Which bank has the lowest interest rate on a personal loan in Canada?

No single bank always has the lowest personal loan rate in Canada, because the rate you are offered depends on your credit profile, not just the lender. Canada's big banks (RBC, TD, Scotiabank, BMO, and CIBC) post similar starting rates, and which one wins for you depends on your credit score, income, and whether the loan is secured. Credit unions frequently undercut all five.

The annual percentage rate (APR) is the yearly cost of borrowing, including interest and most mandatory fees. In April 2026, chartered banks charged a volume-weighted average of about 7.7% APR on new personal loans, according to the Bank of Canada. That is the average across all approved borrowers. The strongest applicants pay less, and higher-risk applicants pay much more.

Rather than ranking banks, it helps to compare lender types, because the lowest rate usually comes from a category of lender, not a specific brand:

| Lender type | Typical personal loan APR | Best for |

|---|---|---|

| Credit unions | ~6% - 12% | Members with good credit who want the lowest rate |

| Big Five banks | ~7% - 13% | Existing customers with steady income |

| Online and fintech lenders | ~10% - 30% | Fair credit, fast funding, fewer in-branch steps |

| Alternative and subprime lenders | ~20% - 35% | Bad credit or thin files, capped at the 35% legal maximum |

Rate bands move with the Bank of Canada policy rate and reset constantly, so treat these as a guide and confirm current numbers directly with each lender. When the central bank cuts its policy rate, variable personal loan rates tend to follow within weeks, while fixed rates on new loans drift down more slowly. This is why the "lowest rate" bank can change from one quarter to the next, and why a rate that looked best six months ago may no longer be competitive today.

Why "which bank has the lowest rate" is the wrong question

Asking which bank is cheapest assumes there is one right answer for everyone, but the lowest rate is borrower-specific, and three common traps cause shoppers to overpay. Reframing the question around your own profile saves more money than chasing a single advertised number.

- The advertised "from 6.99%" is a floor, not a typical rate. Lenders quote their best-case APR, which only borrowers with excellent credit and strong income actually receive. Most applicants are offered a higher rate, so the headline number is a starting point, not a promise.

- The lowest rate is not always the lowest cost. A loan with a slightly higher rate but no origination fee, no prepayment penalty, and no bundled loan insurance can cost less overall than a lower-rate loan loaded with extras. Always compare the total cost of borrowing over the full term.

- Shopping only the big banks skips the lenders that often win. Many borrowers compare the Big Five and stop there. Credit unions, which routinely price 1 to 2 points lower, never enter the comparison. That single omission can be the difference between the lowest rate and a middling one.

The practical takeaway: shop by your own credit tier across at least one credit union and one bank, and compare the total cost, not the advertised rate.

What a personal loan actually costs at each rate

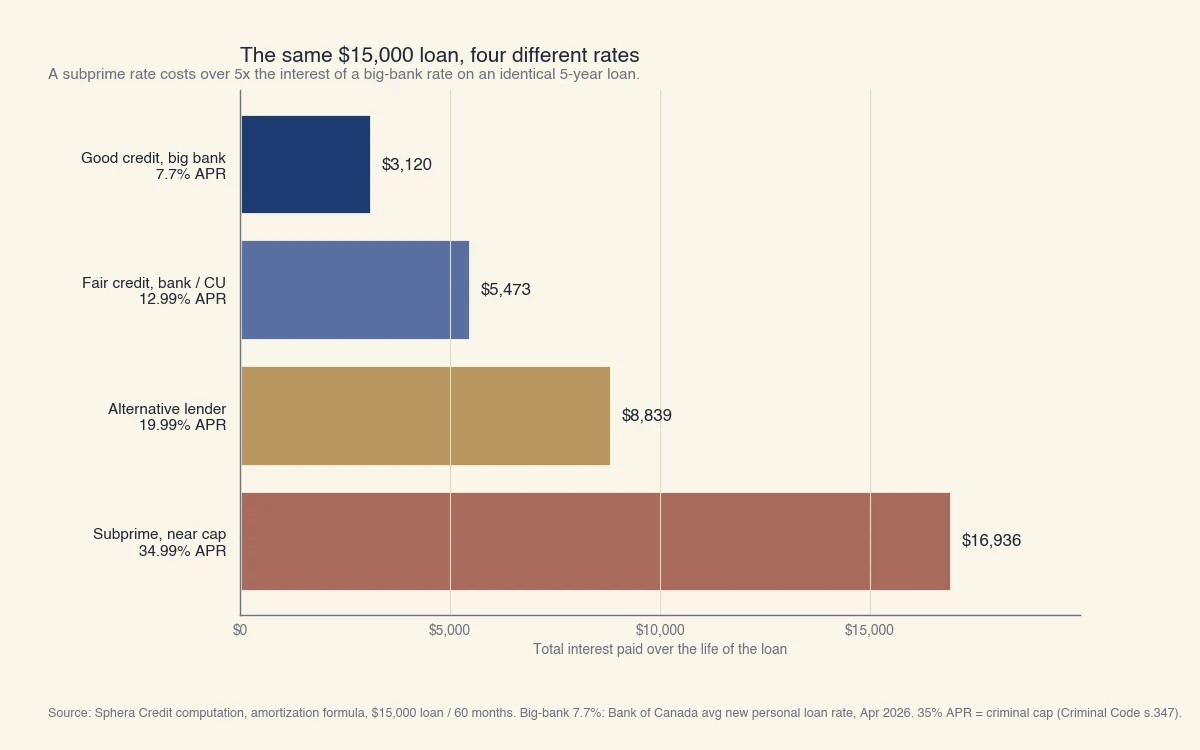

The rate you qualify for changes the cost of the same loan by thousands of dollars, so a small difference in APR is worth real effort to capture. The chart below runs an identical $15,000 personal loan over five years (60 months) at four representative Canadian rates, using the standard amortization formula.

Source: Sphera Credit computation using the standard amortization formula on a $15,000 personal loan over 60 months. Big-bank rate (7.7%): Bank of Canada average new personal loan plan rate, April 2026. The 35% APR ceiling is the criminal interest rate cap under Criminal Code section 347. Mid-tier rates are representative.

The same $15,000 loan produces very different bills:

| Rate (APR) | Monthly payment | Total interest over 5 years |

|---|---|---|

| 7.7% (good credit, big bank) | $302 | $3,120 |

| 12.99% (fair credit) | $341 | $5,473 |

| 19.99% (alternative lender) | $397 | $8,839 |

| 34.99% (subprime, near the cap) | $532 | $16,936 |

Moving from a subprime 34.99% rate to a big-bank 7.7% rate cuts the interest bill from $16,936 to $3,120 on the same loan. That is more than five times the cost for borrowing the identical amount. The lesson is that the rate you qualify for matters far more than the lender's brand, and that improving your credit before you apply can be worth thousands of dollars.

Even a smaller gap adds up. The same $15,000 loan at 7.7% costs about $870 less in interest than the same loan priced two points higher at 9.7%, which is roughly the saving you capture just by getting a quote from a credit union before you sign. Over the full five-year term, that is real money for the price of one extra phone call.

What determines the rate a bank offers you

Lenders price a personal loan on your risk, and your credit score is the single largest input, followed by income stability, the loan structure, and the legal rate ceiling. Understanding these inputs lets you predict your tier before you apply.

- Credit score. This is the strongest driver of your rate. Higher scores signal a lower chance of missed payments, so they earn lower rates.

- Income and debt-service ratios. Lenders check that your income comfortably covers the new payment alongside your existing debts. A lower debt-to-income ratio, the share of your monthly income that goes to debt payments, supports a better rate.

- Secured versus unsecured. A secured loan is backed by collateral such as a car or a savings deposit, which lowers the lender's risk and your rate. An unsecured loan has no collateral and prices higher.

- Fixed versus variable. A fixed rate stays the same for the whole term. A variable rate moves with the lender's prime rate, which itself tracks the Bank of Canada policy rate, so it can rise or fall during the loan.

Your score tier maps roughly to these rate bands at mainstream lenders:

| Credit score | Tier | Likely personal loan rate |

|---|---|---|

| 760+ | Excellent | Lowest advertised rates |

| 725 - 759 | Very good | Near-prime bank rates |

| 660 - 724 | Good | Standard bank rates |

| 560 - 659 | Fair | Higher bank tiers or fintech lenders |

| Below 560 | Poor | Alternative lenders, up to the 35% cap |

One ceiling applies to every lender. Since January 1, 2025, the criminal rate of interest under section 347 of the Criminal Code is 35% APR, down from the previous 60% effective annual rate. Any consumer lender charging more than 35% APR is committing an offence, so a legitimate Canadian personal loan never exceeds that rate.

How to get the lowest personal loan rate in Canada

You can lower the rate you are offered by improving your credit profile and by forcing lenders to compete for your business. The steps below have the largest effect, roughly in order of impact.

- Raise your credit score before you apply. Pay every bill on time, bring credit card balances below 30% of their limits, and avoid new credit applications in the months before you borrow. A move up one score tier can lower your rate by several points.

- Get quotes from at least one credit union and one bank. Credit unions often price below the big banks, and an existing bank may match a lower offer to keep your business. The Financial Consumer Agency of Canada recommends comparing the total cost of borrowing across lenders.

- Consider a secured loan or a co-signer. Pledging collateral or adding a creditworthy co-signer reduces the lender's risk and can drop your rate, especially if your own credit is fair or thin.

- Borrow only what you need over the shortest comfortable term. A shorter term means less total interest, even though the monthly payment is higher. Match the loan size to the actual expense.

- Watch the fees, not just the rate. Ask about origination fees, prepayment penalties, and optional loan insurance. A low rate wrapped in fees can cost more than a slightly higher rate with none.

If you fall outside a lender's standard credit box, the answer is not always a higher rate. Modern underwriting can assess repayment ability more accurately than a single score, which is the work Sphera Credit does for lenders: helping them say yes to good borrowers fairly, with an accurate read of risk rather than a blunt cutoff.