How much does it cost to buy down your interest rate?

One mortgage discount point costs 1% of the loan principal and typically reduces the interest rate by 0.25 percentage points. On a $400,000 30-year loan in the current 2026 rate environment, paying $4,000 for one point trims the rate from roughly 6.50% to 6.25% and saves about $66 per month, with a 60-month breakeven. The cost is mechanical: the answer to "how much" is always 1% of the loan multiplied by the number of points. The hard question is whether you should buy any.

This page answers the cost question first, then walks the comparisons that determine whether points are the right use of your closing-day cash: points versus paying down principal, points versus a larger down payment, and points versus a temporary 2-1 buydown.

How discount points work

A discount point is a one-time, upfront fee paid at closing in exchange for a permanently lower interest rate over the life of the loan. The trade is mechanical: 1 percent of the loan principal per point, in exchange for roughly 0.25 percentage points off the rate. The cost is paid to the lender, not to the seller or the broker.

The rate reduction per point is not fixed by law. Different lenders, different loan products, and different rate environments produce different reductions:

- Typical: 0.25 percentage points off per point.

- Range in current 2026 environment: 0.125% to 0.375% per point. Lenders with thinner margins on long-duration loans tend to offer more rate reduction per point.

- Cap: most lenders cap at 3 to 4 points per loan. The federal Qualified Mortgage rule caps total points-plus-fees at 3% of the loan principal for loans above the 2025 threshold of $107,747 (CFPB).

Points appear on your Loan Estimate and Closing Disclosure under "Origination Charges" and must be disclosed before closing under TILA-RESPA.

Cost example

| Loan amount | 0 points | 1 point | 2 points | 3 points |

|---|---|---|---|---|

| $300,000 | $0 | $3,000 | $6,000 | $9,000 |

| $400,000 | $0 | $4,000 | $8,000 | $12,000 |

| $500,000 | $0 | $5,000 | $10,000 | $15,000 |

| $750,000 | $0 | $7,500 | $15,000 | $22,500 |

This is the entire "how much does it cost" answer: 1% of loan principal per point. The harder question is whether the resulting rate reduction is worth the upfront cost.

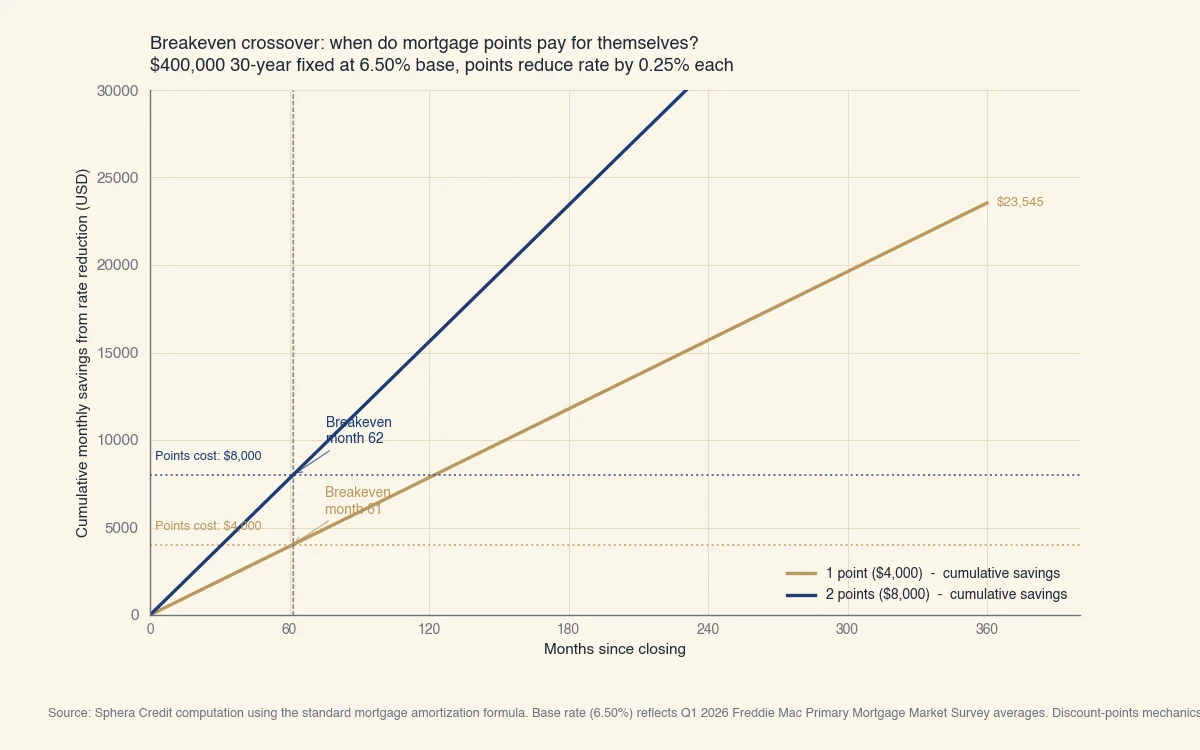

Worked example: 1 point on a $400,000 mortgage

At a base rate of 6.50% on a 30-year $400,000 mortgage, paying $4,000 for one point drops the rate to 6.25%, reduces the monthly principal-and-interest payment from $2,528 to $2,462, saves $66 per month, and breaks even after 60 months. The crossover graph below visualizes the breakeven point.

Source: Sphera Credit computation using standard mortgage amortization formulas. Loan terms based on Q1 2026 Freddie Mac Primary Mortgage Market Survey average rates. Calculation verified against CFPB and IRS published methodologies.

The math:

- Cost of 1 point: 1% × $400,000 = $4,000

- Monthly P&I at 6.50%: $2,528

- Monthly P&I at 6.25%: $2,462

- Monthly savings: $2,528 - $2,462 = $66

- Breakeven: $4,000 ÷ $66 ≈ 60 months (5 years)

- Lifetime savings if held 30 years: $66 × 360 = $23,760 in nominal dollars

- Lifetime savings net of point cost: $23,760 - $4,000 = $19,760

To model the math for your own loan amount and rate, use the mortgage payment calculator. Plug in your principal, the base rate, and a points scenario to see your monthly difference.

A second point doubles the cost but roughly doubles the savings, so breakeven stays near 60 months. The marginal point past two is usually less attractive because most lenders concede less rate per dollar at higher point levels.

Should you buy points, pay down principal, or skip both?

The honest comparison no SERP top result shows: the $4,000 you would spend on points can also pay down principal or add to your down payment. For a $400,000 loan at 6.50%, buying one point saves $66 per month. Putting the same $4,000 toward principal saves about $22 per month. Adding $4,000 to the down payment to drop below an LTV threshold can save $100+ per month by eliminating PMI. The right answer depends on where you are below 20% equity, whether you are likely to refinance, and how long you will own the home.

| Use of $4,000 | Monthly impact | Breakeven | Reversible? |

|---|---|---|---|

| 1 discount point | -$66 P&I | 60 months | No (sunk cost) |

| Add to down payment (above 20% LTV) | None directly | N/A | Yes (equity stays in home) |

| Add to down payment (drops below 80% LTV threshold) | -$100 to -$200 if PMI removed | Immediate | Yes |

| Pay down principal in month 1 | -$22 P&I | About 180 months | Yes (becomes equity) |

| Keep in liquid savings | None | N/A | Fully liquid |

Three decision rules:

- If buying with less than 20 percent down: add the $4,000 to your down payment first. Reducing the loan-to-value ratio to eliminate private mortgage insurance can save $100 to $300 per month, far more than any rate point will. Only consider points after PMI is no longer a factor.

- If you are at or above 20 percent down and plan to hold past breakeven: points usually win. The lifetime interest savings exceed the upfront cost.

- If you are at or above 20 percent down but might refinance within 3 to 4 years: apply the money to principal instead. Principal reduction stays with you (becomes equity); points are sunk on the day of closing.

Breakeven by tenure profile

Buying points only makes sense if you stay long enough. Median US homeowner tenure is around 13 years (NAR), but that statistic masks a huge range: first-time buyers stay 8 years, repeat buyers 16 years, and a refinance inside 5 years effectively ends the original loan. Match your real tenure expectation to the breakeven before committing $4,000.

| Tenure profile | Expected hold | 1-point breakeven met? | 2-point breakeven met? |

|---|---|---|---|

| First-time buyer (single, mobile) | 4-7 years | Maybe (60-month breakeven) | Maybe |

| First-time buyer (settling down) | 7-12 years | Yes | Yes |

| Growing family upgrading | 5-9 years | Maybe | Maybe |

| Mid-career stable household | 10-15 years | Yes | Yes |

| Empty-nester | 15+ years | Yes | Yes |

| Retiree forever home | 20+ years | Yes | Yes |

A refinance inside the breakeven window is the silent killer of points economics. If rates drop by 0.75% to 1.00% within 36 months, the typical mortgage refinance becomes attractive (NAR). Anyone buying in a high-rate environment with realistic refinance expectations within 3 years should usually skip points entirely and use the cash for principal or down payment instead.

Permanent buydown vs temporary 2-1 and 3-2-1 buydowns

A permanent buydown (discount points) reduces the rate for the life of the loan. A temporary buydown (2-1 or 3-2-1) reduces the rate only for the first two or three years, then reverts to the note rate. Each fits a different situation.

- Permanent (discount points): 1% of loan per point for roughly 0.25% lower rate for the full term. Best when you expect to hold the loan long enough to cross breakeven.

- 2-1 temporary buydown: rate reduced 2 percentage points in year 1, 1 point in year 2, full note rate in year 3 onward. Cost equals the total interest savings across years 1 and 2, held in escrow and applied monthly.

- 3-2-1 temporary buydown: same structure, but 3 / 2 / 1 percentage-point reductions in years 1 through 3. More expensive and rarer in current rate environment.

Who should consider each:

- Permanent points: long-tenure buyers above 20% LTV who do not expect to refinance soon.

- Temporary buydown (seller-paid): buyers in a high-rate market who expect rates to drop within 2 to 3 years and refinance. The seller pays the buydown as a concession; the buyer gets a front-loaded discount and refinances out before the full note rate kicks in. This is the configuration the SERP almost never names but that has been common in the 2024-2026 high-rate environment.

- Temporary buydown (buyer-paid): rarely optimal. If you have cash to spend at closing, points or principal beat a buyer-funded temporary buydown in almost every scenario.

The CFPB has explicit guidance on how temporary buydowns must be disclosed and how unused escrow funds are returned to the borrower if the loan is paid off, refinanced, or assumed before the buydown period ends.

Tax treatment and other rules

Discount points on a primary home purchase are deductible in the year paid if you itemize and meet the IRS conditions in Topic No. 504. Refinance points are not deductible in one year; they must be deducted ratably over the loan term. A few other rules matter at closing:

- Itemize requirement: points are deductible only if you itemize on Schedule A. With the standard deduction at roughly $30,000 for married filing jointly in 2026, many households take the standard and lose the deduction.

- $750,000 cap on deductible mortgage interest: applies to home-purchase debt incurred after December 15, 2017 (IRS Topic 504). Older mortgages retain the $1 million cap.

- Refinance ratable deduction: points paid on a refinance must be deducted over the loan term. If you refinance a 30-year loan, you deduct 1/30 of the points per year. If you refinance again or pay off the loan early, any remaining undeducted points become fully deductible in the payoff year.

- Origination fees are not discount points: origination charges and points appear in the same section of your Loan Estimate but only discount points reduce the rate. Origination is not deductible as mortgage interest.

Bottom line

Buying down your interest rate costs 1% of the loan per point, drops the rate roughly 0.25%, and breaks even around 60 months on a typical $400,000 30-year loan at 6.50%. Before buying any points: check whether your money is better spent eliminating PMI or paying down principal, and match your real expected tenure against the breakeven. If you might refinance within 3 years or sell within 5, skip points entirely; if you are settled and well past 20 percent equity, points usually win in the long run.