What was the interest rate in Canada?

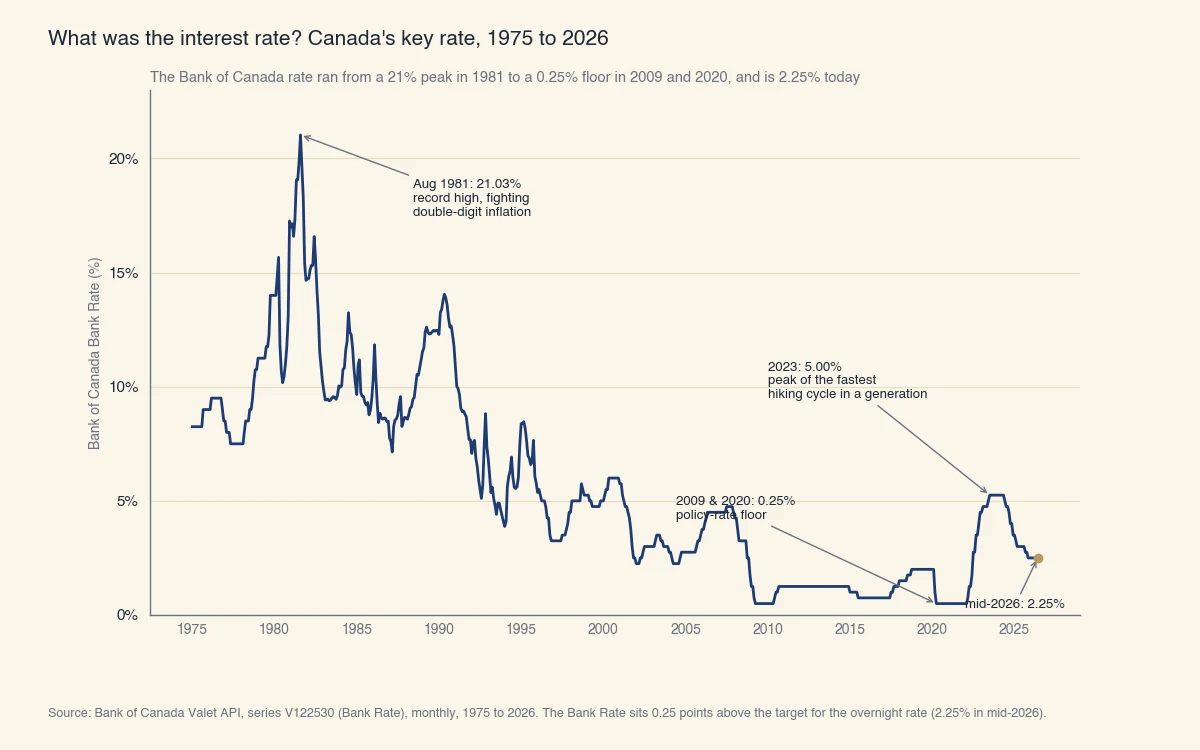

Over the past 50 years, the Bank of Canada's key interest rate has swung from a peak of 21.03% in August 1981 down to a floor of 0.25% in 2009 and again in 2020, and today it sits at 2.25%. There is no single "the interest rate" that held over time. The number moved constantly as the Bank of Canada responded to inflation, recessions, and financial crises (Bank of Canada).

The Bank Rate is the benchmark the Bank of Canada has published as its key rate for decades. It is the rate the Bank charges financial institutions on short-term loans, and today it sits 0.25 points above the more commonly quoted policy rate (the target for the overnight rate). Charting the Bank Rate gives the clearest single picture of what the interest rate was across Canadian history.

Source: Bank of Canada Valet API, series V122530 (Bank Rate), monthly, 1975 to 2026. The Bank Rate sits 0.25 points above the target for the overnight rate, which is 2.25% in mid-2026.

The eras that shaped the chart:

- The early 1980s peak. To break double-digit inflation, the Bank pushed the Bank Rate to 21.03% in August 1981. Mortgage holders renewing that year faced rates they could barely carry.

- The long decline. Through the 1990s and 2000s the rate trended down as inflation stabilized near the Bank's 2% target.

- The crisis floors. The rate fell to a 0.25% policy-rate floor in April 2009 (financial crisis) and March 2020 (pandemic).

- The 2022-2023 shock. The Bank raised the policy rate from 0.25% to 5.00% in about 18 months, the fastest hiking cycle in a generation, to fight post-pandemic inflation.

- The 2024-2026 easing. As inflation cooled, the Bank cut the policy rate back to 2.25% by mid-2026.

What was the highest interest rate, and why do sources disagree?

The highest interest rate in Canadian history was the 21.03% Bank Rate of August 1981, but you will also see a 16% "record high" quoted, and both can be right depending on the data series. The gap is a data-source trap worth understanding.

The 21% figure comes from the Bank of Canada's own Bank Rate series, which runs back to the 1930s (Bank of Canada). The 16% figure (February 1991) comes from shorter series that only start in 1990 and therefore never capture the 1981 spike. Those same shorter series report a long-run average near 5.75%. Neither number is wrong; they answer different questions. When you read any "record" interest rate, check what series it uses and how far back it goes.

What is the interest rate in Canada right now?

As of June 10, 2026, the Bank of Canada policy rate is 2.25%, held steady for the fifth straight meeting, and the prime rate at the major banks is 4.45%. The next scheduled rate decision is July 15, 2026 (Bank of Canada).

If you want today's full ladder of Canadian rates, from the policy rate up through prime to mortgages and credit cards, see what is the interest rate in Canada. The short version:

- Policy rate: 2.25%. Set by the Bank of Canada. Almost no one borrows at this rate directly.

- Prime rate: 4.45%. Set by each commercial bank, roughly the policy rate plus 2.20 points. Variable mortgages and lines of credit are priced against it.

- Your product rate. What you actually pay, sitting on top of prime depending on the product and your credit.

Compared with history, a 2.25% policy rate is low. It is a fraction of the 1981 peak and close to the levels Canada saw through the 2010s.

What is an interest rate, and who sets it in Canada?

An interest rate is the price of borrowing money, expressed as a percentage of the amount borrowed per year, and in Canada the headline rate is set by the Bank of Canada. The Bank sets the policy rate, formally the target for the overnight rate, to keep inflation low and stable near a 2% target (FCAC).

How the Bank has set its key rate has changed over the decades, which is part of why historical comparisons need care:

- 1935 to 1956: the Bank Rate was fixed, set directly by the Bank.

- 1956 to 1962, then 1980 to 1996: the Bank Rate floated, pinned 25 basis points above the yield on 3-month treasury bills.

- 1996 to today: the Bank sets the Bank Rate at the top of an operating band around the target for the overnight rate (Bank of Canada).

There is a practical lesson buried in this history. The interest rate everyone quotes is not the rate you actually pay. The policy rate is a wholesale rate between the Bank and financial institutions. Your rate is built on top of it: prime tracks the policy rate closely, but a fixed-rate mortgage follows Government of Canada bond yields instead, so a policy-rate cut does not automatically lower a fixed mortgage. Knowing which benchmark your loan follows matters more than the headline number.

What did those interest rates mean for a real mortgage?

The difference between the 2021 low and the 2023 peak was worth more than $1,000 a month on a typical $400,000 variable-rate mortgage. Percentages stay abstract until you turn them into dollars, so here is the math on a $400,000 balance amortized over 25 years, with the variable rate set at prime minus 0.50 points (a common discount).

| Period | Policy rate | Approx. variable rate | Monthly payment |

|---|---|---|---|

| 2021 (pandemic low) | 0.25% | ~1.95% | ~$1,686 |

| 2026 (today) | 2.25% | ~3.95% | ~$2,101 |

| 2023 (peak) | 5.00% | ~6.70% | ~$2,751 |

The numbers are illustrative, but the pattern is real. A borrower who renewed a variable mortgage at the 2023 peak paid roughly $1,065 more each month than someone on the 2021 low rate, on the same balance. That is about $12,800 a year, which is why the 2022-2023 hiking cycle strained so many household budgets even though the policy rate had been near zero just two years earlier.

The takeaway from a half-century of rate history: plan around the rate you can carry, not the rate you hope for. If you hold a variable mortgage or a line of credit, build a buffer for a swing of a full percentage point or more, because history shows rates can move that far in a single year.

What interest rate applies to OSAP and other Canadian loans?

The federal Canada Student Loan portion of OSAP charges 0% interest, permanently, since April 1, 2023, while other common Canadian loans are priced off the prime rate. The policy rate fans out into very different product rates (Government of Canada).

| Loan type | Typical interest basis | Approx. rate (mid-2026) |

|---|---|---|

| Canada Student Loan (federal OSAP portion) | Interest permanently eliminated | 0% |

| Ontario provincial OSAP portion | Provincially set, floating | ~prime + 1% |

| Variable-rate mortgage | Prime minus a discount | ~3.95% |

| Home equity line of credit (HELOC) | Prime plus a margin | ~4.95% |

| Unsecured personal line of credit | Prime plus 2 to 7 points | ~6.45% to 11.45% |

| Typical credit card | Set by the issuer | ~20.99% |

A few points to hold onto:

- OSAP is split. The federal Canada Student Loan portion is interest-free for good, but the provincial portion is set by your province. In Ontario it has carried a floating rate of prime plus 1%, so the "interest rate on OSAP" you repay depends on the mix of federal and provincial debt.

- Student loan interest can be tax-relevant. Interest paid on eligible government student loans may qualify for a federal tax credit, which softens the cost of any provincial portion.

- The product matters more than the policy rate. A credit card near 21% costs far more than a mortgage near 4%, and no Bank of Canada decision closes that gap. Moving a balance to a lower-rate product usually beats waiting for a rate cut.

At Sphera Credit, our work is helping lenders read each borrower's file accurately and fairly, especially when the numbers do not fit a simple rate-sheet box. Understanding what the interest rate was, how it is built today, and which benchmark your own loan follows is the first step to borrowing on terms that fit your situation.