What happens to interest rates during a recession?

Interest rates usually fall during a recession, because the Bank of Canada lowers its policy interest rate to make borrowing cheaper and encourage spending when the economy is shrinking. As the policy rate drops, the prime rate at commercial banks follows, and so do the rates on variable mortgages, lines of credit, and many consumer loans (Bank of Canada).

An interest rate is the price of borrowing money, charged as a percentage of the amount borrowed per year. A recession is a significant, broad-based drop in economic activity that lasts more than a few months (Statistics Canada). When activity falls, the central bank's usual response is to cut rates so that credit gets cheaper and demand recovers.

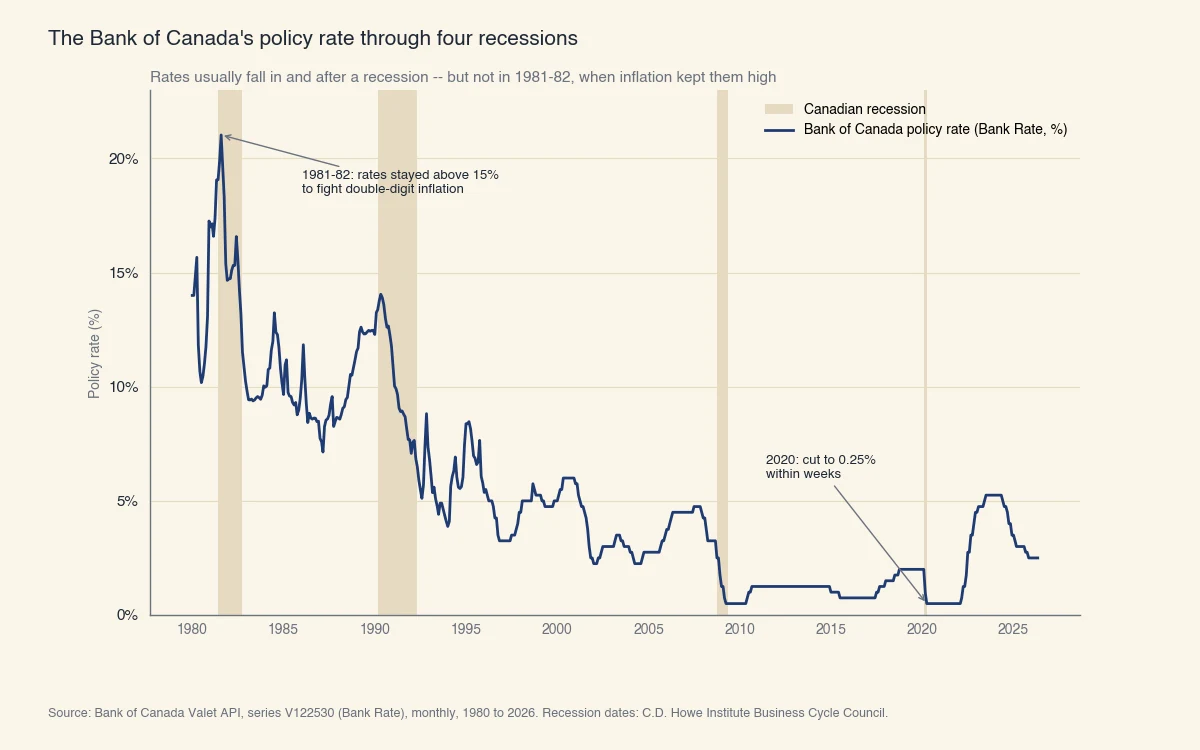

The historical record in Canada is clear. In the 2008-09 recession the Bank of Canada cut its policy rate to 0.5%, and in the 2020 recession it cut to 0.25% within weeks (Bank of Canada). The chart below shows the policy rate across the last four Canadian recessions.

Source: Bank of Canada Valet API, series V122530 (Bank Rate), monthly, 1980 to 2026. Recession dates: C.D. Howe Institute Business Cycle Council.

One important detail before going further: the rate the Bank of Canada controls is a short-term rate. It strongly influences variable borrowing costs and savings yields, but it does not directly set fixed mortgage rates. That distinction explains a lot of the confusion about recessions and rates, and the rest of this page works through it.

Why does the Bank of Canada lower interest rates in a recession?

The Bank of Canada lowers rates in a recession to defend two goals at once: keeping inflation near its 2% target and supporting employment and output when demand collapses. Cutting the cost of borrowing is the main tool it has to pull a weak economy back toward normal (Bank of Canada).

The mechanism runs through a chain of rates:

- The policy interest rate (also called the target for the overnight rate) is the rate the Bank of Canada sets. It is the rate major financial institutions charge each other for one-day loans (Bank of Canada).

- The prime rate is the rate commercial banks charge their best customers. It moves almost in lockstep with the policy rate, usually sitting about 2.2 percentage points above it.

- Variable consumer rates (variable mortgages, home equity lines of credit, many personal lines) are quoted as "prime plus or minus" a margin, so they move whenever prime moves.

When the Bank of Canada cuts the policy rate by, say, half a percentage point, the prime rate typically drops by the same amount within days, and every variable-rate borrower tied to prime sees their interest cost fall. That is the channel that makes credit cheaper in a downturn.

What a rate cut is trying to do

A recession is, at its core, a shortfall in spending. Households worried about their jobs cut back, businesses delay investment, and the drop in demand feeds on itself. Lower interest rates counter this by making it cheaper to borrow and less rewarding to save, which nudges money back into spending and investment. The Bank of Canada describes this as supporting demand so the economy returns to full capacity and inflation stays near target (Bank of Canada). Cutting rates to revive demand is also why lower interest rates can stoke inflation once spending recovers too far.

This is also why savings yields fall in a recession. The same cut that lowers your borrowing cost lowers the interest banks pay on savings accounts and guaranteed investment certificates (GICs). Cheaper credit and lower deposit yields are two sides of the same policy.

Do interest rates always go down in a recession?

No. Interest rates usually fall in a recession, but not always: when a downturn arrives alongside high inflation, the central bank may hold rates high or even raise them to bring prices under control. The rule "rates fall in a recession" is a strong tendency, not a law.

Canada's own history proves the point. The 1981-82 recession was one of the deepest of the postwar era, yet the Bank Rate stayed above 15% through most of it and peaked above 21% in August 1981 (Bank of Canada). Inflation was running in double digits, and the central bank judged that taming prices had to come first, even at the cost of a severe recession. You can see this clearly in the chart above: the 1981-82 recession band sits at the very top of the rate range, while the 1990-91, 2008-09, and 2020 bands all show rates falling.

The lesson is that what happens to rates depends on why the recession is happening:

- A demand-driven recession (spending collapses, inflation is low or falling) usually brings rate cuts. The 2008-09 and 2020 recessions fit this pattern.

- A supply-driven or inflationary recession (a stagflation, where prices rise even as output falls) can keep rates high. The early 1980s fit this pattern.

Why your fixed mortgage rate may not drop when the Bank of Canada cuts

Even when the Bank of Canada cuts its policy rate, fixed mortgage rates may not fall, because fixed rates track Government of Canada bond yields rather than the overnight rate. Bond yields reflect what investors expect for inflation and growth over several years, so they can move in a different direction from the short-term policy rate.

This catches many borrowers off guard. A variable-rate mortgage is tied to the prime rate, so a policy-rate cut feeds through quickly. A five-year fixed mortgage is priced off the five-year Government of Canada bond yield, which may already have moved before the Bank of Canada acts, or may not move at all. So in a recession you can see variable rates falling while fixed rates barely budge. If you are deciding between fixed and variable, this difference matters more than the headline policy rate (FCAC).

What a recession means for your borrowing and savings

For most Canadians, a recession-driven rate cut means cheaper variable borrowing and lower savings yields, but the effect depends on which side of the ledger you are on and what kind of credit you hold. The table below summarizes the typical outcomes.

| If you are... | What a recession-driven rate cut usually means |

|---|---|

| A variable-rate mortgage or line-of-credit holder | Your interest rate and payment usually fall soon after the Bank of Canada cuts, since these rates track the prime rate. |

| A fixed-rate mortgage holder up for renewal | You may renew at a lower rate, but only if bond yields have fallen, not just the policy rate. Check current fixed rates, not the headline cut. |

| A saver (savings account or GIC) | Expect lower yields. Deposit and GIC rates usually fall quickly when the policy rate drops. |

| A new borrower (car loan, personal loan) | Borrowing is cheaper, but lenders often tighten approval standards because default risk rises when jobs are less secure. |

A few practical points follow from this:

- A lower rate is not the same as easy approval. In a recession, lenders see higher default risk and often raise their credit standards. Cheaper money on paper does not help if you cannot qualify. This is exactly where applicants who fall just outside a lender's standard criteria get declined, and where careful, accurate assessment of a borrower's real situation matters most.

- Variable beats fixed only if rates keep falling. A variable rate saves money while the Bank of Canada is cutting, but exposes you to rate hikes on your mortgage when the cycle turns. Match the choice to your tolerance for payment changes, not just to today's recession.

- Locking a GIC early can protect yield. If you expect a rate-cutting cycle, locking in a longer GIC before the cuts can preserve a higher yield, since new GICs will pay less after each cut.

As of mid-2026, the Bank of Canada has held its policy interest rate at 2.25% for several consecutive meetings, down from the 5% peak it reached in 2023-2024 to fight post-pandemic inflation. Because the policy rate only moves on the Bank of Canada's scheduled rate-decision dates, always confirm the current figure on its policy interest rate page (Bank of Canada).

The bottom line: in most recessions, interest rates fall because the Bank of Canada cuts to revive spending, and variable borrowers and savers feel it first. But the rule breaks when inflation is the bigger problem, and fixed mortgage rates follow bond markets, not the central bank. Knowing which forces are at work is what lets you read a recession correctly instead of assuming every downturn means cheaper credit.