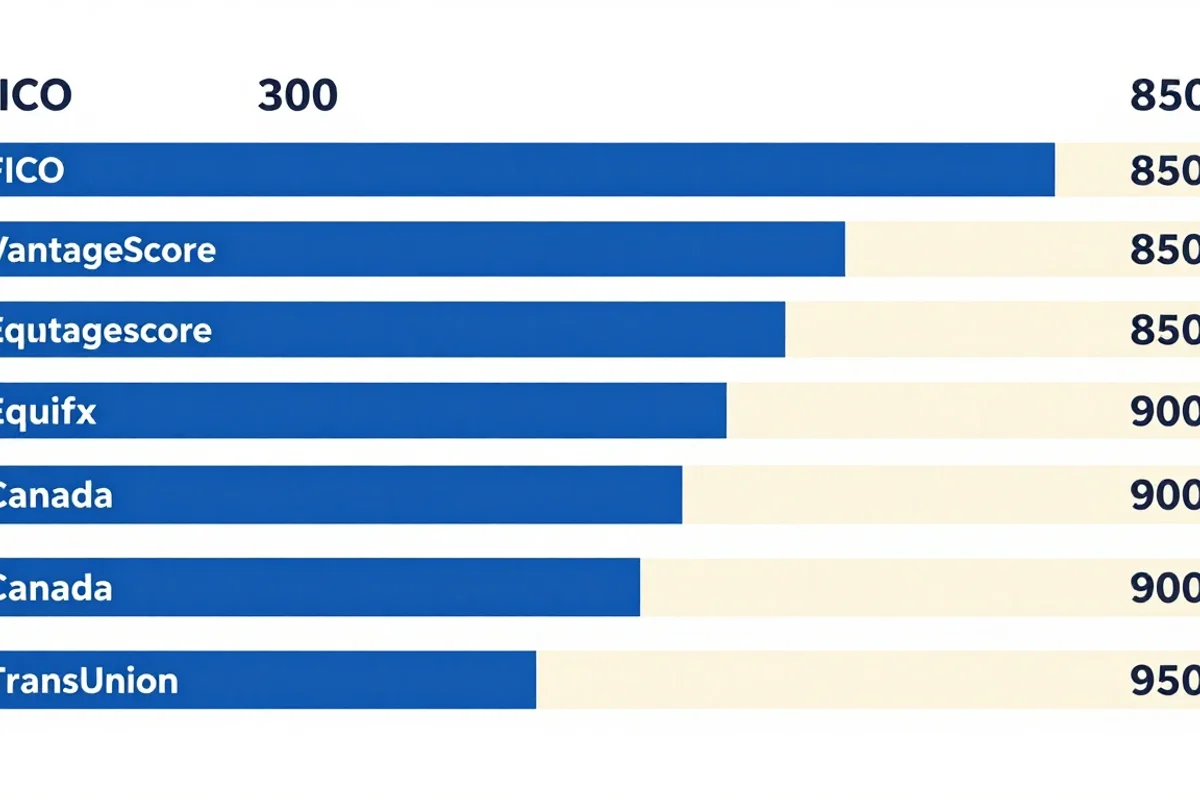

The max credit score is 850 on the US FICO and VantageScore scales, and 900 on the Canadian Equifax and TransUnion scales. Which number applies to you depends on which country you are borrowing in and which credit bureau is reporting on you (Fair Isaac, Equifax Canada).

In practice, the difference between the US and Canadian maximums matters less than where you fall within the lender's "excellent" band. A US borrower at 800+ and a Canadian borrower at 800+ both qualify for the best advertised rates on a mortgage, auto loan, or credit card. Going from 820 to 850 (or from 820 to 900) earns no additional rate discounts at most lenders. The math of the scoring model continues, but the practical reward stops.

Why the maximums differ: the credit-bureau industry never standardized a single scale. FICO, the dominant US scoring model, was built around the 300-850 range starting in 1989. Equifax Canada and TransUnion Canada each adopted a 300-900 range for their Canadian consumer products. VantageScore later launched its own US 300-850 scale to compete with FICO. None of the bureaus or models share a common ceiling.

Quick reference: max scores by model and country

| Model / bureau | Country | Range | Max |

|---|---|---|---|

| FICO 8 | United States | 300 - 850 | 850 |

| FICO 9 | United States | 300 - 850 | 850 |

| FICO 10 / 10T | United States | 300 - 850 | 850 |

| VantageScore 3.0 / 4.0 | United States | 300 - 850 | 850 |

| Equifax Canada (consumer) | Canada | 300 - 900 | 900 |

| TransUnion Canada (consumer) | Canada | 300 - 900 | 900 |

| FICO Auto Score 8 (industry-specific) | United States | 250 - 900 | 900 |

| FICO Bankcard Score 8 (industry-specific) | United States | 250 - 900 | 900 |

The industry-specific FICO variants like Auto Score and Bankcard Score use the 250-900 range, but consumer-facing scores from your bank's app or a free service like Credit Karma always use the 300-850 (US) or 300-900 (Canada) range.

Source: Experian 2025 consumer credit data. Tier shares derived from Experian's published cumulative distribution (1.76% at 850, 22.8% at 800+, 48.1% at 750+, 70% at 670+, 84% at 580+).

How rare is a perfect credit score?

About 1.5% of US consumers with a FICO score reach 850, and fewer than 1% of Canadians reach 850+ on the Equifax scale. A perfect score is statistically rare because the model is calibrated so that small imperfections (one slightly higher utilization month, one new account opened in the last 12 months, one credit card under three years old) prevent the maximum even when the file is otherwise spotless (Experian).

The exact share moves slightly each year. In recent reports, Experian has placed the 850-FICO share at 1.31% to 1.74% of US scoreable consumers. Equifax Canada has reported a similar concentration at the top of its 300-900 scale, with most Canadians clustered between 700 and 800. For whether anyone actually reaches the Canadian 900 ceiling, see is a 900 credit score possible and the highest credit score possible in the US. For the tier cutoffs and what each band actually qualifies you for, see what counts as a good credit score.

What separates a 780 from an 850?

Not behaviour. Both scores are "excellent" and qualify the borrower for the same products at the same rates. The difference is data depth.

A 780 typically reflects a clean file with 5 to 10 years of history. An 850 typically requires:

- A credit history of 15 years or longer.

- At least 4 to 6 active accounts in good standing, with a mix of revolving and installment credit.

- Zero late payments on any account, ever, in the bureau's full reporting window.

- Credit utilization under 5% on every revolving account when the bureau pulls the score.

- No new credit applications in the past 12 to 24 months.

- All cards over 3 years old (or older), with at least one over 10 years old.

Each of these factors moves the score by a few points. Reaching the max requires hitting all of them at the same moment the bureau generates the score, which is why even the most disciplined borrowers often hover at 820-840 instead of touching 850.

Why the max barely matters once you cross 800

Above roughly 800, most US lenders treat all scores as equally excellent and offer the same rate to a 800 borrower as to an 850 borrower. Canadian banks behave the same way around 800 to 900: their published rate cards do not improve once a borrower clears the "excellent" tier.

This matters because it changes the practical answer to "should I optimize for a perfect score?" For most people the answer is no. Once you are at 760+, you have already captured every rate advantage your score can give you. Pushing further is mostly vanity: it does not save you money on your next mortgage or car loan.

Where chasing the max actually pays off

Two narrow situations:

- Mortgage shopping in a thin market. A small handful of US lenders give a 0.05% to 0.10% rate concession at 780+, and a smaller handful give another tiny concession at 800+. On a 30-year US$500k mortgage that adds up, but it is a niche benefit. Most major US and Canadian banks do not offer it.

- Premium credit-card approvals. Some invitation-only cards (top-tier US Amex products, Canadian World Elite Mastercard variants) ask for an excellent file as part of underwriting. Hitting 800+ rather than 760+ raises your odds of approval, though income and existing relationship usually matter more than the score number itself.

Outside those two cases, the marginal score points above 800 are not worth chasing.

How do you reach the max credit score?

Reaching 850 (US) or 900 (Canada) requires a long, clean, low-utilization file built over a decade or more, with zero late payments and very few new accounts. The five FICO factors all need to be at or near their best simultaneously when the score is generated.

The realistic path looks like this:

- Years 1 to 2. Open a starter card or credit-builder loan. Pay every bill on time. Most files reach 660-700 in this window.

- Years 3 to 5. Add a second or third credit product to build mix. Keep utilization under 30% on every card. Score typically reaches 720-760.

- Years 6 to 10. Maintain the same accounts. Keep utilization under 10%. Avoid new credit applications outside actual need (a mortgage, an auto loan, one new card every few years). Score typically reaches 780-820.

- Years 10+. A long history starts to compound. Utilization at under 5%, no new accounts, zero late payments. Score typically reaches 820-850 (US) or 850-900 (Canada).

A single missed payment in the rebuild window resets several factors. Most bureaus weight a 30-day late payment heavily for 12 to 24 months, and the record stays on file for 6 to 7 years. There is no shortcut.

What does NOT help reach the max

A handful of common myths to discard:

- Carrying a small balance to "show activity". False. Reporting a $0 statement balance does not hurt your score, and reporting a balance increases utilization. Pay in full.

- Closing old credit cards. Closing your oldest card lowers your average account age and reduces total available credit, which raises utilization. Both push your score down.

- Frequently checking your own score. Soft inquiries (the kind your bank app or a free service uses) do not affect your score. Hard inquiries (when you apply for new credit) lower it by a few points temporarily.

- Disputing accurate negative information. Bureaus will not remove accurate data. You can only outwait the 6 to 7 year reporting window.

- Paying for credit-repair services. They cannot do anything you cannot do yourself for free. Most reputable advice (FCAC, CFPB) warns against them.

What about scoring models that lenders use behind the scenes?

When a Canadian or US lender pulls your credit during a real application, they often use an industry-specific FICO variant rather than the consumer-facing score you see in your bank app. The auto-loan industry typically uses FICO Auto Score 8 (250-900). Mortgage lenders in the US still pull FICO 2, 4, and 5 (the "old" classic models, 300-850). Card issuers often use FICO Bankcard Score 8 (250-900). Your number on each of these can differ from your free-app score by 20 to 60 points, even though the underlying credit data is identical. For why those versions diverge, see whether a FICO score is the same as a credit score. The max on each model is what that model is calibrated to, not what your bank's mobile app shows.

Should you aim for the max, or just for "excellent"?

For most people, the answer is to aim for the "excellent" band (760+ in the US, 760+ in Canada) and stop optimizing. That captures every rate advantage available to consumer borrowers. Going from 760 to 850 (or 900) takes years of incremental discipline for almost no additional financial reward.

The exception is if you find the score itself motivating. Treating credit as a long-term game where the number reflects financial discipline is psychologically useful, even if the dollars-and-cents return on going from 820 to 850 is essentially zero.

The number is a signal, not the goal. The goal is a financial position where credit is a tool you choose to use, not a constraint you have to manage around.