Are interest rates going down in Canada?

No. As of July 2026, interest rates in Canada are not going down. The Bank of Canada has held its policy interest rate at 2.25% since October 2025 and kept it there again at its March 2026 decision (Bank of Canada). The policy interest rate is the Bank of Canada's target for the overnight rate, the rate that sets the floor for what banks charge each other and, in turn, what you pay on variable loans and lines of credit.

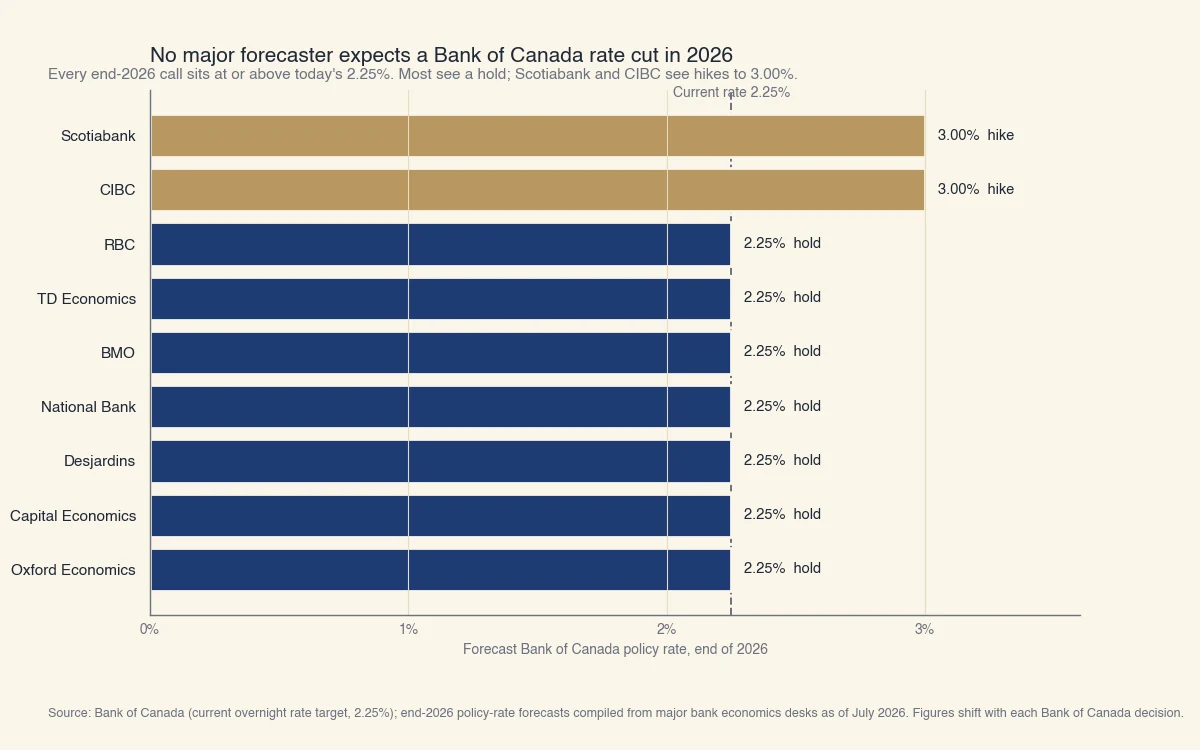

The bigger surprise for anyone searching this question is the direction of the risk. After two years of falling rates, the next move is now more likely to be a hike than a cut. Every major bank economics desk expects the policy rate to hold at 2.25% or rise in 2026. Not one forecasts a cut below the current level.

Here is where things stand in mid-2026:

- Policy rate: 2.25%, unchanged since October 2025

- Prime rate at the major banks: about 4.45%

- Headline inflation: running near 2.8% to 3.2%, above the 2% target, on higher energy prices (Statistics Canada)

- The market's read: a hold at the next decision, with hike odds building later in the year

Why you might expect a cut, and why it is not coming

If you assumed rates were still falling, you are working from a 2025 mental model that no longer holds. The Bank of Canada cut its policy rate repeatedly through 2024 and into 2025, taking it down to 2.25% as inflation cooled from its 2022 highs. That easing cycle is over. The Bank paused once inflation neared its 2% target, and a 2026 shock changed the picture entirely.

The trigger is energy. A supply disruption pushed oil and gasoline prices sharply higher in 2026, and that fed straight into headline inflation. When inflation runs above the 2% target, the Bank of Canada's job is to hold rates high enough to bring it back down, not to cut (Bank of Canada). On top of that, cross-border tariffs have raised the cost of many imported goods, adding a second source of price pressure.

So the reader's instinct ("rates were dropping, surely they keep dropping") is understandable, but the conditions that justified the cuts have reversed. Inflation is no longer falling toward target on its own, which removes the case for further easing and builds the case for a possible hike.

What still could bring rates down

A cut is not impossible, it is just not the base case. Rates would fall again if inflation drops back to 2% and stays there, or if the economy weakens enough that the Bank needs to support growth. Canadian GDP contracted late in 2025, so a sharper slowdown is the main scenario that would put cuts back on the table. Absent that, the Bank has little reason to ease.

What the major forecasters actually expect for 2026 and 2027

The forecast consensus is unusually one-directional: hold now, and if anything, hike later. Among the big banks and independent economics shops, most expect the Bank of Canada to keep the rate at 2.25% through 2026, while Scotiabank and CIBC are the hawkish outliers calling for hikes to 3.00% by year-end.

Source: Bank of Canada (current overnight rate target, 2.25%); end-2026 policy-rate forecasts compiled from major bank economics desks as of July 2026. Figures shift with each Bank of Canada decision.

Looking further out, several desks pencil in gradual hikes in 2027, taking the rate toward 2.75% or 3.00% as the economy stabilizes. The exact path is uncertain and every forecast moves with the next inflation report, but the shape is consistent: flat this year, drifting up next year. The one thing no mainstream forecast contains is a return to the sub-2% rates of the pandemic era.

| Forecaster | End of 2026 | Direction |

|---|---|---|

| RBC, TD, BMO, National Bank, Desjardins | 2.25% | Hold |

| Capital Economics, Oxford Economics | 2.25% | Hold |

| Scotiabank, CIBC | 3.00% | Hike |

Are home mortgage rates going down in Canada?

Home mortgage rates are not falling either, and the two types of mortgage rate move for different reasons. Understanding which one you have tells you what to expect.

Variable mortgage rates are tied directly to the Bank of Canada policy rate through your lender's prime rate. Because the policy rate is holding at 2.25%, prime is steady near 4.45%, so variable rates are flat. If the Bank hikes, your variable rate rises within days of the decision.

Fixed mortgage rates do not follow the policy rate at all. They track Government of Canada bond yields, which reflect where the bond market expects rates to sit over the term. Those yields have edged up in 2026 as the market priced out cuts and priced in the inflation risk, so fixed rates are steady to slightly higher, not lower. The five-year Government of Canada yield sits near 3.1%, which keeps typical five-year fixed offers in the high-3% to mid-4% range.

The short version: whether you are looking at variable or fixed, there is no meaningful downward move to wait for in 2026.

What a rate hold costs you in dollars

The practical cost of "no cut" is the relief you were counting on but will not get. Many borrowers held off refinancing or stayed in a variable rate expecting one or two more cuts to lower their payment. On a $500,000 mortgage, that missing half-point is real money.

Here is a worked comparison on a $500,000 mortgage amortized over 25 years (Sphera Credit computation, standard monthly amortization):

| Scenario | Rate | Monthly payment | Vs today |

|---|---|---|---|

| The cut you hoped for | 3.70% | about $2,557 | -$138 / month |

| Today's rate (hold) | 4.20% | about $2,695 | baseline |

| A hike to prime +0.75% | 4.95% | about $2,909 | +$214 / month |

Two takeaways. First, waiting for the cut cost you nothing to hope for but delivered nothing: the payment you wanted (roughly $2,557) never arrived, and you are paying about $138 a month more than that. Second, the more important number is the downside: if the Bank hikes 0.75% and prime rises with it, a variable holder's payment climbs by roughly $214 a month, about $2,600 a year. The asymmetry matters. There is little upside left from cuts and real downside from hikes.

What this means for you

"Are rates going down" has a different answer depending on how you borrow or save. Use this table to find your situation.

| Your situation | What a flat-to-higher rate means | What to consider |

|---|---|---|

| Variable-rate mortgage holder | No payment relief is coming; budget for flat or higher payments | Stress-test your budget for prime rising toward 5.2% |

| Renewing a mortgage in 2026 | You will likely renew above your pandemic-era rate, not below | Shop the renewal early and compare a shorter term |

| Prospective home buyer | Waiting for cuts is no longer a winning strategy | Qualify on today's rate, do not count on future cuts |

| Carrying a line of credit or card | Variable borrowing costs stay high | Prioritize paying down variable-rate balances |

| Saver or GIC holder | Higher-for-longer works in your favour | Consider locking longer terms while yields hold |

If you are a variable-rate mortgage borrower, the key point is that your rate moves with the Bank of Canada, so a hold means your payment holds and a hike raises it. If you hold a fixed-rate mortgage, your rate is locked for your term, but your renewal rate depends on Government of Canada bond yields, which have edged up in 2026. Either way, planning around a rate cut is planning around an event most forecasters do not expect (FCAC).

When is the next Bank of Canada rate decision?

The Bank of Canada sets its policy rate on eight fixed dates each year, and each one is the next chance for the rate to move. The Bank publishes the full schedule in advance, so you can plan renewals and rate locks around it (Bank of Canada).

Watch two things ahead of each decision: the Consumer Price Index report from Statistics Canada, which tells you whether inflation is cooling or heating, and the Bank of Canada's own statement, which signals how it reads the economy. When inflation prints above target, expect a hold or a hike. It would take several months of inflation falling back toward 2%, or a clear economic downturn, before a cut becomes the likely outcome.

For borrowers, the takeaway is simple. Do not build your plan around a Canadian rate cut in 2026. Build it around a rate that holds near 2.25%, with a real chance of moving higher. That is where the Bank of Canada, the bond market, and the major bank forecasters all point.