What is the interest rate in Canada right now?

There is no single "interest rate in Canada." As of June 10, 2026, the Bank of Canada policy rate is 2.25%, the prime rate at the major banks is 4.45%, and the rate you actually pay ranges from about 3.95% on a variable mortgage to roughly 20.99% on a credit card. When people ask this question, they usually mean one of three different rates (Bank of Canada).

The three rates people mean:

- The policy rate (2.25%) is the rate the Bank of Canada sets. It is the anchor for everything else, but almost no consumer borrows or saves at this rate directly.

- The prime rate (4.45%) is the rate each commercial bank lends to its most creditworthy customers. Variable mortgages, lines of credit, and many other products are priced against prime.

- Your product rate is what you personally pay or earn. It sits on top of prime (for borrowing) or below it (for savings) depending on the product and your credit profile. It is, in the end, the rate of interest you actually pay.

The rest of this page walks through each rate, shows how one central-bank number fans out into what Canadians actually pay, and works a dollar example so the percentages feel concrete.

What is the Bank of Canada policy rate and how is it set?

The Bank of Canada policy rate, formally the target for the overnight rate, is 2.25% as of June 10, 2026, after the Bank held it steady for the fifth consecutive meeting. The overnight rate is the interest banks charge each other to borrow funds overnight, and the Bank sets a target for it to steer the whole economy (Bank of Canada).

The Bank announces its decision on eight fixed dates each year. Alongside the 2.25% target, the related Bank Rate (the rate the Bank charges on short-term loans to financial institutions) sits at 2.50%, and the deposit rate sits at 2.20%.

How the Bank decides

The Bank's job is to keep inflation low and stable, with a 2% target inside a 1% to 3% range. When inflation runs hot, the Bank raises the policy rate to cool spending. When the economy weakens, it cuts the rate to encourage borrowing and investment.

At the June 2026 decision, the Governing Council chose to wait. Headline inflation rose to 2.8% in April 2026, driven mostly by energy prices, while core inflation eased to 2.1%. The Council pointed to rising energy costs, supply-chain disruptions, and global uncertainty on one side, and weak domestic activity on the other, so it held rather than moved (Bank of Canada).

Why the policy rate matters even though you do not pay it

You never borrow at 2.25%, but that number sets the floor for every other rate in the country. A change of 0.25 points at the Bank of Canada flows through to prime within days, and from prime into variable mortgages and lines of credit. The policy rate is the lever; the rates you pay are what the lever moves.

What is the prime rate in Canada?

The prime rate in Canada is 4.45% as of June 2026, and it tracks the Bank of Canada policy rate plus a spread of about 2.20 percentage points. The prime rate is the benchmark each bank uses to price its variable-rate lending to strong borrowers (FCAC).

Because prime equals the policy rate plus roughly 2.20 points, the math is direct: a 2.25% policy rate produces a 4.45% prime rate. When the Bank of Canada cuts by 0.25 points, prime almost always falls by the same 0.25 points within a day or two.

The Big Six banks (RBC, TD, Scotiabank, BMO, CIBC, and National Bank) almost always post the same prime rate, so "prime" is effectively one national number. Each bank can set its own, but competition keeps them aligned.

A few products are priced as prime plus or minus a margin:

- A variable-rate mortgage is often quoted as prime minus a discount (for example, prime minus 0.50%).

- A home equity line of credit (HELOC) is usually prime plus about 0.50%.

- An unsecured personal line of credit is typically prime plus 2 to 7 points, depending on your credit, and what drives line of credit interest rates explains why that margin varies so much between lenders.

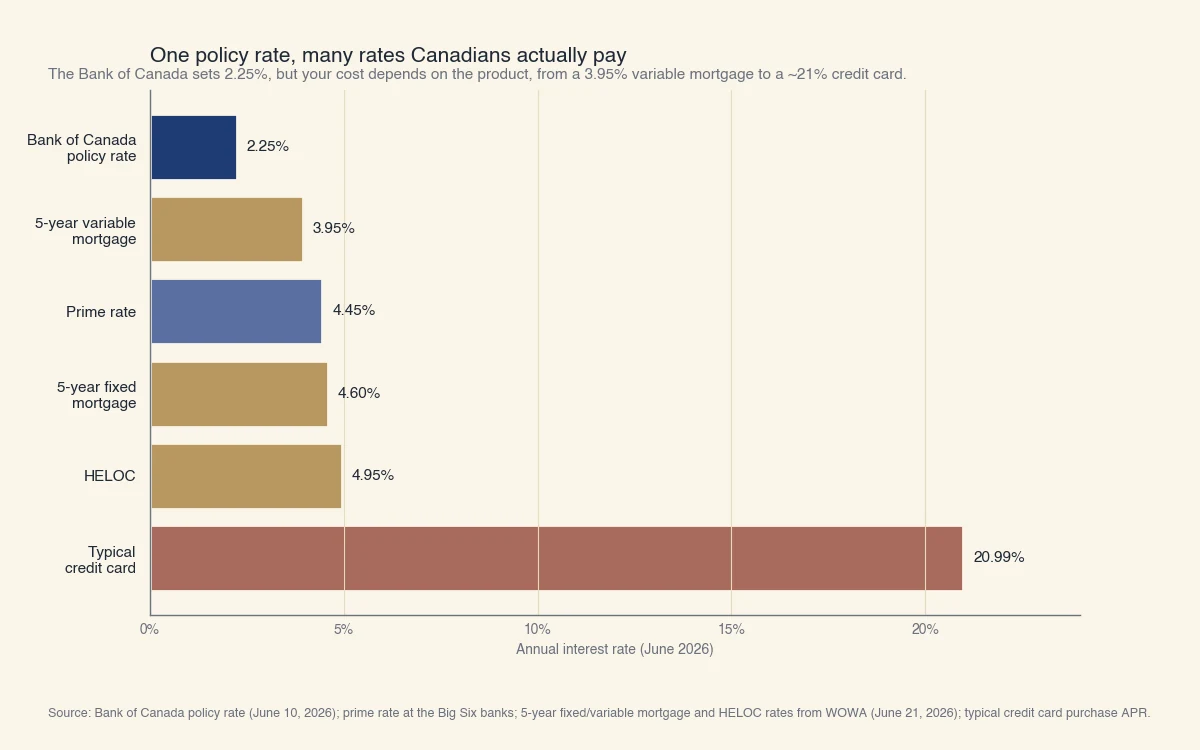

What interest rates do Canadians actually pay?

One central-bank rate of 2.25% turns into a wide ladder of rates once it reaches consumers, from about 3.95% on a 5-year variable mortgage to roughly 20.99% on a typical credit card. The product you choose matters far more than the policy rate itself.

Source: Bank of Canada policy rate (June 10, 2026); prime rate at the Big Six banks; mortgage and HELOC rates from WOWA (June 21, 2026); typical credit card purchase APR.

Here is the same ladder as a table, with what each rate is tied to:

| Rate | June 2026 level | Tied to |

|---|---|---|

| Bank of Canada policy rate | 2.25% | Set by the Bank of Canada |

| 5-year variable mortgage | ~3.95% | Prime minus a discount |

| Prime rate | 4.45% | Policy rate + ~2.20 points |

| 5-year fixed mortgage | ~4.60% | Government of Canada bond yields |

| HELOC | ~4.95% | Prime + ~0.50% |

| Typical credit card | ~20.99% | Set by the card issuer |

Two things stand out. First, fixed-rate mortgages do not follow prime. A fixed rate is set from Government of Canada bond yields, so it can rise or fall even when the Bank of Canada holds steady. Second, the credit card sits far above everything else. No Bank of Canada cut will make a 20.99% card cheap, which is why carrying a card balance is the most expensive common form of borrowing in Canada.

What does the interest rate mean for your monthly payments?

On a $400,000 mortgage at the current 3.95% variable rate over 25 years, the monthly payment is about $2,100, and each 0.25-point move by the Bank of Canada changes that payment by roughly $55 a month. Percentages are abstract until you turn them into dollars, so here is the math (FCAC).

Using the standard amortization formula on a $400,000 balance over a 25-year amortization:

| Rate | Monthly payment | vs 3.95% |

|---|---|---|

| 3.70% (after a 0.25-point cut) | ~$2,046 | -$54 |

| 3.95% (today's variable) | ~$2,100 | baseline |

| 4.20% (after a 0.25-point hike) | ~$2,156 | +$56 |

A single quarter-point decision at the Bank of Canada moves this payment by about $55 a month, or roughly $660 a year. Over a 5-year term, that is more than $3,000. This is why borrowers with variable mortgages watch the eight announcement dates so closely.

Now compare a credit card. Carrying a $5,000 balance at 20.99% costs about $1,050 a year in interest, and a Bank of Canada cut does nothing to lower it. The lesson: which product you borrow with matters more than where the policy rate sits. Moving a balance from a credit card to a HELOC or a personal loan can cut your interest cost by far more than any rate decision will.

When will interest rates in Canada change?

The Bank of Canada announces its rate decision on eight fixed dates each year, and the next one is July 15, 2026. As of June 2026, markets and forecasters expect the policy rate to stay near 2.25% through the rest of the year, with only a modest move likely into 2027 (Bank of Canada). That pause after two years of cuts is why interest rates in Canada are not currently going down.

What to watch between decisions:

- Inflation reports. If core inflation drifts back above the 2% target, the Bank is more likely to hold or hike. If it falls clearly below, cuts become more likely.

- Energy prices and trade. The June 2026 hold was driven partly by energy costs and US trade uncertainty. Both can push the next decision either way.

- Employment and growth. Weak jobs and slow growth give the Bank room to cut; a strong economy argues for holding.

No one can predict the exact path, and the Bank itself decides meeting by meeting. The practical takeaway is to plan around the rate you have, not the rate you hope for. If you carry a variable mortgage or a line of credit, build a buffer for a 0.50-point move in either direction so a single decision does not strain your budget.

At Sphera Credit, our focus is on helping lenders assess each borrower accurately and fairly, especially when a file does not fit a simple rate-sheet box. Understanding how the rate you are quoted is built, from the policy rate up through prime to your product, is the first step to borrowing on terms that fit your situation.