How do you calculate the interest rate per month?

To calculate the interest rate per month, divide the annual interest rate by 12 and convert it to a decimal: a 9% annual rate becomes 0.09 ÷ 12 = 0.0075, which is 0.75% per month. This monthly figure is the periodic rate, the rate a lender actually applies to your balance during one billing cycle.

The steps are short:

- Start with the annual rate. This is the plain interest rate on your loan agreement, not the APR. The APR is the interest rate plus lender fees, so it runs higher than the rate charged on your balance (CFPB).

- Convert the percentage to a decimal. Move the decimal point two places left: 9% becomes 0.09.

- Divide by the number of payments per year. For monthly payments, divide by 12. So 0.09 ÷ 12 = 0.0075.

- Read it back as a percentage if you want. 0.0075 is 0.75% per month.

That single number is all you need to find the interest charged in any given month. The next section turns the rate into dollars.

How do you calculate the interest rate per year from a monthly rate?

To go the other direction, multiply the monthly rate by 12: a 0.75% monthly rate is a 9% nominal annual rate. This works for the quoted, nominal rate. It does not capture compounding, which is covered further down. If you only know the dollar interest and the balance, you can also back into the rate: divide one month's interest by the balance, then multiply by 12. On a $10,000 balance charged $75 in a month, that is ($75 ÷ $10,000) × 12 = 0.09, or 9% per year. This reverse check is useful when a statement shows a finance charge but not the rate.

How do you calculate the interest you owe in a single month?

Multiply your current balance by the monthly periodic rate. A $10,000 balance at a 9% annual rate carries $10,000 × 0.0075 = $75 of interest in that month. The dollar figure changes every month on most loans because the rate is applied to whatever balance is left.

How that plays out depends on whether the loan uses simple interest or amortizes.

Simple interest is charged only on the original principal and does not compound. The formula is I = P × r × t, where P is the principal, r is the annual rate as a decimal, and t is the time in years. For one month, set t to 1/12:

- $5,000 balance at 8% for one month: $5,000 × 0.08 × (1/12) = $33.33.

Amortized interest is the common case for personal loans, auto loans, and mortgages. Each fixed payment is split between interest and principal, and the split shifts over the term. Take a $10,000 loan at 9% over 5 years, where the fixed monthly payment works out to $207.58:

| Month | Starting balance | Interest (balance × 0.0075) | Principal paid | Ending balance |

|---|---|---|---|---|

| 1 | $10,000.00 | $75.00 | $132.58 | $9,867.42 |

| 2 | $9,867.42 | $74.01 | $133.57 | $9,733.85 |

| 3 | $9,733.85 | $73.00 | $134.58 | $9,599.27 |

Early payments are heavy on interest because the balance is high. As the balance falls, the interest portion shrinks and more of each payment retires principal. This is why paying extra early in a loan saves the most.

To find the fixed payment yourself, use the standard amortization formula: payment = P × r ÷ (1 − (1 + r)^−n), where P is the loan amount, r is the monthly periodic rate, and n is the total number of payments. For the $10,000 loan at 0.75% per month over 60 months, that is $10,000 × 0.0075 ÷ (1 − 1.0075^−60) = $207.58. Once you have the payment, each month's interest is just the balance times the monthly rate, and the rest reduces principal. Repeating those two steps row by row builds the full schedule above.

Why your monthly rate is not just the annual rate divided by 12

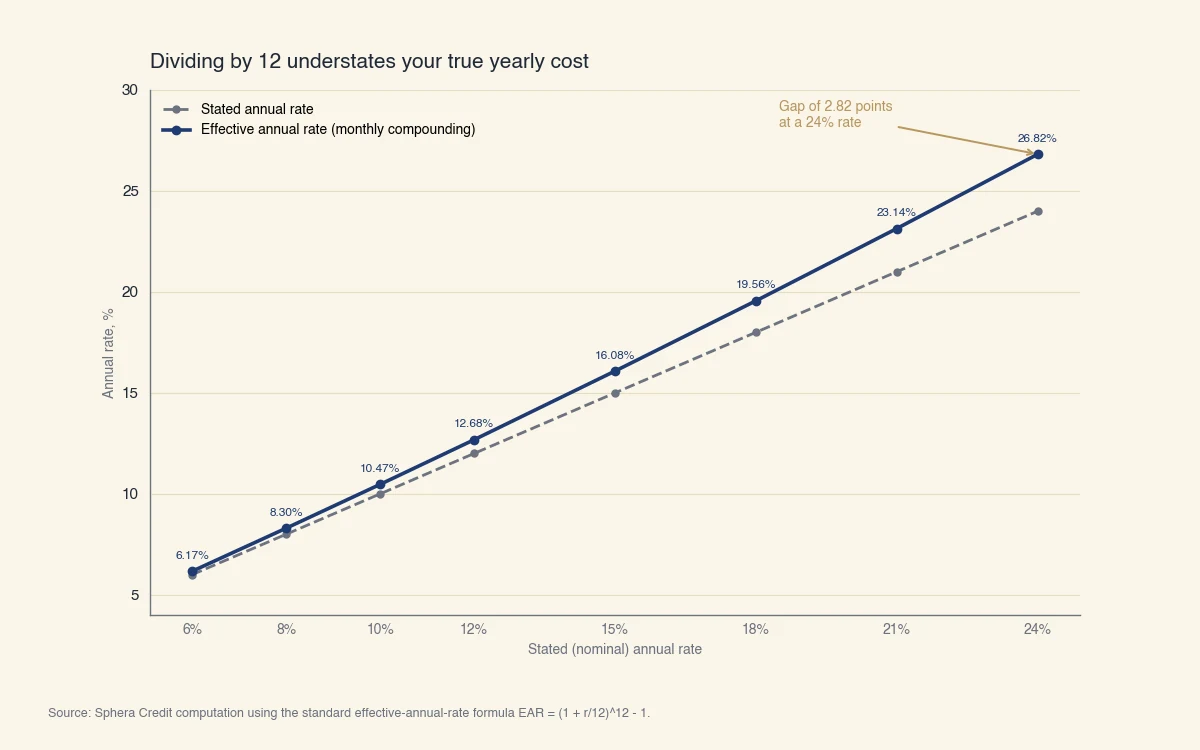

Dividing the annual rate by 12 gives the nominal monthly rate, but it understates your true yearly cost, because monthly compounding charges interest on interest. A 12% nominal rate compounded monthly costs 12.68% over a full year, not 12%. Almost every loan-interest guide skips this distinction, yet it is the heart of "how much does my rate really cost."

Three terms separate cleanly once you see the math:

- Nominal annual rate is the quoted rate, for example 12%.

- Periodic (monthly) rate is the nominal rate ÷ 12, here 1% per month.

- Effective annual rate (EAR), disclosed as APY on deposit products, is what you actually pay or earn once compounding is counted.

The conversion is one formula: EAR = (1 + periodic rate)^number of periods − 1. For a 12% nominal rate:

- (1 + 0.01)^12 − 1 = 1.1268 − 1 = 0.1268, or 12.68%.

The gap widens as the rate climbs, which matters most on high-rate balances like credit cards.

Source: Sphera Credit computation using the standard effective-annual-rate formula EAR = (1 + r/12)^12 − 1.

This is also why the APR and the monthly rate are not interchangeable. The APR folds in fees, so dividing the APR by 12 mixes fee cost into what looks like pure interest. Regulation Z sets the legal method for determining the APR precisely so borrowers can compare offers on one number (CFPB, 12 CFR 1026.22). When you compute the interest on a balance, use the stated interest rate. When you compare two loan offers, use the APR. The federal Truth in Savings standard applies the same logic in reverse for savings, requiring banks to quote APY so compounding is reflected (CFPB, Regulation DD Appendix A).

Should you divide the annual rate by 12 or by 365?

Divide by 12 when interest is charged monthly on the balance, and divide by 365 when interest accrues daily. The right divisor depends on the product, not on personal preference. This is the question the rest of the web answers inconsistently, with some guides using 12 and others using 365 without saying why.

The accrual method, set by the loan type, decides the divisor:

| Loan type | How interest accrues | Divisor for the periodic rate |

|---|---|---|

| Most personal and auto loans | Monthly, on the remaining balance | Annual rate ÷ 12 |

| US mortgages | Monthly, on the remaining balance | Annual rate ÷ 12 |

| Credit cards | Daily, compounded on the balance | APR ÷ 365 |

| Federal student loans | Simple daily accrual | Rate ÷ 365 |

For a credit card, the daily method matters. A 24% APR card has a daily periodic rate of 0.24 ÷ 365 = 0.000657. On a $2,000 balance carried for a 30-day cycle, daily compounding produces about $39.78 in interest, while a flat "divide by 12" estimate suggests $40.00. The two are close here, but they drift apart as the cycle length and the balance change day to day, which is exactly why issuers compute interest on a daily periodic rate. Card issuers must disclose the APR under federal rules, and the CFPB notes the APR runs higher than the plain rate when fees apply (CFPB).

For a standard installment loan, the monthly method is correct, and dividing by 365 would understate each month's charge.

What changes how much monthly interest you actually pay?

Your monthly interest in dollars moves with three things: the rate, the balance, and how often interest compounds. Two of those are partly in your control.

- The rate is set at origination and tracks the wider rate environment. The Federal Reserve publishes average rates on consumer loans in its G.19 release, a useful benchmark for judging whether an offer is competitive (Federal Reserve G.19).

- The balance falls fastest when you pay more than the minimum. Because interest each month is the rate times the balance, a smaller balance means less interest, which is why extra principal payments compound in your favor.

- Compounding frequency decides how far the effective rate sits above the nominal rate. Monthly compounding on an installment loan is mild; daily compounding on a revolving card balance is not.

At Sphera Credit, our work centers on reading a borrower's full financial picture accurately, including how their existing debt is priced, so that credit decisions rest on the real cost of borrowing rather than a single headline rate.