Why do lower interest rates cause inflation?

Lower interest rates make borrowing cheaper, which encourages households to spend and businesses to invest, which raises total demand. When that demand outpaces the economy's productive capacity, sellers raise prices and inflation rises. The Bank of Canada's monetary-policy framework treats this rate-to-spending-to-prices chain as the principal transmission mechanism it controls (Bank of Canada). The relationship holds on average but is neither instant nor automatic; the transmission lag runs roughly 18 to 24 months and the strength of the effect depends on where the economy sits relative to capacity.

The plain-language version of the chain: the Bank of Canada cuts the overnight rate by 25 basis points; commercial banks lower their prime rate; borrowing on credit cards, lines of credit, and new mortgages gets cheaper; some households decide to buy a house or a car they were postponing; businesses bring forward an equipment purchase; that extra spending hits the same supply of goods and labour; if supply cannot keep up, prices rise.

Why this matters in practice: the rate-inflation link is the reason the Bank of Canada exists and the reason mortgage rates change. Understanding the link tells a borrower why rates cut now will likely show up in higher prices in 18 months, and why a central bank raising rates aggressively today is signaling it expects inflation to keep running above target without intervention.

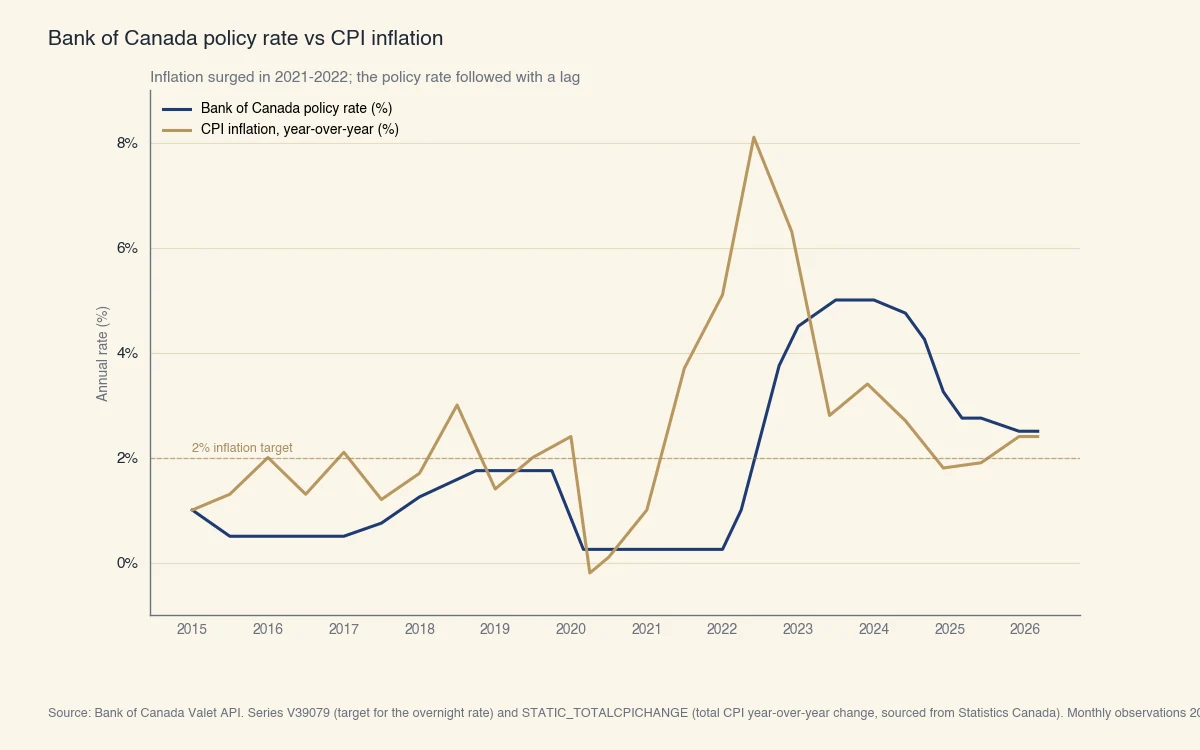

The chart below shows the Bank of Canada's policy rate alongside annual CPI inflation since 2015. The 2021-2022 inflation surge was the fastest in 40 years; the policy rate followed roughly six months later, peaking at 5.00% in mid-2023. By 2024-2025 inflation had returned near the 2% target and the policy rate began coming down.

Source: Bank of Canada Valet API. Series V39079 (target for the overnight rate) and STATIC_TOTALCPICHANGE (total CPI year-over-year change, sourced from Statistics Canada). Monthly observations 2015 to 2026.

How does the rate-inflation link work step by step?

The Bank of Canada describes monetary-policy transmission as five linked channels: borrowing rates, exchange rate, asset prices, expectations, and credit availability. Each channel turns a change in the overnight rate into a change in spending, and that spending change into a change in inflation 12 to 24 months later.

The five transmission channels:

- Borrowing rates. A lower policy rate lowers the prime rate, which lowers credit-card APRs, HELOC rates, line-of-credit rates, and the rates on new mortgages. Households and businesses face cheaper debt, so they take on more.

- Exchange rate. Lower Canadian rates relative to other countries' rates make the Canadian dollar less attractive to foreign investors, which lowers the dollar's exchange value. Imports become more expensive (raising inflation directly) and Canadian exports become cheaper for foreigners (raising demand).

- Asset prices. Lower rates push up the present value of stocks, real estate, and other assets. Households who own appreciating assets feel wealthier and spend more (the "wealth effect").

- Expectations. If households and businesses believe the central bank will keep policy loose, they expect inflation and act on that expectation: workers ask for bigger raises, sellers raise prices preemptively. Expectations can be self-fulfilling.

- Credit availability. Lower rates make banks more willing to lend, which expands the supply of credit available to borrowers who would have been declined at higher rates.

All five channels work in the same direction: lower rates → more spending → more demand → upward pressure on prices.

Why doesn't every rate cut cause inflation?

Lower rates only push prices up when demand growth bumps against the economy's productive capacity. A stylized way to see this: if there are 1 million unsold cars on dealer lots and 100,000 unemployed factory workers, an extra 50,000 cars of demand can be filled by drawing down inventory and hiring some of the unemployed. Prices barely move. If inventory is at zero and unemployment is at 3%, the same 50,000 extra cars of demand produces wage bidding, parts shortages, and higher car prices.

This is why the 2020 pandemic stimulus produced very little inflation in 2020-2021 (supply was deeply impaired but demand collapsed first), and why inflation surged in 2021-2022 (supply chains struggled to restart while household savings unleashed pent-up spending). The same policy rate had different effects in different regimes.

Why did Canadian inflation surge in 2021-2022?

The 2021-2022 inflation episode combined three forces: pandemic-era demand stimulus running into pandemic-era supply constraints, a global energy-price shock following Russia's invasion of Ukraine, and a sharp rebound in services demand once public-health restrictions lifted. The Bank of Canada's analysis attributes roughly equal shares to demand, supply, and energy in 2022 (Bank of Canada). It was not a pure rate-driven inflation episode, but the policy-rate response was nonetheless the central tool that brought inflation back down.

The progression in numbers:

| Date | BoC policy rate | CPI YoY |

|---|---|---|

| Jan 2021 | 0.25% | 1.0% |

| Jan 2022 | 0.25% | 5.1% |

| June 2022 | 1.50% | 8.1% (peak) |

| Jan 2023 | 4.50% | 5.9% |

| July 2023 | 5.00% (peak) | 3.3% |

| Jan 2024 | 5.00% | 2.9% |

| Dec 2024 | 3.25% | 1.8% |

| March 2026 | 2.50% | 2.4% |

The chart at the top of this page plots the same data monthly. The pattern is the canonical central-bank response: hold rates low while inflation appears transitory, then raise aggressively once inflation persists, then cut once inflation has clearly returned to target.

What is the inflation target?

The inflation target is the year-over-year change in the Consumer Price Index that the central bank tries to achieve on average over the medium term. The Bank of Canada and the Government of Canada renew the target in a five-year inflation-control agreement; the current target is 2%, with a control range of 1% to 3%.

The 2% target is not a Canadian peculiarity. Most advanced-economy central banks (the US Federal Reserve, European Central Bank, Bank of England, Reserve Bank of New Zealand, Bank of Japan since 2013) target 2% inflation. The number is empirical: low enough that inflation does not erode purchasing power meaningfully, high enough to give the central bank room to cut nominal rates in a recession without hitting the zero lower bound.

What happens when interest rates and inflation move in opposite directions?

The textbook relationship runs from rates to inflation through demand, but in practice rates and inflation often move together because the central bank reacts to inflation rather than driving it. The chart at the top of this page shows exactly this: from 2021 onward, inflation rose first, then the policy rate followed. From 2024 onward, inflation fell first, then the policy rate followed.

This is why charts of "the relationship between interest rates and inflation" can look misleading. The naive correlation tells you the central bank is reactive, not that high rates cause high inflation. Properly disentangling the relationship requires controlling for what the central bank was forecasting, which the IMF's "Back to Basics" series on monetary policy works through in some detail (IMF).

What is the Phillips curve?

The Phillips curve is the empirical observation that low unemployment usually coincides with higher inflation, and high unemployment usually coincides with lower inflation. It is named after A.W. Phillips, who first published the relationship for the UK in 1958. Modern versions of the curve add inflation expectations as a third variable, because the original 1958 curve broke down in the 1970s when inflation expectations decoupled from current unemployment.

For 1990-2020 the Phillips curve in Canada was very flat: unemployment dropping from 8% to 5.5% barely moved inflation. Bank of Canada research attributes the flattening to better-anchored inflation expectations and structural changes in labour and product markets. The 2021-2022 surge briefly steepened the curve again, suggesting expectations were less anchored than they had appeared.

The practical takeaway for borrowers: the rate-inflation transmission is real but weaker and slower than the textbook suggests. A 25-basis-point cut today does not produce a 25-basis-point inflation rise next month; over 18 to 24 months it produces a small, hard-to-isolate contribution to demand and prices.

Can low rates cause asset-price inflation without consumer-price inflation?

Yes, and that is the dominant pattern in advanced economies between roughly 2010 and 2020. Most central banks held policy rates very low while consumer-price inflation stayed below target. Asset prices (housing, equities, cryptocurrencies, fine art) rose substantially. Asset-price inflation is not in the Bank of Canada's CPI mandate, but the Bank's Financial Stability Report and the Office of the Superintendent of Financial Institutions both flag housing-price inflation and household-debt buildup as separate financial-stability concerns.

The mechanism: low rates raise the present value of any income-producing asset (a house's rental cash flow, a stock's dividend stream, a bond's coupon stream). The same dollar of future income is worth more today when the discount rate is lower. Asset owners' wealth rises; a smaller share of new buyers can afford to enter the market; prices keep rising. None of this shows up in the CPI basket of consumer goods and services, so the central bank's CPI metric stays in target while the housing market doubles.

Whether this is a "policy mistake" is contested. The Bank of Canada's view is that price stability and financial stability are separate mandates, with macroprudential tools (OSFI's stress test, default-insurance rules, debt-service-ratio caps) handling asset-price excesses while the policy rate handles CPI inflation. Critics argue the separation is artificial, since cheap money flows wherever returns are highest, including into assets.

What does this mean for a borrower today?

The rate-inflation link affects a Canadian borrower three concrete ways: variable-rate payments track the policy rate within weeks, fixed-rate offers move with bond yields and expected inflation, and the real return on savings depends on the gap between nominal rates and CPI. Knowing the link does not let you forecast rates, but it tells you which lever to watch when planning a loan or refinance.

- Variable-rate loan payments move with the policy rate. A 1-percentage-point rate cut on a $400,000 variable-rate mortgage saves about $200 to $250 a month at current rates. The cut reaches your payment within one to two billing cycles.

- Fixed-rate offers move with bond yields, which move with expected inflation. A 5-year fixed mortgage rate is priced off the 5-year Government of Canada bond yield. If markets expect higher inflation, bond yields rise, and the 5-year fixed rate rises even before the Bank of Canada acts.

- Real returns on savings depend on the gap between rates and inflation. A 4% GIC is a 1% real return when inflation is 3%, and a 3% real return when inflation is 1%. The same nominal rate has very different purchasing power depending on the inflation environment. For the US-side question of when the rate cycle turns, see when interest rates will go down.

For long-term planning the rule of thumb is: do not assume current rates will persist. The policy rate has averaged about 3% over the past 25 years; it has been as low as 0.25% and as high as 5.25%. A 25-year mortgage will see at least one full rate cycle, probably two. Building stress-test scenarios into your budget is what the OSFI stress test exists for.