What is underwriting in real estate?

Real estate underwriting is the lender's risk assessment that decides whether to fund a property loan, for how much, and on what terms. An underwriter verifies the borrower's income, credit, and existing debt, then assesses the property itself through an appraisal, and produces a decision: approve, decline, or approve with conditions (FCAC).

Underwriting sits between a pre-approval and the money being advanced. A pre-approval is an early estimate based on stated numbers. Underwriting is the real check, where the lender confirms every figure against documents and the property, then commits actual funds.

Two things make real estate underwriting different from a plain personal loan review. First, the loan is secured by the property, so the lender appraises the asset and lends against its value. Second, the loan amounts are large and long, so small differences in risk change the rate and the terms a borrower receives. Both the borrower and the property have to pass.

What does a real estate underwriter check?

A real estate underwriter checks two things in parallel: the borrower's ability to repay, and the property's value as security. The borrower side answers "will this person make the payments?" and the property side answers "if they stop, can the lender recover the loan?"

On the borrower side, the underwriter reviews:

- Income and employment -- pay stubs, T4s, notices of assessment, and for self-employed applicants, two years of business financials.

- Credit history -- the credit bureau report, scores, and any past defaults, collections, or bankruptcies.

- Debt load -- existing loan payments, credit-card minimums, and other obligations, expressed as debt-service ratios.

- Down payment and its source -- how much equity the borrower brings, and proof the funds are genuine savings rather than undisclosed borrowing.

On the property side, the underwriter orders an appraisal, an independent estimate of the property's market value, to confirm the price is supported and to set the loan-to-value (LTV) ratio. LTV is the loan amount divided by the property value: a $400,000 loan on a $500,000 home is an 80% LTV. The underwriter also checks the title, the property type, and how easily the asset could be resold.

Most lenders run the file first through an automated rules engine, then send anything the engine cannot score cleanly to a human for manual underwriting. Self-employed income, a thin credit file, a newcomer to Canada, or an unusual property are the classic triggers for a manual review.

How does real estate underwriting work in Canada?

In Canada, residential real estate underwriting runs on a national rulebook: OSFI Guideline B-20, the mortgage stress test, and the debt-service-ratio limits used by the default insurers. Every federally regulated lender underwrites residential mortgages to these standards (OSFI).

Three rules shape almost every Canadian mortgage decision:

- The stress test (minimum qualifying rate). Lenders must qualify you not at your contract rate, but at the greater of your contract rate plus 2% or 5.25%. If your mortgage rate is 4.5%, you must still show you could afford payments at 6.5%. This is the single most common reason an otherwise-affordable file is cut back.

- Debt-service ratios (GDS and TDS). Gross Debt Service (GDS) is your housing costs (mortgage, property tax, heat, and half of any condo fees) divided by gross income. Total Debt Service (TDS) adds all your other debt payments. For insured mortgages, CMHC caps GDS at 39% and TDS at 44% (CMHC).

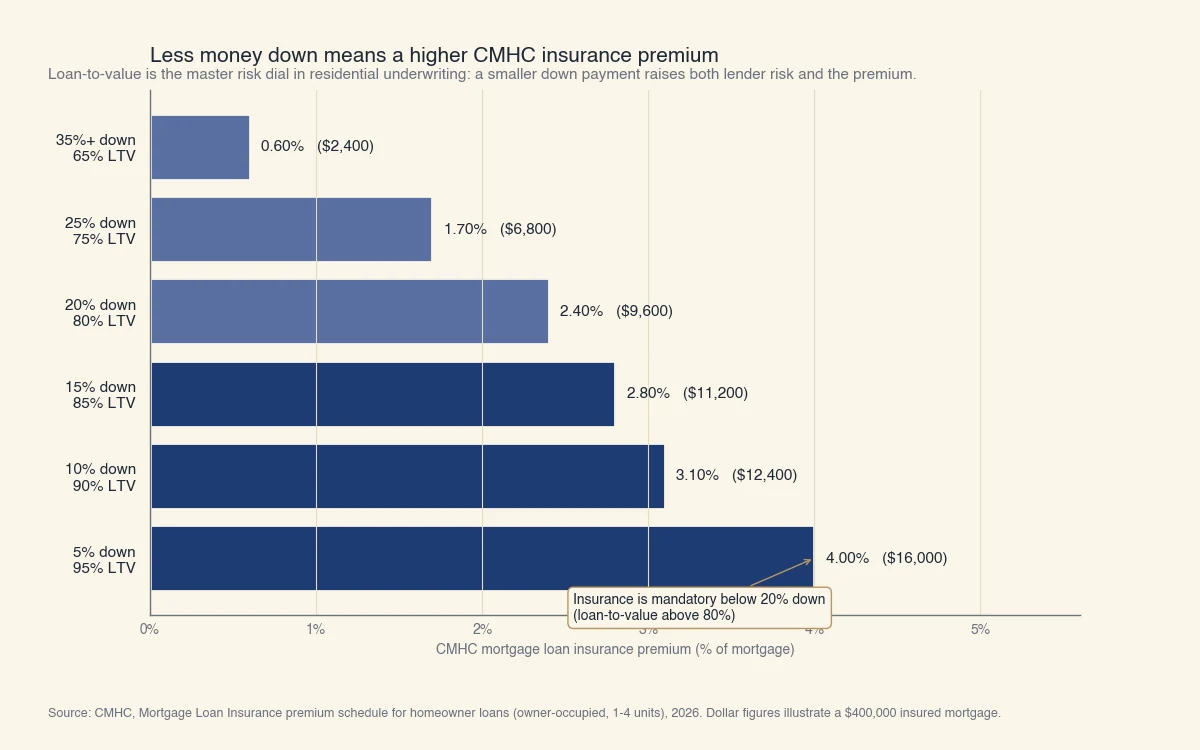

- Mortgage default insurance. When your down payment is under 20% (an LTV above 80%), the loan is "high-ratio" and you must buy default insurance from CMHC, Sagen, or Canada Guaranty. The premium is added to your mortgage.

A worked GDS / TDS example

Take a household with $120,000 gross annual income, which is $10,000 a month:

- Mortgage payment: $2,800

- Property tax: $400

- Heat: $150

- Housing total: $3,350 → GDS = 33.5% (under the 39% limit)

- Car loan and card minimums: $600

- All-in total: $3,950 → TDS = 39.5% (under the 44% limit)

This file passes on ratios. The underwriter would then re-run the housing payment at the stress-test rate to confirm it still fits. These numbers are illustrative; your lender uses your actual figures.

The down payment matters beyond just the ratios, because it sets your LTV and therefore your insurance premium. The smaller the down payment, the higher the lender's risk and the higher the CMHC premium, as the schedule below shows.

Source: CMHC, Mortgage Loan Insurance premium schedule for homeowner loans (owner-occupied, 1-4 units), 2026. Dollar figures illustrate a $400,000 insured mortgage.

Residential vs commercial real estate underwriting: what's the difference?

Residential underwriting sizes the loan to the borrower's personal income, while commercial underwriting sizes it to the property's own cash flow. That single difference changes which numbers matter, who reviews the file, and how long it takes.

| Factor | Residential | Commercial |

|---|---|---|

| Main question | Can this person afford the payments? | Does the property earn enough to cover the loan? |

| Key ratios | GDS, TDS, LTV, stress test | DSCR, cap rate, LTV, debt yield |

| Income looked at | Borrower's salary and employment | Property's net operating income |

| Decision driver | Scorecard plus debt-service limits | Custom analysis, often a credit committee |

| Typical timeline | 1 to 10 days | 30 to 90 days |

On the commercial side, the underwriter starts from net operating income (NOI), the property's rent minus its operating expenses, then applies three checks:

- Debt service coverage ratio (DSCR) -- NOI divided by the annual loan payment. Lenders typically want a DSCR of 1.25 or higher, meaning the property earns 25% more than the debt costs.

- Capitalization rate (cap rate) -- NOI divided by property value, used to value the asset.

- Debt yield -- NOI divided by the loan amount, a rate-independent check on how leveraged the deal is.

A worked commercial example

Suppose a property produces $100,000 in NOI, the market cap rate is 8%, and the lender allows a maximum 75% LTV with a required 1.25 DSCR at a 7% rate over a 20-year amortization:

- Value from the cap rate: $100,000 ÷ 8% = $1,250,000

- Maximum loan by LTV: 75% × $1,250,000 = $937,500

- Maximum loan by DSCR: the payment can be at most $80,000 a year, which supports roughly $859,000

- The lower number wins, so the loan is capped at about $859,000.

Here the DSCR is the binding constraint, not the LTV. Knowing which constraint binds is the heart of commercial underwriting, because it tells the borrower whether more equity or more property income would support a larger loan.

How long does real estate underwriting take, and how can you improve your odds?

A clean residential file is often underwritten in 24 to 72 hours, but missing documents or manual review can stretch that to one or two weeks, and commercial files run far longer. The process moves through four stages: application, verification, appraisal, and decision with conditions.

To move through underwriting faster and improve your odds of approval:

- Send a complete file up front. Income documents, down-payment proof, and the purchase agreement together. The most common delay is a back-and-forth over missing paperwork.

- Keep your debt and credit stable. Do not open new loans or run up cards between pre-approval and funding. The underwriter re-checks at the end.

- Leave room under the ratios. A larger down payment lowers both your LTV and your insurance premium, and it gives the stress test more cushion.

- Match the property to the lender. Unusual properties (rural, mixed-use, very small units) narrow your lender options; ask before you make an offer.

One point catches many buyers off guard: a mortgage pre-approval is not final approval. The lender re-verifies your income, credit, and the appraised value during underwriting, and the stress test qualifies you at a rate higher than the one you will actually pay. A pre-approval tells you the likely ceiling; underwriting is where the loan becomes real.

This is also where modern lending is changing. When a borrower falls outside the standard automated box, such as self-employed income or a thin credit file, the file goes to slower manual review. Sphera Credit's work focuses on exactly those cases: giving underwriters better, explainable information on the borrowers the automated system cannot score cleanly, so the decision is accurate rather than just fast. For the wider picture, see what underwriting is, what an underwriter does, and how the same risk check applies in underwriting in business development. For the mortgage-specific role, see what a mortgage underwriter does, and for timing, how long underwriting takes.