What is the difference between interest rate and APR?

The interest rate is the cost of borrowing the principal, expressed as an annual percentage; the APR (annual percentage rate) is that same interest rate plus most upfront lender fees, re-expressed as a single annual percentage. APR is always equal to or greater than the interest rate, never lower. Federal law requires both numbers to appear side by side on every consumer loan disclosure under Regulation Z, the rule that implements the Truth in Lending Act (CFPB).

Here is the practical version. The rate a lender advertises, the rate on a rate-shopping site, and the rate on the first-call quote is the interest rate. It drives your monthly payment. The APR is the number you use to compare two offers, because it folds the fees into one figure.

| Interest rate | APR | |

|---|---|---|

| What it measures | Cost of borrowing the principal | Interest rate plus most upfront fees |

| Includes fees? | No | Yes (origination, points, mortgage insurance) |

| Sets your monthly payment? | Yes | No |

| Best used for | Calculating the payment | Comparing two loan offers |

| Always higher? | It is the floor | Equal to or above the interest rate |

A worked example makes the gap concrete. Take a $300,000 30-year fixed mortgage at a 6.50% interest rate with $6,000 in upfront finance charges (origination plus points). The interest rate sets the monthly principal-and-interest payment at about $1,896. The APR, which spreads that $6,000 across the full 30-year term, works out to roughly 6.70%. Same loan, two different numbers: 6.50% is what you pay each month on, 6.70% is what it truly costs once the fees are counted.

This page explains the three rate numbers you meet as a borrower and a saver, why APR sits above the interest rate, and one thing almost no one tells you: the disclosed APR quietly assumes you keep the loan for its entire term. For a deeper look at the yes-or-no framing and a longer list of comparison mistakes, see is APR the same as interest rate.

Interest rate vs APR vs APY: what is the difference?

Interest rate, APR, and APY are three annual percentages that answer three different questions: the interest rate is the base cost, APR adds borrowing fees, and APY adds compounding on savings. People confuse them because all three are quoted as an annual percent, but two of them describe borrowing and one describes earning.

- Interest rate is the base rate. On a loan it is your borrowing cost before fees; on a savings account it is the rate before compounding.

- APR (annual percentage rate) is a borrowing number. It takes the interest rate and adds the lender's upfront fees, without compounding. You see it on mortgages, auto loans, personal loans, and credit cards.

- APY (annual percentage yield) is a saving number. It takes the interest rate and adds the effect of compounding over a year, without any fees. You see it on savings accounts, certificates of deposit, and money-market accounts.

The clean way to hold the three apart:

| Number | Side | Adds to the base rate | Where you see it |

|---|---|---|---|

| Interest rate | Both | Nothing (it is the base) | Every rate quote |

| APR | Borrowing | Upfront fees | Loans, credit cards |

| APY | Saving | Compounding | Savings, CDs, money-market |

Two short examples. A $10,000 three-year personal loan at a 12% interest rate with a $400 origination fee carries an APR near 14.9%, because the fee is folded in. A savings account paying a 4.90% interest rate compounded daily carries an APY near 5.02%, because you earn interest on your interest (Regulation DD). The rate is the same starting point; the fee pushes APR up on the loan, and compounding pushes APY up on the savings.

Banks are required to disclose APY on deposit accounts under Regulation DD (the Truth in Savings Act), the savings-side counterpart to Regulation Z on the borrowing side. That is why a savings ad leads with APY and a loan ad leads with APR: each rule forces the more honest number to the front for that product.

Why is APR higher than the interest rate?

APR sits above the interest rate whenever a loan carries upfront fees that Regulation Z classifies as prepaid finance charges, because APR averages those fees across the loan term while the interest rate ignores them. A loan with no such fees has an APR equal to its interest rate. A loan with heavy upfront fees has a noticeably higher APR.

The fees that raise APR are the ones the lender controls:

- Origination charges. The lender's fee to set up the loan, usually 0.5% to 1% of the amount borrowed.

- Discount points. Optional upfront payments that buy down the interest rate. Each point costs 1% of the loan amount. Points lower your rate but raise your APR. The trade-off math is in how much it costs to buy down a rate.

- Mortgage broker fees. Broker compensation paid by the borrower upfront flows into APR.

- Mortgage insurance. FHA upfront and annual premiums, and conventional private mortgage insurance, flow into APR.

The fees that do NOT raise APR are third-party charges the lender passes through:

- Appraisal fee

- Credit report fee

- Title insurance and title search

- Recording fees and transfer taxes

- Property tax and homeowners insurance escrows

The dividing line is set in Regulation Z: charges the lender imposes or controls go into the APR, while third-party pass-through charges stay out (Regulation Z, 12 CFR 1026). Regulation Z also holds lenders to an APR accuracy tolerance of one-eighth of one percentage point on most loans, which is why every lender's APR on the same loan lands in the same narrow band.

When are the interest rate and APR the same?

The interest rate and APR are equal when a loan has no APR-includable fees, which is the normal case for credit cards. A credit card charges no origination fee and no closing costs, so its purchase APR is simply the periodic interest rate annualized. This is why the CFPB and most card issuers use "APR" and "interest rate" interchangeably for cards (CFPB). Mortgages are the opposite: they almost always carry origination or other prepaid charges, so their APR sits above the interest rate.

One card wrinkle worth knowing: most cards give you a grace period, so you pay no interest at all on purchases if you clear the statement balance in full each month. The advertised purchase APR only bites when you carry a balance.

Does APR tell the whole story?

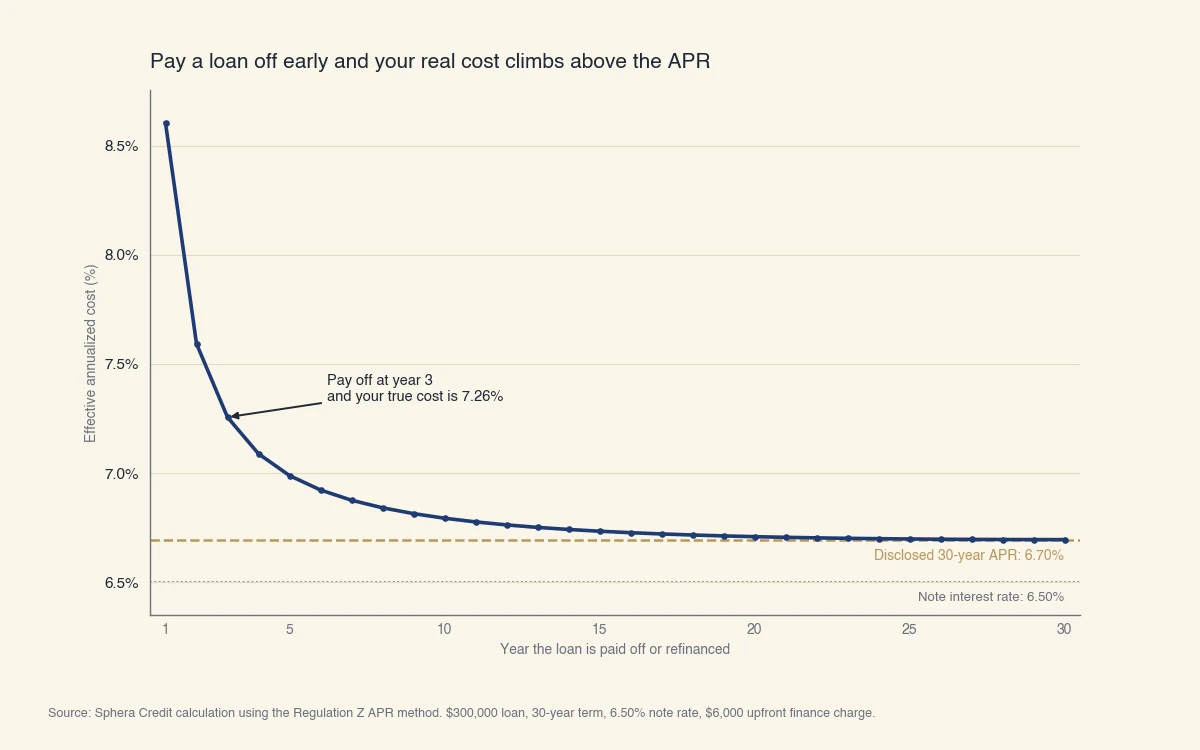

No. The disclosed APR assumes you hold the loan for its full term, so if you pay it off or refinance early, your true annualized cost is higher than the APR. This is the single most useful fact about APR, and it is missing from almost every explainer. APR spreads the upfront fees across the entire term. Retire the loan sooner and those same fixed fees get charged against far fewer years, which drives the real cost up.

The chart below traces the effective annualized cost of the same $300,000 loan at 6.50% with $6,000 in fees, plotted against the year the borrower pays it off:

Source: Sphera Credit calculation using the Regulation Z APR method. $300,000 loan, 30-year term, 6.50% note rate, $6,000 upfront finance charge.

At the full 30-year term the effective cost equals the disclosed APR of 6.70%. Pay the loan off at year seven and the true cost climbs to about 6.88%. Pay it off at year three and it reaches roughly 7.26%, well above both the 6.50% interest rate and the 6.70% APR. The fees did not change; the number of years to absorb them did.

This matters because few borrowers actually keep a 30-year mortgage for 30 years. Most sell or refinance well before term. Regulation Z still requires the APR to be computed over the full original term, because that is the only assumption that does not depend on each borrower's plans (Regulation Z). The disclosure is standardized and useful, but it is a full-term number. If your real holding period is short, treat the interest rate plus the upfront fees as the truer cost, not the APR.

How do you use interest rate and APR to compare loans?

Use the interest rate to know your payment, and use APR to compare two offers of the same type and term, then adjust for how long you actually plan to keep the loan. APR is the right comparison signal for loans you will hold to maturity. For shorter plans, the interest rate and the fee total matter more than the single APR figure.

A simple decision guide for mortgages:

| Your plan | The number to trust |

|---|---|

| Keep the loan to full term | APR |

| Refinance in 3 to 5 years | Interest rate, then weigh the fees separately |

| Sell within 2 to 3 years | Interest rate; low-rate, high-fee "buydown" loans usually lose |

| Adjustable-rate loan | Today's interest rate plus the rate caps; APR only estimates |

Every mortgage applicant receives a CFPB Loan Estimate within three business days of applying. It places the interest rate and the APR on the same page, along with the total fees, so you can compare offers directly (CFPB). Get Loan Estimates from at least three lenders, line them up, read the APR for the comparison signal, and read the total-cost columns for the full bill.

Two habits keep you out of trouble. First, compare like with like: a 15-year and a 30-year APR are not directly comparable, because the same fees amortize over different lengths. Second, do not confuse a rate-shopping quote with a real offer; the advertised APR usually assumes a high credit score and a large down payment. To work the underlying math yourself, see how to calculate an interest rate and what a nominal interest rate is.