What is a good interest rate for a car?

A good US auto loan rate in 2026 is roughly 4.66% APR for super-prime borrowers buying new and 7.70% for super-prime buyers of used vehicles, with each lower credit tier adding 1 to 7 percentage points. Those numbers come from Experian's State of the Automotive Finance Market for Q4 2025, the most recent quarterly release at publication (Experian).

The trick is that "good" does not mean one rate. It means a rate at or below the average for your credit tier, on the loan term that fits your budget, with the manufacturer rebates and dealer add-ons accounted for. The rest of this page walks through the average rate at each tier, why two borrowers with the same score get different quotes, and the two structural pieces (dealer markup, 0% APR trade-offs) that move your effective rate by more than your credit score does.

Quick reference for 2026, sourced from Experian's quarterly market report:

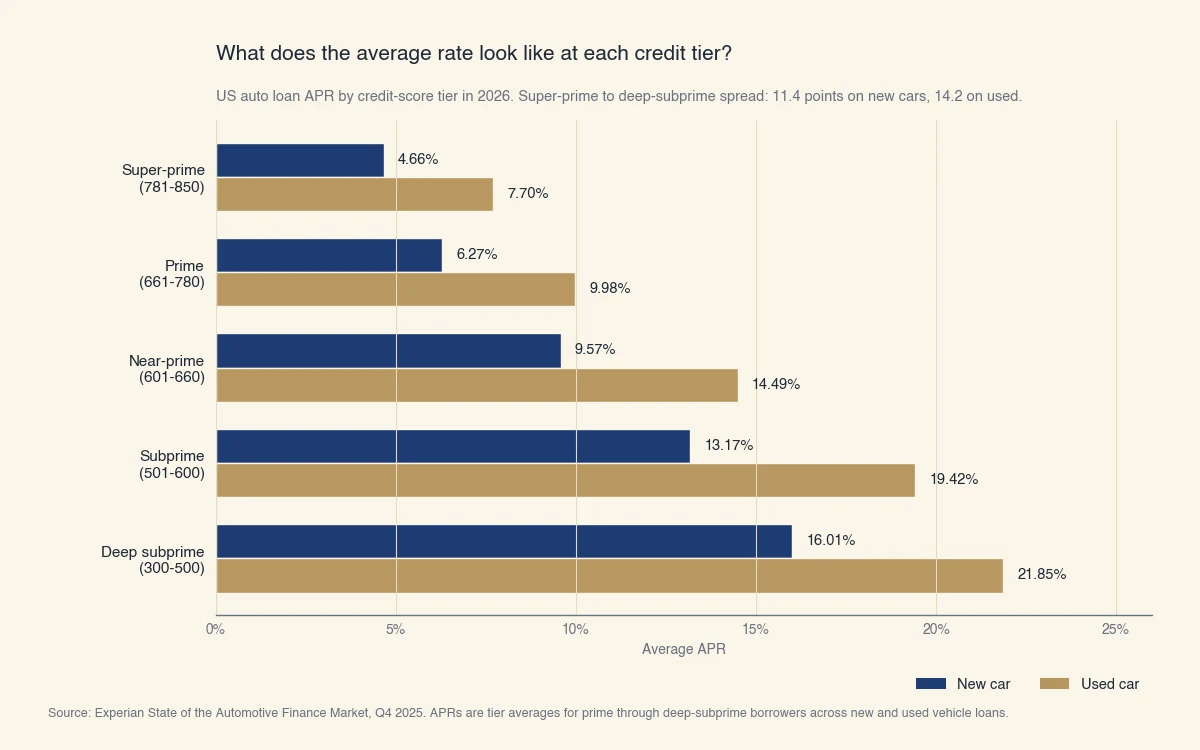

- Super-prime (781+): 4.66% new, 7.70% used

- Prime (661–780): 6.27% new, 9.98% used

- Near-prime (601–660): 9.57% new, 14.49% used

- Subprime (501–600): 13.17% new, 19.42% used

- Deep subprime (300–500): 16.01% new, 21.85% used

The Federal Reserve's federal funds target rate sits at 3.50–3.75% as of mid-2026, with one further rate cut signalled in the most recent FOMC projections (Federal Reserve FOMC calendars). Auto loan rates tend to move with the funds rate on a 1–3 month lag, so the numbers above will likely drift slightly lower in late 2026 if the cut materialises.

Average car loan rates by credit score in 2026

The gap between super-prime and deep-subprime new-car rates is roughly 11.4 percentage points; on used cars it widens to 14.2 points, which is the widest tier spread in the consumer credit market. A reader landing on this page wants the table laid out cleanly, so here it is:

| Credit tier | New car APR | Used car APR | Loan-life cost on $30k / 60 months (new car) |

|---|---|---|---|

| Super-prime (781–850) | 4.66% | 7.70% | ~$3,689 in interest |

| Prime (661–780) | 6.27% | 9.98% | ~$5,025 in interest |

| Near-prime (601–660) | 9.57% | 14.49% | ~$7,795 in interest |

| Subprime (501–600) | 13.17% | 19.42% | ~$10,917 in interest |

| Deep subprime (300–500) | 16.01% | 21.85% | ~$13,512 in interest |

Source: Experian State of the Automotive Finance Market, Q4 2025. Loan-life cost computed at 60-month term on a $30,000 principal.

The headline number to pay attention to is the spread between prime and near-prime: a reader whose score falls from 670 to 650 (still both "good" in everyday language) sees their new-car rate jump from 6.27% to 9.57%. On a $30,000 60-month loan that one tier change costs roughly $2,770 in extra interest over the life of the loan. Improving a near-prime score by 20 points to push into prime is one of the highest-impact actions a buyer can take before applying.

Used cars are uniformly higher across all tiers because used vehicles depreciate less predictably than new ones. Lenders price the larger loss-given-default into the rate. If you are shopping a 2-year-old certified pre-owned car, expect to pay 3 to 5 percentage points more than the new-car rate in the same tier.

To translate these tier averages into a monthly payment for your specific loan amount and term, run the numbers through the car loan calculator. Provincial-specific versions with the correct sales-tax math are linked from that page.

Why your rate is usually not your tier's average rate

The credit score puts you into a tier, but lenders price within the tier independently, and dealers add their own markup on top, so two borrowers with identical 720 scores can be quoted rates 1 to 3 percentage points apart. This is the part of the answer the SERP largely skips.

There are two distinct effects at play.

Lender-specific pricing

Different lenders have different funding costs, different appetite for auto risk, and different model assumptions about default. A credit union with a low cost of capital and a "member rewards" pricing philosophy will routinely beat a captive lender (the manufacturer's finance arm) by half a point on the same borrower profile. Captives sometimes win the other way around when they layer in a manufacturer subsidy. Online direct lenders price aggressively on prime borrowers and conservatively on near-prime.

The practical takeaway: the rate any one lender quotes you is a sample of one. Federal Trade Commission guidance and Consumer Financial Protection Bureau best-practice both suggest comparing offers from at least three lenders before signing (CFPB Auto Finance Tools).

Dealer markup on indirect loans

When a dealer arranges your loan instead of you bringing your own preapproval, the loan goes through an indirect-finance arrangement. The lender quotes the dealer a buy rate for your profile. The dealer is then permitted (in most states) to offer you a contract rate higher than the buy rate, and the dealer keeps the difference as a finance reserve.

A typical dealer markup runs 1 to 2 percentage points. On a 60-month $30,000 loan, that's roughly $30 per month or $1,800 over the loan's life, money that goes to the dealer's finance department, not the lender. Some captive financing programs cap the markup; some lenders prohibit it entirely; the FTC's 2024 Combating Auto Retail Scams (CARS) Rule introduced new disclosure requirements that made some markup practices easier to spot but did not eliminate them (FTC CARS Rule).

The simplest defense is to walk in with a preapproval from a bank or credit union before negotiating the rate at the dealership. The dealer then has to beat your outside rate to win the financing, flipping the buy-rate / contract-rate spread back in your favour.

0% APR offers versus cash rebates: which is actually cheaper

A 0% APR offer is not always the cheapest path; many manufacturer 0% APR programs require forfeiting a $1,500 to $4,000 cash rebate that, when taken instead, funds a smaller principal that produces less total interest at 5 to 6% APR than the headline 0% APR loan would. This is the second piece of conventional wisdom that misleads buyers.

Worked example. A new vehicle has a $35,000 sticker price. The manufacturer is offering one of two incentives, either-or:

- Option A: 0% APR financing for 60 months on the full $35,000.

- Option B: $2,500 cash rebate plus a 6.27% APR (the prime average) financing on $32,500.

The total cost of Option A is exactly $35,000 ($583 per month over 60 months, no interest).

The total cost of Option B is the financed principal plus interest: a 60-month loan at 6.27% APR on $32,500 produces a monthly payment of about $632 and roughly $5,440 in total interest, for a total out-of-pocket of $37,940. In this case, 0% APR wins by about $2,940.

But change the rebate to $4,000 and the math flips. Option B becomes a $31,000 loan at 6.27%, monthly payment $603, total interest $5,189, total out-of-pocket $35,189, meaning the rebate-and-finance option costs only $189 more than 0% APR on the full price, and a single percentage-point lower rate (5.27% APR) tips it to cheaper. For the underlying APR-versus-interest-rate distinction these comparisons hinge on, see is APR the same as the interest rate.

The breakeven moves with the term length, the rebate size, and the alternative APR you can secure. A simple rule: if the cash rebate divided by the financed amount exceeds your alternative APR over the loan term, take the rebate. Otherwise, take the 0% APR.

If a salesperson tells you the 0% APR is automatically the best deal, run both numbers yourself before signing.

What moves your rate beyond your credit score

Several factors apart from your score push your final rate up or down by significant amounts: term length, down payment, debt-to-income ratio, vehicle age, and whether the loan is direct or indirect. Knowing how each one moves the rate lets you tune the loan structure before applying.

- Term length. A 72- or 84-month loan typically carries a rate 0.25–0.75 percentage points higher than a 60-month loan because the lender holds the default risk for longer. The longer term lowers the monthly payment but increases total interest.

- Down payment. A larger down payment reduces the loan-to-value ratio. Most lenders price below 80% LTV one way and above 90% LTV another. Putting 15–20% down often saves a quarter to half a percentage point even at the same credit score.

- Debt-to-income ratio. Lenders looking at a thin file or a high DTI (above ~40%) tighten pricing or request a co-signer. CFPB analysis of HMDA data shows DTI as the second-strongest predictor of approval after credit score itself.

- Vehicle age. Used vehicles older than 5–7 years are sometimes priced 1–3 percentage points above the standard used-car rate because the collateral value erodes faster.

- Direct vs indirect loan. A direct loan from a bank or credit union (you walk into the lender) usually beats the indirect-financing rate at the dealer (the dealer arranges the loan) by 0.5–2.0 percentage points. The dealer markup discussed above is the main reason.

These factors are partially independent of one another. A super-prime borrower can still get a mediocre rate by financing a 7-year-old vehicle on an 84-month term at a dealer with full markup, and a near-prime borrower can punch above their tier by walking in with a 60-month preapproval, 20% down, and a 4-year-old vehicle.

How to verify what rate you actually qualify for

The fastest way to find your real rate is to get prequalified by 2 or 3 lenders before stepping onto a dealer lot. Prequalification is a soft credit pull that does not affect your score, and the resulting estimate is far more accurate than online rate-by-tier averages.

A practical sequence:

- Check your credit score for free through your bank, credit card issuer, or directly via a credit bureau. Confirm the tier you're in.

- Pull your free credit reports through annualcreditreport.com and dispute any errors. Even a 20-point correction can move you across a tier boundary.

- Get prequalified by your primary bank or credit union. Most will return an indicative APR within 1–2 business days from a soft pull.

- Get prequalified by an online direct lender (Capital One Auto Navigator, Bank of America, Chase Auto, and many credit-union APIs offer this). Compare the APRs.

- When you visit the dealership, share that you have outside financing already and ask if the dealer can beat it. The dealer's quote (their buy rate plus any markup) is your benchmark.

If the dealer's quote is not at least 0.5 percentage points lower than your best outside quote, take your outside financing.

The disclosures the dealer must give you under the Truth in Lending Act, Regulation Z, include the APR, the finance charge, the total amount financed, the total of payments, and the total sale price (CFPB Reg Z). Read them. Ask which rows are negotiable. The APR is.