What is home loan underwriting?

Home loan underwriting is the process a mortgage lender uses to verify your finances and the property, then decide whether lending to you is an acceptable risk. After you submit a mortgage application, an underwriter (the person or automated system that makes the credit decision) checks your income, debts, assets, and credit against the lender's rules and the value of the home before any money changes hands (CFPB).

Underwriting answers one question: if the lender gives you this loan on this house, how likely are you to repay it, and how well does the property protect the lender if you do not? Everything the underwriter does maps back to that single risk question.

Most files today first run through an automated underwriting system (AUS), software that scores the application against the investor's rules. The two that handle the bulk of US mortgages are Fannie Mae's Desktop Underwriter and Freddie Mac's Loan Product Advisor. A human underwriter still reviews the output, clears conditions, and signs off.

What does a home loan underwriter actually check, with the math?

An underwriter measures your file against four numbers: your debt-to-income ratio, your loan-to-value ratio, your cash reserves, and your credit score. Lenders organize these into the four Cs of credit, sometimes a fifth:

| The C | What it means | What it feeds |

|---|---|---|

| Capacity | Can you afford the payment? | Debt-to-income (DTI) ratio |

| Credit | Do you pay on time? | Credit score and report |

| Collateral | Is the home worth the loan? | Loan-to-value (LTV) ratio from the appraisal |

| Capital | Do you have skin in the game? | Down payment and cash reserves |

| Conditions | Do the loan terms and economy fit? | Rate, term, and loan purpose |

The two ratios decide most files, so it helps to see them on a real applicant. Take a borrower earning $90,000 a year ($7,500 gross per month) buying a $400,000 home with 20% down ($80,000), leaving a $320,000 loan at a 6.75% 30-year fixed rate. They carry $700 a month in a car payment and student loans, and they keep $15,000 in the bank after the down payment.

| Underwriting check | Calculation | Result | Typical limit |

|---|---|---|---|

| Loan-to-value (LTV) | $320,000 / $400,000 | 80% | At or below 80% avoids PMI |

| Housing payment (PITI) | $2,076 P&I + $400 tax + $100 insurance | $2,576 / month | n/a |

| Front-end DTI | $2,576 / $7,500 | 34.3% | About 28% to 31% preferred |

| Back-end DTI | ($2,576 + $700) / $7,500 | 43.7% | Up to 45%, or 50% via AUS |

| Cash reserves | $15,000 saved vs. $5,152 (2 months PITI) | Clears | Often 2 to 6 months |

The front-end DTI is the housing payment alone against income; the back-end DTI adds every other monthly debt. This borrower's back-end DTI of 43.7% slips under the 45% line that manual underwriting allows and well under the 50% an automated approval can reach (Fannie Mae). The 80% LTV means no private mortgage insurance, and the reserves cover more than two months of payments. On paper, this file approves. Push the back-end DTI past 45% or let the appraisal come in low, and the same file needs a compensating factor or a denial.

What are the steps in the home loan underwriting process?

Underwriting moves through a fixed sequence: application, document verification, appraisal, title search, and the underwriter's decision, then closing. Each step feeds the underwriter another piece of the risk picture:

- Application and document collection. You submit the application and supporting paperwork. Expect pay stubs, two years of W-2s or 1099s, bank and asset statements, and two years of tax returns if you are self-employed.

- Verification. The underwriter confirms the documents are real and consistent. They re-check employment, trace large deposits, and recalculate your income from the source documents rather than taking the application at face value.

- Appraisal. A licensed appraiser values the home. This sets the collateral figure and your LTV. A low appraisal is one of the most common reasons a clean file suddenly needs more cash or a price renegotiation.

- Title search. A title company confirms the seller can legally transfer the home and that no liens or ownership disputes cloud it.

- The decision. The underwriter issues one of four outcomes (below) and, if conditions apply, lists exactly what you must provide to reach a final clear to close.

- Closing. Once conditions clear, you sign and the loan funds.

Underwriting itself often takes only a few days, but the full path from application to a funded loan runs about 40 to 50 days. Most delays trace back to missing documents or appraisal scheduling, not the underwriter's speed.

What can the underwriter decide, and what really happens to applications?

An underwriter returns one of four answers: approved, approved with conditions, suspended, or denied. Conditional approval is the normal path, not a warning sign. Here is what each means and what you do next:

| Decision | What it means | Your next step |

|---|---|---|

| Approved | The file meets every rule with no outstanding items | Move to closing |

| Approved with conditions | Approved once you supply specific items (a letter of explanation, an updated statement) | Send the conditions, then get the clear to close |

| Suspended | The underwriter needs more information before deciding | Provide what is requested; the file is paused, not rejected |

| Denied | The file does not meet the lender's rules | Read the adverse-action notice, fix the issue, or reapply elsewhere |

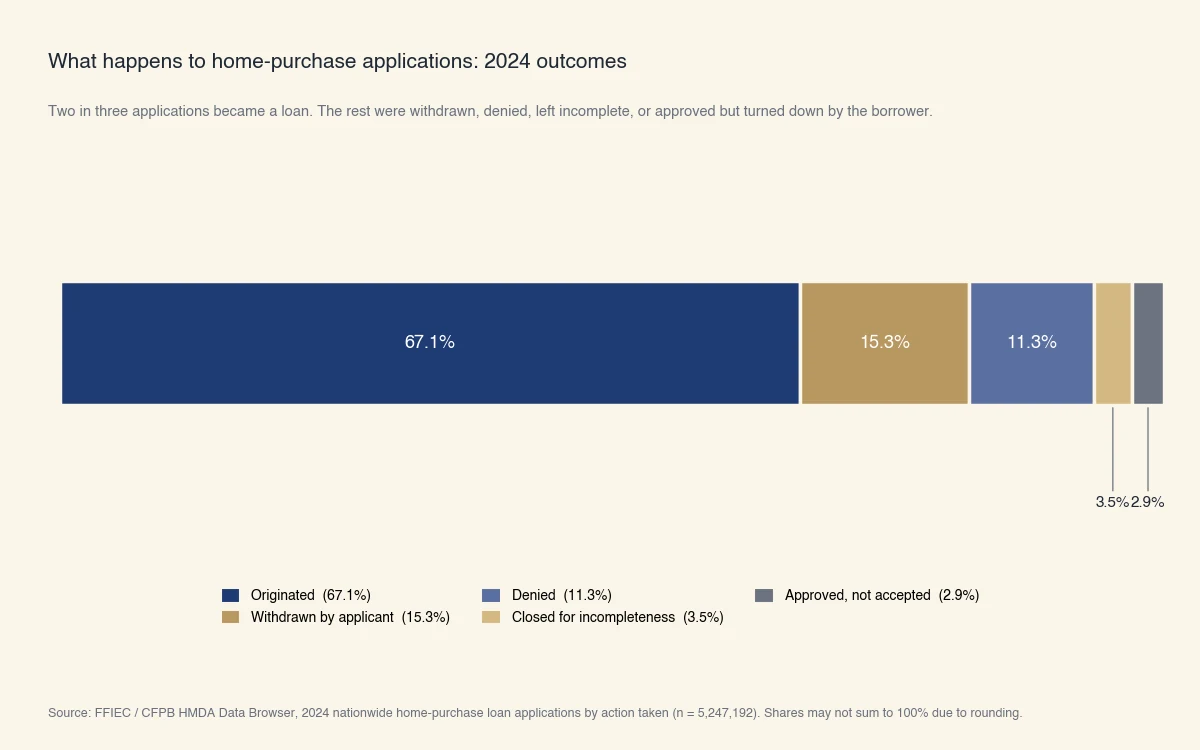

It also helps to see the real-world odds. Of every home-purchase mortgage application reported nationwide in 2024, about two in three became a loan; the rest were withdrawn by the borrower, denied, left incomplete, or approved but turned down by the applicant.

Source: FFIEC / CFPB HMDA Data Browser, 2024 nationwide home-purchase loan applications by action taken (n = 5,247,192). Shares may not sum to 100% due to rounding.

Notice that outright denials (11.3%) are smaller than applicant withdrawals (15.3%). Many files never reach a denial because the borrower walks away first, often after a low appraisal or a rate move. The chart is the funnel behind the four decisions above.

Common myths about home loan underwriting

The biggest underwriting mistakes come from believing the loan is done before it is. Four myths cause most of the surprises:

- "Preapproval means I am approved." Preapproval is an early estimate based on a light review, not an underwriting decision (CFPB). The full file still has to clear underwriting.

- "A high credit score guarantees approval." Credit is one of four Cs. A 780 score still gets denied if the back-end DTI runs too high or the appraisal comes in below the price. Capacity and collateral can sink a file with perfect credit.

- "Conditional approval is a soft denial." It is the opposite. Most approvals arrive with conditions, a short list of documents the underwriter wants before the final sign-off. Supplying them is routine.

- "An automated approval is final." An "approve/eligible" from Desktop Underwriter or Loan Product Advisor is the start of the human review, not the end. An underwriter still verifies the inputs and clears the conditions before funding.

What are your rights if an underwriter denies your loan?

If your mortgage is denied, federal law gives you the right to know exactly why. Under the Equal Credit Opportunity Act and its Regulation B, the lender must send a written adverse-action notice listing the specific reasons for the denial, usually within 30 days (CFPB). Vague answers like "you did not qualify" do not satisfy the rule; the notice has to name the actual reasons, such as a high debt-to-income ratio or insufficient collateral value.

You are also entitled to a free copy of the home appraisal the underwriter relied on, and you can dispute errors in the credit report or appraisal that drove the decision. A denial is not always permanent. If the reason was a fixable one, paying down a card to lower your DTI, correcting a credit-report error, or bringing more cash to lower your LTV, the same file can pass on a second pass.

This is also where lending is changing. When a borrower sits just outside a lender's rules, traditional underwriting often returns a flat denial. Sphera Credit's role is to make that edge of the credit box more accurate and explainable, so the reasons behind a decision are clear rather than a black box. The goal is a fairer read of borrowers who do not fit the standard template, not a faster rubber stamp.

Key takeaways

Home loan underwriting is the lender's risk check, and it comes down to five things worth remembering:

- It verifies your income, credit, assets, and the property before approving a mortgage.

- The decision rests on four numbers, the four Cs: capacity (DTI), credit, collateral (LTV), and capital (reserves).

- Most approvals come back conditional, and preapproval is never the same as an underwriting approval.

- In 2024, about 67% of US home-purchase applications became loans; more were withdrawn than denied.

- If you are denied, federal law entitles you to a written notice with the specific reasons and a free copy of your appraisal.