How do you become a mortgage underwriter in Canada?

To become a mortgage underwriter in Canada, earn a bachelor's degree in a business or quantitative field, take an entry-level lending role such as loan processor or mortgage administrator, learn the lender's credit policy on the job, then move into a junior underwriter seat. A mortgage underwriter is the person at a bank, credit union, or mortgage lender who decides whether to approve a loan by weighing the borrower's risk against the lender's policy (Job Bank).

The path is built from experience, not from a single licence or exam. Here is the sequence most Canadian underwriters follow:

- Earn a relevant bachelor's degree. Business administration, commerce, economics, or finance are the common choices. A degree that shows strong mathematics and data-analysis skills is an advantage, because underwriting is risk measured in numbers (Job Bank).

- Get an entry-level lending role. Loan processor, mortgage administrator, fulfillment officer, or underwriting assistant roles put you next to real files. You learn how income is documented, what an appraisal says, and how a lender's policy reads in practice.

- Learn the lender's credit policy on the job. Expect up to a year of structured training and supervised work before you decision files on your own. This is where the five Cs of credit (character, capacity, capital, collateral, and conditions) stop being a textbook list and become a working habit.

- Add a designation if your employer values it. Optional credentials like the Accredited Mortgage Professional of Canada (AMPC) signal competence, especially on the broker and non-bank side (Mortgage Professionals Canada).

- Move into an underwriter seat. Once you can assess a file end to end and defend the decision, you apply for or get promoted into a junior or associate underwriter role, then build toward full and senior underwriting.

The two parts of this article that the typical career guide skips are the ones that save you the most time and money: whether you actually need a licence (you probably do not), and what the path looks like year by year. Both are covered below. If you want the wider view of the role first, start with what is an underwriter.

What education, designations, and skills do you need?

You need a bachelor's degree in a business or quantitative discipline, the ability to read financial documents and credit reports accurately, and sound judgement under policy; formal designations are useful but rarely mandatory for an in-house underwriter. Job Bank lists a bachelor's degree in business administration, commerce, economics, or a related field as the usual requirement, with employer training programs layered on top (Job Bank).

The education and credential stack breaks into three tiers:

- Required by most employers: a bachelor's degree, plus the employer's internal credit-policy training. This is the floor.

- Helpful, sometimes expected: courses from the Canadian Securities Institute or comparable institutes, and on the broker and non-bank side, the Accredited Mortgage Professional of Canada (AMPC) designation administered through UBC's Sauder School of Business. The AMPC takes about 40 hours across four courses plus a summative exam, with a 75% pass mark (Mortgage Professionals Canada).

- Specialist and senior: designations such as the CFA or commercial-credit training matter for non-conforming, commercial, and asset-based files, where risk does not reduce to a checklist.

The skills employers screen for are consistent across postings: analytical thinking, attention to detail, clear written and verbal communication, and the confidence to make and defend a decision. Underwriters spend their day applying the five Cs of credit to real applications, verifying income and assets, reading appraisals, and checking each file against the lender's policy and against OSFI's expectations for prudent residential mortgage practice in Guideline B-20.

Do you need a licence to be a mortgage underwriter in Canada?

In most cases, no. An in-house mortgage underwriter employed by a bank or credit union does not need a provincial mortgage-broker or mortgage-agent licence, because that licensing regime covers people who arrange mortgages for the public, not the lender's own staff who assess the lender's risk. Ontario's regulator is explicit that banks and credit unions are exempt from the requirement to be licensed as a mortgage brokerage, broker, agent, or administrator (FSRA).

This is the single most common point of confusion in this topic, and most career guides get it wrong by listing provincial mortgage-agent licensing as a step to becoming an underwriter. The licence and the underwriting job answer two different questions:

| Mortgage underwriter (in-house) | Mortgage broker / agent | |

|---|---|---|

| Works for | The lender | The borrower |

| Job | Approves or declines the lender's risk | Arranges a mortgage from lenders |

| Provincial licence | Generally not required (bank and credit-union staff are exempt) | Required in most provinces |

| Where they sit | Inside a bank, credit union, or lender | At a brokerage |

| Regulated by | The lender's policy and OSFI Guideline B-20 | The provincial regulator (FSRA, BCFSA, and others) |

A mortgage agent or broker licence governs the act of dealing in or arranging mortgages with the public for compensation. In Ontario, for example, FSRA licenses Level 1 agents (who can place a mortgage with a traditional lender like a bank or credit union) and Level 2 agents (who can also use alternative and private lenders) (FSRA). None of that applies to an internal credit adjudicator.

The exception is real and worth stating: if you also originate or arrange mortgages for borrowers, for example at a brokerage or in a hybrid role, then the provincial licence applies to that activity. Before you pay for a licensing course, confirm with your target employer whether the role is internal underwriting or public-facing origination, because they have very different requirements.

What does the career path and timeline look like?

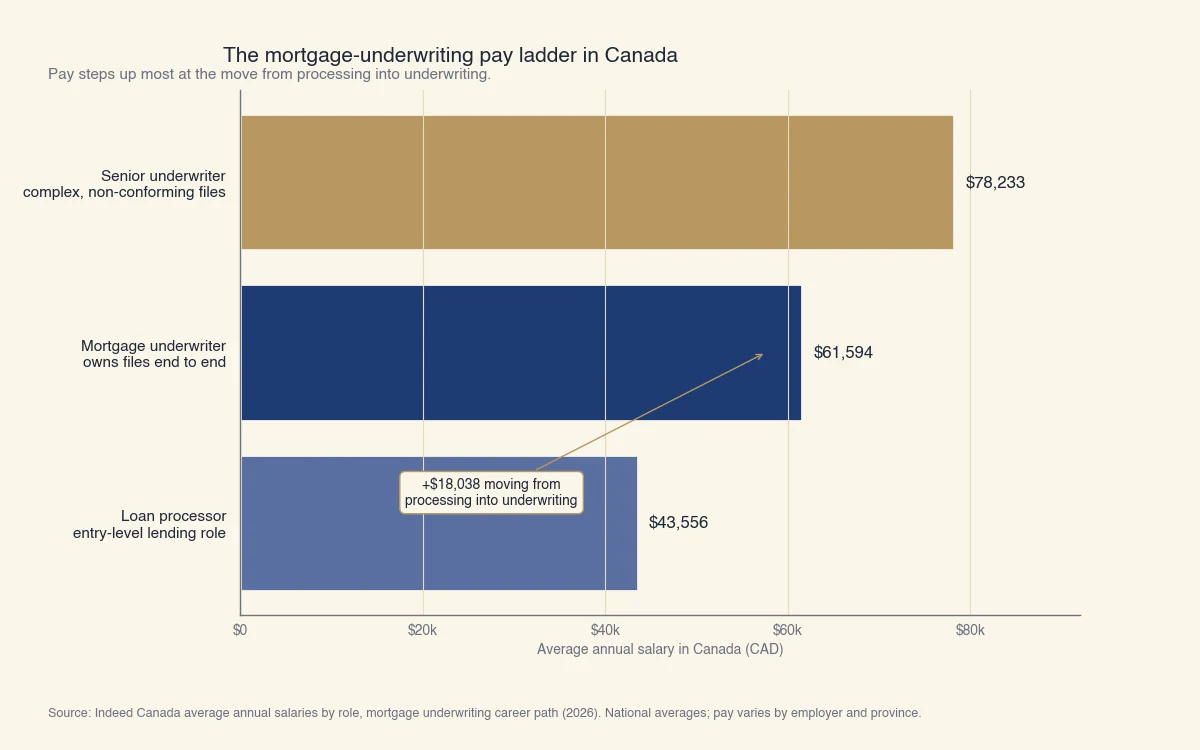

The realistic path runs about four to six years from first-year student to working underwriter: roughly three to four years for the degree, then one to three years in an entry-level lending role before you decision files on your own. Pay climbs at each rung, and the jump from processing to underwriting is where compensation and responsibility both step up.

Here is a concrete progression for a Canadian candidate who starts with a commerce or finance degree:

- Year 0 to 1, loan processor or mortgage administrator (around $43,000). You assemble and verify application packages, order appraisals and credit reports, and clear conditions. You are learning the documents an underwriter relies on.

- Year 1 to 3, junior or associate underwriter (climbing toward the underwriter band). You decision straightforward, policy-conforming files under supervision, then with growing independence. You internalize the lender's risk appetite and OSFI Guideline B-20 expectations.

- Year 3 and beyond, mortgage underwriter (around $61,000). You own files end to end, approve within your authority limit, and escalate exceptions. You can defend any decision against policy.

- Senior underwriter (around $78,000). You handle complex and non-conforming files, mentor juniors, and may hold a higher signing authority.

Source: Indeed Canada average annual salaries by role, mortgage underwriting career path (2026). Figures are national averages and vary by employer and province.

The figures above are national averages; large banks and complex-risk employers pay above them, while smaller regional lenders and B-lenders often pay below (Indeed Canada). For a fuller breakdown of underwriting pay by type of underwriter and employer, see how much do underwriters make.

Is mortgage underwriting a good career in Canada?

Mortgage underwriting offers stable, above-average pay, a clear ladder from processor to senior, and judgement-heavy work that resists automation, which makes it a strong career for analytical people who want to stay close to lending without selling. The trade-off is that routine, policy-conforming files are increasingly decisioned by rules engines and bureau-driven models, so the long-term reward goes to underwriters who build specialized risk expertise.

Two forces shape the outlook:

- Routine decisions are being automated. Prime mortgages that fit OSFI Guideline B-20 cleanly are increasingly handled by models, with the human role reduced to verification. That compresses the value of purely routine underwriting work.

- Complex judgement stays scarce and well paid. Non-conforming mortgages, self-employed borrowers, and commercial files do not reduce to a checklist. The regulatory expectation that the lender, not an algorithm alone, stands behind each approval keeps experienced underwriters in the decision seat.

At Sphera Credit we work on this from the lender side. Our AI agents take on the document-collection and verification work that used to consume junior-underwriter time, and they are built to activate when a borrower falls outside the standard credit box, exactly the files where a human's judgement matters most. The point is accuracy and explainability on hard files, not pushing more volume through. For someone entering the field today, that division of labour is the signal: build the judgement that complex risk demands, and the routine work that machines do better will not define your career.

If you are weighing the field more broadly, two related reads help: should I be worried about underwriting for the borrower's view of the process, and how long does underwriting take for what the job actually produces day to day.