How do you calculate an interest rate?

Three formulas cover almost every interest-rate calculation a borrower or saver needs: simple interest (I = P × r × t), compound interest (A = P × (1 + r/n)^(nt)), and the standard amortization formula for loan payments. The right one depends on the product. Bank savings accounts use compound interest. Most credit-card and mortgage products use compounding plus amortization. Old-school personal loans sometimes still use simple interest. Knowing which formula applies tells you whether the rate you see is the rate you actually pay.

The Financial Consumer Agency of Canada publishes plain-language explanations of each formula along with examples, and the Cost of Borrowing (Banks) Regulations require Canadian lenders to disclose interest using consistent definitions across products (FCAC).

Why the choice of formula matters in dollars: the gap between simple and compound interest on a $10,000 balance over 5 years at 5% is only $262. The gap on a $400,000 mortgage over 25 years between monthly and semi-annual compounding is roughly $1,200. The gap between a 5.50% and 6.50% mortgage rate over the same 25 years is about $80,000. Compounding convention matters less than the headline rate, but for big balances and long periods, every basis point shows up.

What is the simple interest formula?

The simple interest formula is I = P × r × t, where I is the interest accrued, P is the principal, r is the annual interest rate (as a decimal), and t is time in years. A $5,000 personal loan at 8% simple interest for 3 years accrues $5,000 × 0.08 × 3 = $1,200 of interest. The total repayment is the principal plus the interest: $6,200. Simple interest does not compound; the rate only ever applies to the original principal. Real personal-loan rates vary widely by lender, so it pays to compare which bank has the lowest personal loan rate in Canada before you borrow.

What is the compound interest formula?

The compound interest formula is A = P × (1 + r/n)^(n × t), where A is the future amount, P is the starting principal, r is the annual rate, n is the number of compounding periods per year, and t is the number of years. Compound interest captures the "interest on interest" effect that makes long-term saving and long-term debt work the way they do.

Worked example for a $10,000 deposit at a 5% annual rate compounded annually for 5 years:

A = 10,000 × (1 + 0.05/1)^(1 × 5) = 10,000 × 1.05^5 = $12,762.82

Compare with simple interest at the same rate:

I = 10,000 × 0.05 × 5 = $2,500, total A = $12,500

The compounding adds $262.82, or about 1% of the starting principal. Now run the same calculation over 25 years:

- Compound: $10,000 × 1.05^25 = $33,864

- Simple: $10,000 + ($10,000 × 0.05 × 25) = $22,500

- Compounding-only gap: $11,364, more than the original deposit

This is why FCAC's borrowing-cost guidance uses compound formulas as the default, and why short-term rates and long-term rates feel so different.

What is the effective annual rate?

The effective annual rate (EAR) translates a nominal rate plus a compounding convention into the single equivalent annual rate that produces the same return when compounded once. The formula:

EAR = (1 + r_nominal / n)^n − 1

A 6% rate compounded monthly: (1 + 0.06/12)^12 − 1 = 6.168%. The same nominal 6% compounded daily: (1 + 0.06/365)^365 − 1 = 6.183%. EAR is what makes products with different compounding schedules comparable. Canadian credit cards typically advertise the nominal rate but the EAR is what you actually pay if you carry a balance.

How is interest calculated on a Canadian mortgage?

Canadian mortgages compound semi-annually (twice a year) by federal law, even though most are paid monthly. The Interest Act of Canada (R.S.C., 1985, c. I-15) sets the semi-annual compounding rule for residential mortgages, and lenders convert the semi-annual nominal rate to the equivalent monthly rate using (1 + r/2)^(1/6) − 1. A 6% Canadian nominal mortgage rate has a monthly equivalent of 0.4939% (vs. 0.5000% for true monthly compounding).

The math matters. Below is how the same nominal rate behaves under the two conventions on a 25-year, $400,000 mortgage:

| Convention | Monthly rate | Monthly payment | Total interest paid |

|---|---|---|---|

| US-style monthly compounding | 0.5000% | $2,577.21 | $373,162 |

| Canadian semi-annual compounding | 0.4939% | $2,557.10 | $367,131 |

The Canadian convention saves the borrower about $6,000 in interest over the life of a mortgage at the same headline rate. This is why a 6% Canadian mortgage is structurally a bit cheaper than a 6% US mortgage, though headline-rate comparisons rarely flag the difference.

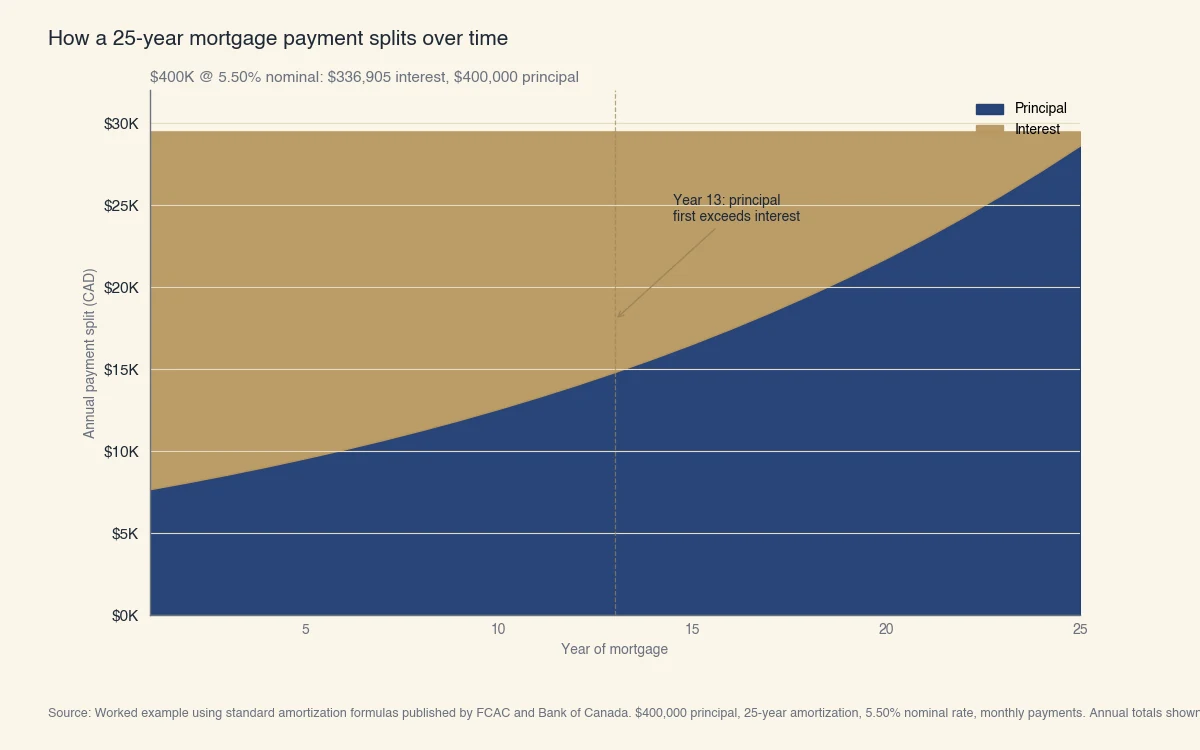

The chart below shows the standard $400,000 25-year Canadian mortgage at a 5.50% nominal rate, splitting each year's payment between principal repayment and interest charges. Early years are dominated by interest because the balance is large; late years are dominated by principal repayment because the balance has shrunk.

Source: Worked example using standard amortization formulas published by FCAC and Bank of Canada. $400,000 principal, 25-year amortization, 5.50% nominal rate, monthly payments. Annual totals shown.

The crossover at year 13 is a useful planning anchor. Borrowers who plan to sell or refinance well before year 13 are paying mostly interest and have built very little equity through amortization alone. Borrowers who pass year 13 are reducing principal faster than interest is accruing, which compounds in their favor over the rest of the term.

What is the loan amortization formula?

The standard amortization formula computes the fixed monthly payment that fully repays a loan over its term, given the principal, rate, and number of payments: M = P × [r × (1 + r)^n] / [(1 + r)^n − 1], where M is the monthly payment, P is the principal, r is the periodic (monthly) interest rate, and n is the total number of payments.

Worked example for a $400,000 mortgage at 5.50% nominal annual rate over 25 years (Canadian semi-annual compounding):

- Convert the semi-annual nominal rate to a monthly rate:

r = (1 + 0.055/2)^(1/6) − 1 = 0.004532(about 0.4532% per month). - Total payments:

n = 25 × 12 = 300. - Apply the formula:

M = 400,000 × [0.004532 × 1.004532^300] / [1.004532^300 − 1]. - Result:

M ≈ $2,442per month.

For a US-style monthly compounding loan at the same nominal 5.50% rate:

r = 0.055 / 12 = 0.004583M = 400,000 × [0.004583 × 1.004583^300] / [1.004583^300 − 1]M ≈ $2,456per month

The structural conclusion: monthly compounding produces slightly higher payments than Canadian semi-annual compounding at the same nominal rate. A borrower comparing Canadian and US mortgage offers should adjust for this convention before assuming the lower headline rate is actually cheaper.

How do you calculate the total interest over a loan's life?

The shortcut is Total interest = (M × n) − P. For the $400,000 Canadian mortgage above:

Total interest = ($2,442 × 300) − $400,000 = $732,600 − $400,000 = $332,600

Plug in different rates and the sensitivity becomes clear:

- 4.50%: $267,400 total interest

- 5.50%: $332,600 total interest

- 6.50%: $400,800 total interest

Each percentage point shifts total interest by about $66,000 to $80,000 on this size loan. That is the cost of waiting an extra cycle on a refinance, or the savings from negotiating 25 basis points off the rate.

How do you calculate interest on a credit card or line of credit?

Most Canadian credit cards calculate interest using a daily periodic rate applied to the average daily balance, but most cards offer a grace period that means you pay zero interest if the statement balance is paid in full each month. Lines of credit calculate interest similarly but typically have no grace period: interest accrues from the moment the funds are drawn.

The credit-card daily-periodic-rate calculation:

- Daily periodic rate (DPR): annual rate / 365. A 22% APR card has a DPR of 0.0603% per day.

- Average daily balance: sum of each day's ending balance divided by the number of days in the cycle.

- Interest charged: DPR × average daily balance × days in cycle.

A $1,500 average daily balance on a 22% APR card over a 30-day cycle accrues 0.000603 × 1,500 × 30 = $27.13 of interest. If the cycle ends and the card is not paid off, that $27.13 is added to the balance and starts accruing its own interest the following day.

Lines of credit (HELOC, unsecured LOC, business operating line) calculate interest in the same daily-balance way but without grace periods. Interest is typically debited from the same account on a fixed monthly date.

What about variable rates?

A variable rate is set as a margin over a published index (in Canada, usually the prime rate). When the Bank of Canada changes the policy rate (see when the next Bank of Canada rate announcement is), banks adjust their prime rate, and every variable-rate product reprices automatically. The math is otherwise identical: the same compounding and amortization formulas apply at the new rate.

Variable-rate borrowers should run the amortization math at both today's rate and a stress-test rate (the OSFI Guideline B-20 minimum is 5.25% or contract rate plus 200 basis points, whichever is higher) before signing, so the household budget can survive a rate increase (OSFI). Rates also move with the economic cycle: during a recession the Bank of Canada usually cuts its policy rate, which lowers variable payments quickly but may leave fixed rates unchanged.

Summary: which formula do I use when?

The right interest formula is determined by what you're calculating: simple interest for non-compounding loans, compound interest for savings, amortization for fixed-rate loan payments, and Effective Annual Rate to compare products with different compounding schedules. The table below maps each common task to the formula it needs.

| If you are calculating | Use |

|---|---|

| Total interest on a no-compounding loan | Simple interest: I = P × r × t |

| Future value of a savings account | Compound interest: A = P × (1 + r/n)^(n × t) |

| Monthly payment on a fixed-rate loan | Amortization: M = P × r(1+r)^n / [(1+r)^n − 1] |

| Comparing rates with different compounding | Effective Annual Rate: (1 + r/n)^n − 1 |

| Total interest paid over a mortgage | (M × n) − P |

| Interest on a credit-card revolving balance | Daily periodic rate × average daily balance × days |

To verify these formulas against your own numbers, run them through the compound interest calculator or the mortgage payment calculator.

Most modern loan calculators and bank apps run these formulas under the hood. Knowing the formulas does not replace the calculator; it means you can sanity-check the calculator and recognize when a rate disclosure is hiding compounding behind a low headline number.