How do interest rate hikes affect your mortgage?

An interest rate hike raises the cost of a variable-rate mortgage almost immediately and raises the cost of a fixed-rate mortgage at renewal, because the two mortgage types are priced against two different rates. When the Bank of Canada raises its policy rate, lenders raise their prime rate, and variable mortgages are priced as prime plus or minus a margin. Fixed mortgage rates instead track Government of Canada bond yields, so a hike reaches a fixed borrower only when they renew or take a new mortgage (Bank of Canada).

The policy rate is the interest rate the Bank of Canada targets for overnight lending between financial institutions. It sets the floor for short-term borrowing costs across the economy. As of July 2026 the policy rate sits at 2.25% and prime is 4.45%, after the Bank held rates at its June 10, 2026 decision (Bank of Canada).

Here is how a hike travels through each mortgage type:

| Mortgage type | Priced against | When a rate hike is felt | What changes |

|---|---|---|---|

| Adjustable-payment variable | Lender prime rate | Within a billing cycle or two | Monthly payment rises |

| Fixed-payment variable | Lender prime rate | Immediately, but hidden | More of the fixed payment goes to interest |

| Fixed rate | Government of Canada bond yields | At renewal only | New payment set at the current rate |

The distinction matters because two households on the same street can feel the same hike years apart, or barely at all, depending only on the mortgage they signed.

How a rate hike hits you depends on your mortgage

The same rate hike produces four very different outcomes depending on which type of mortgage you hold, so the honest answer to "how does this affect me" starts with "which one are you?" Most guides describe a single generic borrower, but the position you are in decides both the size and the timing of the impact.

| Your position | What changes | When | The one action that helps |

|---|---|---|---|

| Fixed-payment variable holder | Payment stays flat; principal paydown slows, then stops at the trigger rate | Right away | Increase your payment voluntarily to stay ahead of the trigger rate |

| Adjustable-payment variable holder | Payment rises with each hike | Within one to two billing cycles | Build the higher payment into your budget before the next decision |

| Fixed-rate borrower renewing soon | New, higher payment at renewal | At term end | Shop the renewal early and budget for the jump now |

| New buyer being qualified | Lower maximum mortgage you qualify for | At application | Get pre-approved and know your stress-test ceiling |

New buyers meet the hike through the stress test. Under OSFI Guideline B-20, a federally regulated lender must qualify you at the higher of your contract rate plus two percentage points or a 5.25% floor (OSFI). When contract rates rise, that qualifying rate rises with them, so a hike shrinks the mortgage a given income can support before it ever touches a monthly payment.

How much does a rate hike actually cost? A worked example

A rate hike costs a real, calculable number of dollars per month, and the number is larger than most people expect once it lands. Below are three worked cases on a $500,000 mortgage with a 25-year amortization, using Canadian semi-annual compounding. Treat them as illustrations, not quotes.

The renewal jump

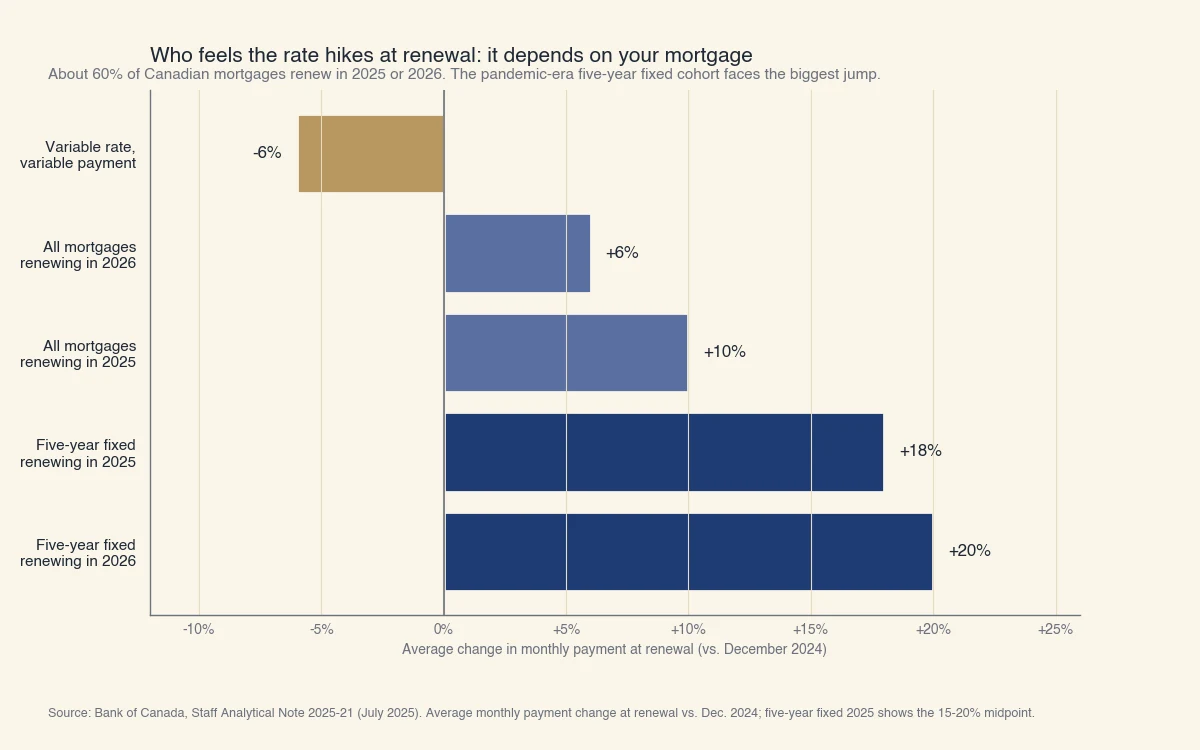

A borrower who locked a five-year fixed rate at 2.5% during the pandemic pays about $2,240 per month. After five years of payments their balance is roughly $423,000. If they renew that balance over the remaining 20 years at 4.5%, the new payment is about $2,670 per month. That is an increase of roughly $430 per month, or about 19%, with no change in how much they borrowed. This is why the Bank of Canada flags five-year fixed borrowers renewing in 2025 and 2026 as the group facing the largest increases (Bank of Canada, 2025).

The trigger rate

A borrower with a fixed-payment variable mortgage set their payment near a 2.0% starting rate. Their trigger rate, the rate at which the whole payment goes to interest, sits around 5%. The Bank of Canada raised the policy rate from 0.25% in early 2022 to 5.00% by mid-2023, and prime climbed from 2.45% to 7.20% over the same stretch (Bank of Canada). That pushed many fixed-payment borrowers well past their trigger rate, so their payment stopped covering interest and the shortfall was added to the balance. The payment looked unchanged while the mortgage quietly grew.

The purchasing-power squeeze

For a buyer, a hike shrinks how much house a given payment can carry. At $2,500 per month over 25 years, a 4.5% rate supports a mortgage of about $452,000. Raise the rate to 5.5% and the same payment supports about $410,000, roughly 10% less. A rough rule follows: each one-percentage-point increase trims about 10% off the mortgage a fixed payment can afford.

Source: Bank of Canada, Staff Analytical Note 2025-21 (July 2025). Average monthly payment change at renewal vs. December 2024; the five-year fixed 2025 figure shows the 15-20% midpoint.

Three things most people get wrong about rate hikes and your mortgage

Most confusion about rate hikes comes from three beliefs that feel true but are not, and each one can cost a household real money. Naming them is the fastest way to understand your own exposure.

"My fixed rate protects me." A fixed rate protects your payment during the term, not forever. The hikes still happen; you simply meet them all at once at renewal instead of gradually. About 60% of Canadian mortgages renew in 2025 or 2026, and roughly 60% of those renewals bring a higher payment, so a fixed rate is a delay, not a shield (Bank of Canada, 2025).

"My payment is fixed, so a hike does not touch me." A fixed-payment variable mortgage keeps the payment steady, which hides the impact rather than removing it. As rates rise, more of each payment goes to interest and less to principal, so you pay down the loan more slowly. Past the trigger rate the payment no longer covers the interest at all, and the unpaid interest is added to your balance. A steady payment can sit on top of a growing mortgage.

"The Bank of Canada sets my mortgage rate." The Bank sets the overnight rate, which moves prime and therefore variable mortgage rates. It does not set fixed mortgage rates. Those follow Government of Canada bond yields, which move on market expectations. This is why fixed rates sometimes rise or fall weeks before the Bank acts, and why a Bank decision to hold can still come with fixed rates moving.

What rate hikes do to the housing market

Higher interest rates cool housing demand by making mortgages more expensive and shrinking what buyers can borrow, which tends to slow price growth or lower prices. When a hike cuts the maximum mortgage a given income supports, fewer buyers can bid at yesterday's prices, so demand softens. The Bank of Canada tracks this through household debt and mortgage payment pressure in its Financial Stability Report (Bank of Canada).

The effect is real but not mechanical. Housing prices also respond to supply, population growth, employment, and local conditions, so rates are one strong force among several. A hike reliably raises the cost of borrowing; it does not guarantee a specific move in any one city's prices.

For most households the more direct concern is cash flow, not price. When rates rise, the FCAC recommends a short list of concrete steps (FCAC):

- Review your budget and test it against a payment that is 15% to 20% higher.

- Check your renewal date and start shopping the renewal a few months early.

- Contact your lender before a higher payment becomes a problem, not after.

- If you hold a fixed-payment variable mortgage, consider raising your payment now to stay ahead of the trigger rate.

Knowing which of the four positions above you are in tells you how much time you have to prepare, and which of these steps matters most for you.