Which bank has the highest TFSA interest rate in Canada?

The highest ongoing TFSA interest rates in Canada almost always come from online-only banks and credit unions, not the Big Six branch banks. A Tax-Free Savings Account (TFSA) is a registered account where the interest you earn is never taxed (Canada Revenue Agency). The rate it pays depends entirely on which institution holds it, and branch banks like RBC and TD pay some of the lowest rates in the market.

The phrase "which bank" is itself a little misleading. The institutions that pay the most are usually not chartered banks at all. They are credit unions and online banks with low overhead, which lets them pass more interest to savers. Here is a representative snapshot of TFSA savings-account rates in June 2026.

| Institution | Type | TFSA savings rate (June 2026) | Deposit protection |

|---|---|---|---|

| Tangerine | Online bank | 4.60% promo for 5 months, then about 0.30% | CDIC ($100,000) |

| Saven Financial | Credit union (Ontario) | 2.85% ongoing | Provincial (FSRA) |

| Canadian Tire Bank | Online bank | 2.40% ongoing | CDIC ($100,000) |

| Hubert Financial | Credit union (Manitoba) | 2.30% ongoing | DGCM (unlimited) |

| EQ Bank | Online bank | 1.50% ongoing | CDIC ($100,000) |

| RBC, TD, and other Big Six | Branch bank | about 0.35% ongoing | CDIC ($100,000) |

Two things stand out. First, the single highest number on the page is a promotional rate, a temporary teaser that drops to a low ongoing rate after a few months. Second, the steady rates that look smaller, like 2.85%, can actually pay you more over a full year. The next section shows why.

Rates move every week, so treat the table as a pattern, not a live quote. Always confirm the current rate on the institution's own page before you open an account.

What does the highest TFSA rate actually earn you?

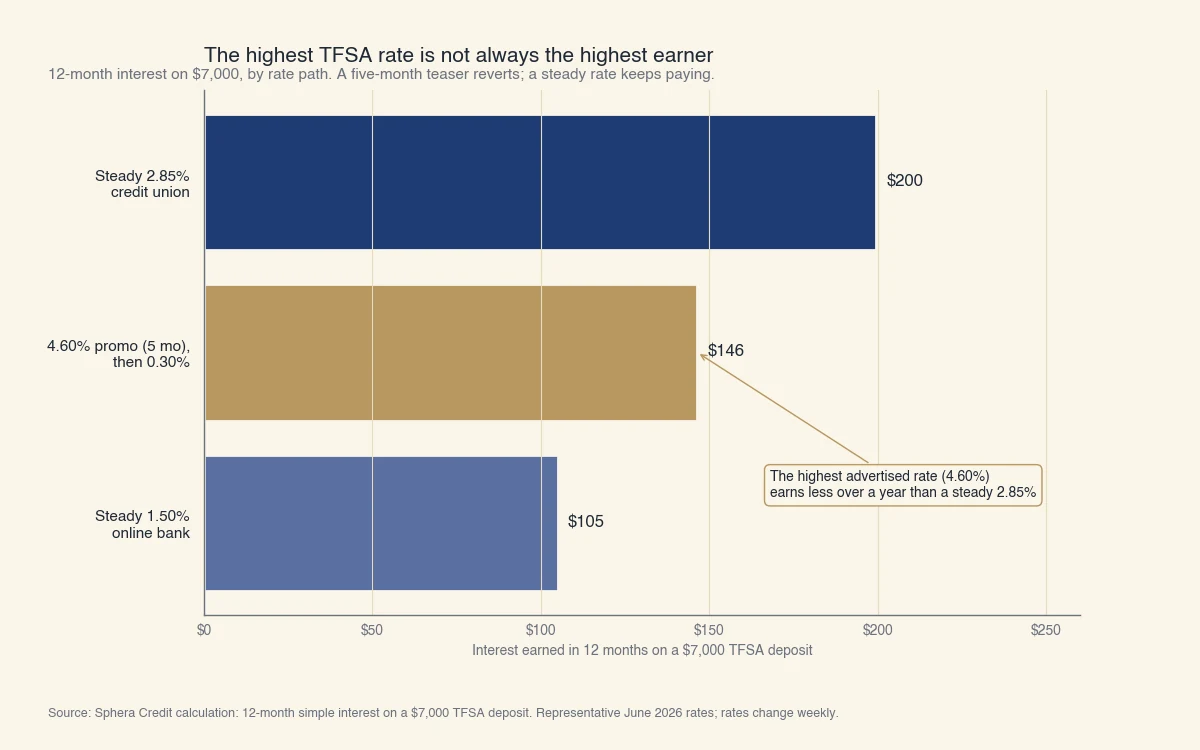

The highest advertised rate is often not the highest earner once the promotional period ends, because a five-month teaser reverts to a low ongoing rate while a steady mid-tier rate keeps paying all year. This is the calculation that the rate tables on competing sites leave out, and it is the one that actually answers the question.

Take a single $7,000 deposit, which is the full TFSA contribution room for 2026, and leave it untouched for twelve months. Compare three real rate paths:

- A 4.60% promo that reverts to 0.30%. You earn 4.60% for five months, then 0.30% for the remaining seven. That works out to $7,000 x 4.60% x 5/12, plus $7,000 x 0.30% x 7/12, which is $134.17 plus $12.25, or about $146.

- A steady 2.85% credit-union rate. You earn 2.85% for the full year: $7,000 x 2.85%, or about $200.

- A steady 1.50% online-bank rate. You earn 1.50% for the full year: $7,000 x 1.50%, or about $105.

Source: Sphera Credit calculation, 12-month simple interest on a $7,000 TFSA deposit, representative June 2026 rates. Rates change weekly.

The boring 2.85% rate quietly beats the flashy 4.60% headline by roughly $54 over the year. The reason is that the teaser only applies for part of the year, and the ongoing rate it reverts to is very low. The lesson is to read the ongoing rate, not the promotional one, unless you plan to move your money the moment the promo expires.

These figures use simple interest and assume the deposit sits untouched. Real savings accounts compound monthly, so the actual dollars are slightly higher, but the ranking does not change. The highest number on the rate sheet is not automatically the highest amount in your account a year later.

Which TFSA is right for your savings goal?

The best TFSA for you depends on when you need the money, not on which institution prints the highest rate. A TFSA is a container, and you can hold three very different things inside it. Matching the container to your goal matters more than squeezing out the last fraction of a percent.

- A high-interest savings account (HISA) keeps your money liquid and pays a variable rate. You can withdraw any day, but the rate can change at any time.

- A Guaranteed Investment Certificate (GIC) locks a fixed rate for a set term, often one to five years. It usually pays more than a savings account, but your money is tied up until the term ends.

- A self-directed or managed investment account holds stocks, exchange-traded funds, or mutual funds. It carries market risk but has the highest long-run growth potential.

Here is how the right choice changes with the saver.

| Saver profile | Goal and time horizon | Best TFSA type | What to optimize for |

|---|---|---|---|

| Emergency-fund saver | Money needed any day | High-interest savings | Liquidity first, rate second |

| Short-term goal saver | House down payment in 1 to 3 years | GIC (laddered) | Highest fixed rate for the term |

| Long-horizon saver | Retirement, 10+ years away | Investments | Growth, not cash rates |

The counterintuitive part is the third row. A saver with a ten-year horizon who parks cash at even the best TFSA savings rate is leaving the account's main benefit on the table. The whole point of a TFSA is tax-free growth, and a 2% savings rate barely keeps pace with inflation. For long-term money, chasing the top savings rate is the wrong move. The Canada Revenue Agency lets your TFSA hold qualified investments precisely so that long-term savers can capture that tax-free growth (Canada Revenue Agency).

If you are comparing a TFSA against an RRSP, the short version is that a TFSA gives you no deduction today but tax-free withdrawals later, while a Registered Retirement Savings Plan gives you a deduction today but taxes withdrawals as income. Lower earners and savers who want flexible access usually lean TFSA; higher earners saving strictly for retirement often lean RRSP.

Is your TFSA money safe, and is the interest really tax-free?

Yes on both counts: TFSA interest is never taxed, and the deposit itself is protected by either CDIC or a provincial guarantee, depending on the institution. These are the two questions savers worry about most, and both have clear answers from primary Canadian sources.

On tax, the rule is simple. Interest, dividends, and capital gains earned inside a TFSA are not taxed and do not need to be reported as income (Canada Revenue Agency). The only common way to create a tax bill is to overcontribute. If you put in more than your room allows, the Canada Revenue Agency charges 1% per month on the excess until you withdraw it (Canada Revenue Agency). The 2026 annual limit is $7,000, and cumulative room reaches $109,000 for someone eligible since 2009.

On safety, the answer depends on the type of institution:

- Banks are federally regulated and covered by the Canada Deposit Insurance Corporation (CDIC), which protects eligible deposits up to $100,000 per insured category at each member institution (CDIC). A TFSA is its own insured category, so it is covered separately from your chequing account at the same bank.

- Credit unions are provincially regulated and covered by a provincial guarantee instead of CDIC. Coverage varies by province, and some are far more generous than the federal limit. In Manitoba, the Deposit Guarantee Corporation of Manitoba (DGCM) guarantees all deposits at a Manitoba credit union with no dollar limit, including accrued interest (DGCM).

This is why a Manitoba credit union can sometimes quote a higher rate and still be a safe place to hold a large balance: the deposit guarantee is unlimited. The Financial Consumer Agency of Canada keeps a plain-language summary of which institutions are covered by which insurer if you want to confirm a specific one (FCAC).

The practical takeaway is that an unfamiliar online bank or small credit union offering a high rate is not riskier than a Big Six bank, as long as it is a CDIC member or covered by a provincial guarantee. The name on the door matters far less than the rate it pays and the insurer that stands behind it.

The bottom line

The highest TFSA interest rate in Canada is rarely at a Big Six branch bank, and the single highest advertised number is rarely the most you can actually earn. Online banks and credit unions consistently pay more, and the highest advertised number is usually a short promotional rate that reverts to something much lower. Read the ongoing rate, match the account type to your goal, and confirm the deposit protection. Do that, and you will earn more than the saver who simply chased the biggest number on the page.

At Sphera Credit, we build credit and lending technology that helps lenders make accurate, explainable decisions. Understanding how rates and accounts really work is the same kind of clear thinking we bring to credit. If you are weighing a borrowing decision next, our other learning guides walk through how interest rates work and credit step by step.