What is an underwriter in a mortgage loan?

A mortgage underwriter is the lender's risk-assessment professional (or automated decision system) who reviews a complete loan file against the lender's credit policy and the specific loan program's rules, then decides whether to approve the loan, decline it, or counter-offer with revised terms. The underwriter is the gatekeeper between a signed application and funded loan, the person at the center of home loan underwriting. The Consumer Financial Protection Bureau's home-buying guide describes the role plainly: the underwriter "evaluates whether the loan is a good fit" using documented standards published by the program (FHA, VA, conventional Fannie / Freddie, jumbo) and the lender's own overlays (CFPB).

The underwriter is not the loan officer. The loan officer takes the application, helps the borrower understand programs, gathers documents, and quotes rates. Once the application is complete, it moves to the underwriting desk. The underwriter does not negotiate terms; they apply the rules. This separation exists because the loan officer is paid on closed loans (so they have an incentive to push approvals) while the underwriter is paid on accurate decisions (so they have an incentive to apply policy consistently).

Why the role matters in practice: the same borrower with the same income and the same FICO can get different decisions from different lenders because the underwriter at each lender works against different overlays. A 620 FICO that clears underwriting at Lender A may fail at Lender B because Lender B's overlay sets the floor at 660. Understanding what the underwriter is actually doing is the borrower's path through the maze.

What is the difference between an underwriter and a mortgage broker?

A mortgage broker is an independent intermediary who shops the application across multiple lenders to find the best fit. A mortgage underwriter is employed by (or contracted to) a single lender and decides whether to fund that lender's loan. Brokers do not approve loans; they pre-qualify and route. Underwriters approve, decline, or counter-offer.

What does a mortgage underwriter do?

The underwriter verifies the borrower's income, debt, credit, assets, and property; calculates the qualifying ratios; checks compliance with the specific loan program; and issues a written decision. The work splits into four phases that run sequentially over 5 to 15 business days for a typical clean US mortgage file (Fannie Mae).

The underwriter's checklist on a typical mortgage file:

- Income verification. Match pay stubs, W-2s, and (for self-employed borrowers) two years of tax returns and the most recent profit-and-loss statement. Call employers for verbal verification of employment within 10 days of closing.

- Debt and credit review. Pull a tri-merge credit report from Equifax, Experian, and TransUnion; calculate the borrower's debt-to-income ratio; flag any new tradelines, late payments, collections, or derogatory items.

- Asset verification. Review 60 to 90 days of bank statements for the down payment, gift-letter documentation for any gifted funds, and proof of cash reserves.

- Property review. Read the appraisal report (and order a second if the value is contested), verify the title is clear, confirm the property tax status, and confirm hazard insurance is in place at closing.

- Program compliance. Confirm the file meets the specific loan program's rules: FHA's single-family handbook for FHA loans, the Fannie Mae or Freddie Mac selling guides for conventional, VA's lender handbook for VA, etc.

- Decision. Issue conditional approval (yes, IF), final approval (yes, fund), denial (no, with HMDA reason code), or counter-offer (yes, but at different terms).

The underwriter is paid to be consistent, not creative. Their notes on the file must explain why each decision was made, citing the specific guideline that applies. This documentation matters at the time of the decision and matters again if the loan ever ends up in a securitization audit, a CFPB exam, or a fair-lending review.

What is the underwriter looking for in your bank statements?

The underwriter reads bank statements for three reasons: confirming the down-payment source (the funds have been in the account for 60 to 90 days, or are documented as a gift); flagging large unusual deposits (any deposit above 50% of monthly income that cannot be sourced is a red flag); and confirming reserves (months of mortgage payments the borrower can cover post-closing if income stops). Borrowers who move large sums between accounts during the underwriting window often trigger fresh document requests; the cleaner the 90-day picture, the faster the file clears.

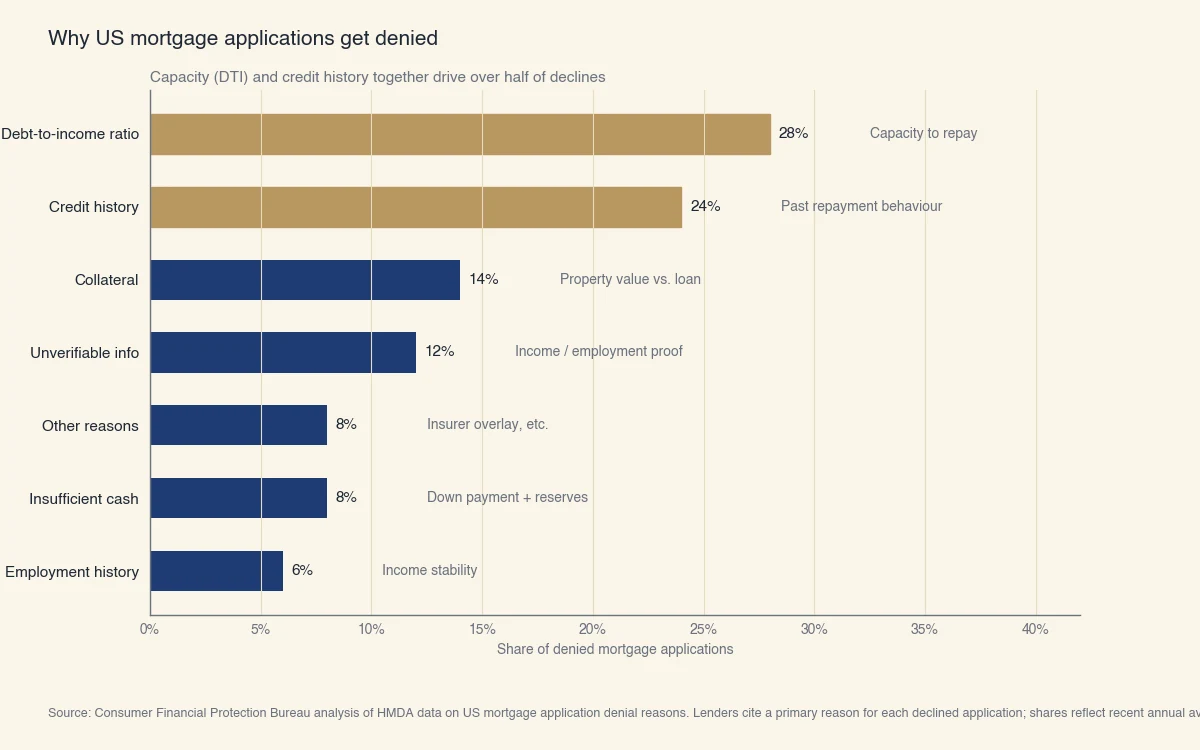

What does the underwriter check, in order of weight?

Mortgage application denials reveal exactly what underwriters weight most: debt-to-income (28% of denials), credit history (24%), collateral / property (14%), unverifiable info (12%), and cash reserves (8%). The Federal Financial Institutions Examination Council publishes these denial reasons annually in HMDA data, and the distribution is remarkably stable from year to year.

Source: Consumer Financial Protection Bureau analysis of HMDA data on US mortgage application denial reasons. Lenders cite a primary reason for each declined application; shares reflect recent annual averages.

The chart maps directly onto the underwriter's checklist. Each denial reason corresponds to one of the items the underwriter verified and rejected:

| Denial reason | What the underwriter found |

|---|---|

| Debt-to-income too high | Front-end DTI > 36% or back-end DTI > 43-50% |

| Credit history | FICO below program minimum, recent late payments, collections, bankruptcy in look-back window |

| Collateral | Appraisal came in below contract; loan-to-value too high |

| Unverifiable info | Income or employment could not be verified within program rules |

| Insufficient cash | Down payment + reserves below program minimum |

| Employment history | Less than two years of stable employment, recent job change |

| Insurance denied | FHA / VA / PMI insurer declined the file |

A borrower can pre-empt the most common denial reasons by computing their own DTI, pulling their own tri-merge credit report (myFICO sells the same model the lender uses), and bringing 90-day bank statements to the first conversation with a loan officer. Most denials are not surprises; they are preventable through a tighter pre-application package.

What is debt-to-income (DTI)?

The debt-to-income ratio has two flavors that mortgage underwriters compute side by side:

- Front-end DTI: monthly housing costs (principal, interest, taxes, insurance, HOA) divided by gross monthly income. The conventional cap is 28% to 36%.

- Back-end DTI: all monthly debt obligations (housing plus credit cards, auto, student loans, child support) divided by gross monthly income. Caps run 43% for qualified mortgages, up to 50% with compensating factors for FHA.

A borrower making $10,000 gross per month, with a target $2,400 monthly housing payment and $700 of other monthly debts, has a front-end DTI of 24% and a back-end DTI of 31%. Both are comfortably within the bands. The same borrower with $1,500 of other monthly debts has a back-end DTI of 39%, still inside conventional limits but closer to the threshold and more sensitive to property tax surprises.

What is the difference between automated and manual mortgage underwriting?

Automated underwriting runs the file through a rules engine and returns a decision in minutes; manual underwriting puts a human underwriter on the file and takes 1 to 5 business days. The two giants in US automated underwriting are Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA). Almost every conventional, FHA, and VA loan in the US passes through one of these systems first.

Decision tree:

- Approve / Eligible through DU or LPA → underwriter still does a final review but the decision is essentially confirmed.

- Refer with caution → manual underwriting required.

- Refer / Eligible (with caveats) → manual review of the specific flagged items.

- Caution → likely decline; manual underwriter looks for compensating factors.

Manual review is required when the file falls outside the system's tolerances. The most common manual triggers:

- Credit score below the lender's automated minimum (typically 580 or 620)

- Self-employed or commission-based income

- Non-occupying co-borrower

- Non-standard property type (rural, leasehold, condotel)

- Recent credit events (bankruptcy, foreclosure) within the look-back window

Manual underwriting can approve a wider range of files than automated underwriting because the human underwriter weighs compensating factors. The trade-off is judgment risk: two manual underwriters can reach different conclusions on the same file. Automated decisions are repeatable; manual decisions are not.

What is conditional vs. final mortgage approval?

Conditional approval is the underwriter's commitment to fund the loan IF a list of remaining conditions is met; final approval ("clear to close") comes only after every condition has been cleared and the file is moving to closing scheduling. Most mortgage applicants reach conditional approval within 1 to 2 weeks of submitting a complete file, and final approval 1 to 3 weeks later, for a total of 25 to 45 days from application to funding.

Typical conditions on a US mortgage approval letter:

- Satisfactory appraisal ordered by the lender, paid by the borrower (typically $500-$700)

- Title commitment with clear title, no unresolved liens, documented easements

- Hazard insurance binder effective on the closing date

- Most recent paycheck stub within 10 days of closing

- Verbal verification of employment within 10 days of closing

- Gift letter signed by any donor for gifted down-payment funds

- Sale of departure residence, if applicable

- Mortgage insurance approval for FHA, VA, USDA, or conventional loans below 20% down

What is "clear to close"?

"Clear to close" (CTC) is the underwriter's final-approval status: every condition has been cleared and the file is ready for the closing department to schedule the signing. From CTC, closing typically follows 3 to 7 business days later because of the federal Closing Disclosure rule (TRID), which requires the borrower to receive the final Closing Disclosure form at least 3 business days before signing.

Borrowers should treat CTC as the milestone that means the loan is real. Before CTC, the loan can still be declined for any reason. After CTC, the loan can still be declined if the borrower triggers a "material change" (loses employment, takes on new debt, undergoes a credit-score drop) before closing. Avoiding new credit applications, large purchases, and job changes between application and closing is the standard "do not move" advice every loan officer gives.

How does mortgage underwriting differ across loan programs?

The underwriter applies a different rulebook depending on the loan program: FHA's Single Family Housing Policy Handbook for FHA, the VA Lender Handbook for VA, the Fannie Mae Selling Guide and Freddie Mac Single-Family Seller / Servicer Guide for conventional, and program-specific guides for USDA Rural and jumbo loans. Each rulebook covers the same five-bucket decision (income, debt, credit, assets, property) but with different thresholds and different documentation standards.

The most consequential differences across programs:

| Dimension | FHA | VA | USDA Rural | Conventional | Jumbo |

|---|---|---|---|---|---|

| Min FICO | 580 (3.5% down) | None set; lender 580+ | None; lender 640+ | 620 | 700+ |

| Max DTI | 50%+ with compensating | 41% guideline; 60%+ possible | 41% / 29% | 43-50% | 43% |

| Down payment | 3.5% | 0% | 0% | 3-20% | 10-20%+ |

| MI / insurer | FHA MIP | VA funding fee | USDA fee | PMI if <20% down | None |

| Property type | Most | Most + condotel restrictions | Rural areas only | Most | Most |

A borrower with marginal credit and limited cash will find FHA underwriting most accommodating. A borrower with strong credit but limited liquidity will find VA (if eligible) or USDA most accommodating on down payment. Conventional and jumbo target stronger files at lower rates.

Why do underwriting standards vary by lender even within the same program?

Lenders add their own overlays on top of the program's rules to limit risk. HUD's published FHA minimum is 500 with 10% down, but most FHA-approved lenders raise their internal floor to 580 or 620. The lender's overlay reflects their own risk appetite, their loss experience on prior FHA loans, their cost of insurance against early defaults, and their relationship with FHA-insurer Ginnie Mae securitization vehicles. For the broader process of underwriting beyond mortgages, see what is underwriting. For the score thresholds tied to each loan program, see what credit score is needed to buy a house.

The practical consequence: a borrower at 580 should expect to shop multiple FHA-approved lenders. The same file can be denied at one and approved at another based on the overlay difference, not on any difference in the file itself.