What credit score is needed to buy a house?

The minimum credit score for buying a house in the United States ranges from 500 (FHA with 10% down) to 700+ (jumbo loans), with most borrowers landing at the 580 to 620 entry point depending on which mortgage program they choose. The four main programs (FHA, VA, USDA, conventional) each publish their own floor, and most lenders add an "overlay" raising the floor by 20 to 60 points. The score you need depends as much on which lender you go to as on which program you choose (HUD).

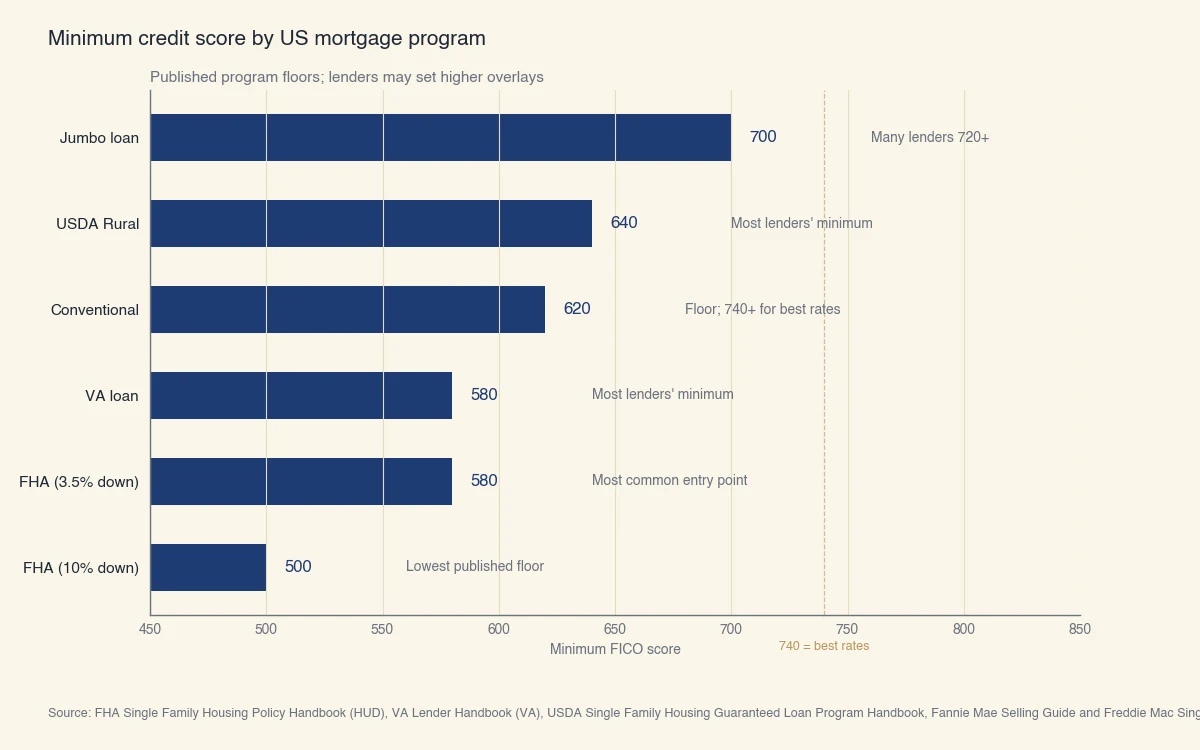

The chart below shows each program's published minimum. Practical experience: assume 20 to 40 points above the published floor as the realistic minimum to find a lender without overlays.

Source: FHA Single Family Housing Policy Handbook (HUD), VA Lender Handbook (VA), USDA Single Family Housing Guaranteed Loan Program Handbook, Fannie Mae Selling Guide and Freddie Mac Single-Family Seller / Servicer Guide. Lender overlays may set higher minimums.

Why the threshold matters in dollars: the difference between a 620 and a 740 score on a $400,000 30-year mortgage is approximately $200 to $300 a month, or $70,000 to $100,000 over the life of the loan, depending on prevailing rates. The score also affects mortgage insurance premiums, down-payment requirements, and which lenders will work with you at all.

What's a credit-score overlay?

A lender overlay is a credit standard that exceeds what the program (FHA, VA, etc.) requires. HUD allows FHA loans down to 500, but most banks set their FHA overlay at 580 or 620 to limit risk. Overlays explain why two borrowers with the same score can get different answers from different lenders. Shopping at least three lenders is standard advice for borrowers near the floor, and in some cases a local lender can lower your interest rate to win your business.

What is the minimum credit score for an FHA loan?

FHA's published minimum is 500 with 10% down or 580 with 3.5% down, but most FHA-approved lenders apply an overlay raising the practical minimum to 580 or 620. FHA loans are insured by the Federal Housing Administration (a HUD subsidiary) and were designed specifically to widen access to homeownership for borrowers with imperfect credit (HUD).

The FHA program is the most common entry point for first-time buyers because it combines:

- A 580 minimum FICO with only 3.5% down

- Down-payment assistance programs that work with FHA

- Acceptance of higher debt-to-income ratios than conventional loans (up to 50% in some cases)

- Looser underwriting on past credit events: a 2-year wait after Chapter 7 bankruptcy and 3 years after foreclosure, vs. 4 and 7 years for conventional

The trade-off is the mortgage insurance premium (MIP). FHA borrowers pay an upfront 1.75% MIP at closing plus an annual MIP that ranges from 0.55% to 0.75% of the loan amount, paid monthly for the life of the loan if the down payment was below 10%. Conventional loans cancel mortgage insurance once the borrower reaches 20% equity.

What credit score is needed for a conventional mortgage?

The published minimum for a conventional Fannie Mae or Freddie Mac conforming mortgage is 620, but pricing tightens significantly above 660 and again above 740. Conventional loans are not federally insured; instead they're sold to or guaranteed by Fannie Mae and Freddie Mac, the two government-sponsored enterprises that buy most US mortgages from originating lenders (Fannie Mae).

The pricing penalty across credit tiers is steep. The table below shows the typical rate spread vs. a 740-score borrower at the same point in time, on a 30-year conforming loan with 20% down:

| FICO | Approximate rate premium | Roughly translates to |

|---|---|---|

| 760+ | Best published rate | Baseline |

| 740-759 | +0.10 to +0.15 pp | $20-30 / month on $400K |

| 720-739 | +0.20 to +0.30 pp | $40-60 / month |

| 680-719 | +0.40 to +0.60 pp | $90-130 / month |

| 660-679 | +0.60 to +0.85 pp | $130-180 / month |

| 640-659 | +0.85 to +1.20 pp | $180-260 / month |

| 620-639 | +1.20 to +1.75 pp | $260-380 / month |

These are approximations. The exact "loan-level price adjustment" (LLPA) Fannie and Freddie charge depends on the down-payment percentage too. Higher down payment partially offsets a lower score; lower down payment amplifies the score penalty.

What about jumbo loans?

A jumbo loan is any mortgage above the conforming loan limit set annually by the Federal Housing Finance Agency (around $766,550 for most counties in 2024-2026, higher in expensive markets). Jumbo loans cannot be sold to Fannie or Freddie, so the underwriting standards are stricter:

- Most jumbo lenders require a 700 minimum FICO; many require 720 or 740

- Down-payment requirements run 10% to 20% (vs. 3% conventional, 3.5% FHA)

- Reserves of 6 to 12 months of mortgage payments are common

- Debt-to-income caps at 43% are typical, with some lenders allowing 45%

If you're shopping in a market where jumbo financing is common, a 740+ score is effectively the entry ticket. Below 700 the lender pool shrinks dramatically.

What credit score do you need for a VA or USDA loan?

The VA does not set a minimum credit score for VA-guaranteed home loans, leaving the floor to individual lenders who typically set theirs at 580 or 620; USDA loans for rural properties require 640 at most lenders. Both programs are federal, both reduce or eliminate the down payment requirement, and both have stricter income and property-type rules than FHA or conventional (VA).

VA loan eligibility highlights:

- Borrower: veterans, active-duty service members, and qualifying spouses

- Down payment: zero is allowed; most VA borrowers put nothing down

- Mortgage insurance: none (replaced by a one-time funding fee of 1.25% to 3.30%)

- Credit floor: the VA itself has none, but most lenders require 580-620

USDA loan eligibility highlights:

- Property: must be in a USDA-designated rural area (the USDA online map identifies eligible addresses)

- Income: household income capped at 115% of the area median income

- Down payment: zero is allowed

- Credit floor: the USDA Single Family Housing Guaranteed Loan Program does not set a minimum, but most lenders require 640

Both programs accept scores below their lender's typical minimum if the borrower has compensating factors like a co-borrower, reserves, or a low debt-to-income ratio. Manual underwriting (vs. the automated underwriting most loans use) is the route for borrowers who fall between the published floor and the lender's overlay.

How is the mortgage credit score different from a regular credit score?

Mortgage lenders pull a tri-merge credit report from all three bureaus (Equifax, Experian, TransUnion) and use the middle score, not the highest or the lowest. For joint applicants, the lender uses the lower of the two middle scores.

Mortgage scores also use older versions of the FICO model (typically FICO 2 from Experian, FICO 4 from TransUnion, and FICO 5 from Equifax) rather than the newer FICO 8 or 9 you see on consumer apps. The older models weight some factors slightly differently, so it's normal for your "mortgage FICO" to come back 10 to 30 points different from the score you saw on Credit Karma or your bank's app the day before.

The takeaway: do not assume the score on a consumer app is what the lender will see. Ask the loan officer to pull the tri-merge early in the conversation so you can negotiate from the actual number that will price the loan.

What can you do if your score is below the program minimum?

Borrowers within 20 to 40 points of a program minimum can usually move into qualifying territory in 60 to 90 days through three concrete moves: pay down revolving balances below 30% of the limit, dispute any reporting errors on the tri-merge report, and avoid every new hard inquiry until after closing. Larger gaps take 6 to 12 months and require building positive payment history rather than fixing utilization.

The fastest score levers, in order of typical impact:

- Utilization. A credit card balance reported above 30% of the credit limit can drop scores 20 to 50 points. Paying down to below 10% before the statement closing date can reverse the drop within one billing cycle.

- Old delinquencies. A single 30-day late payment from years ago can hold a score 30 to 80 points below where it would otherwise be. Goodwill letters to the original creditor occasionally succeed in removing them.

- Credit-report errors. The CFPB has documented that roughly 1 in 5 US credit reports contain a meaningful error. Disputing and resolving an error typically takes 30 to 45 days.

- Hard-inquiry restraint. Every new hard pull can shave 5 to 10 points temporarily. Avoid all non-essential applications during the 90 days before mortgage application. To see how the score you have today translates into a maximum purchase price at current rates, run your numbers through the mortgage affordability calculator.

What does NOT help in the short term: closing old credit cards (this hurts utilization and history), applying for a new card to "build credit fast" (the inquiry penalty exceeds the file-thickness gain), or paying for credit-repair services that promise score increases. The Federal Trade Commission has consistently warned consumers that legitimate score improvement comes only from changes the borrower can make themselves. For a step-by-step guide tailored to each starting tier, see how to boost a US credit score. To understand the human side of the file review after you apply, see what a mortgage underwriter actually does.