Can you get a mortgage with an R7 credit rating?

Yes, you can get a mortgage with an R7 credit rating in Canada, but rarely from a major bank. Approval usually comes from a B-lender, a credit union, or a private lender, at a higher interest rate and with a larger down payment. An R7 is a credit-report code that means you settled a debt through a consumer proposal, a debt management plan, or a similar arrangement instead of paying it in full as originally agreed (Equifax Canada).

An R7 tells a lender that you had serious repayment trouble in the recent past. That raises your risk profile, but it does not erase your ability to borrow. What changes is where you can borrow and what it costs.

The short version: prime banks want clean recent credit, so an active R7 almost always pushes you to alternative lenders who price the risk rather than refuse it. The rest of this page shows the R-rating scale, how the three tiers of Canadian mortgage lenders treat an R7, what the higher rate actually costs in dollars, and whether you need to wait for the rating to age off your report.

What is an R7 credit rating, and how long does it last?

An R7 sits near the bottom of Canada's R1 to R9 credit-rating scale, where R1 means you pay on time and R9 means the debt went to collections or bankruptcy. The "R" stands for revolving credit, and the number describes how the account was repaid (TransUnion Canada). Other prefixes exist for other credit types, such as "M" for mortgages and "I" for installment loans, but the number scale is the same.

| Rating | What it means |

|---|---|

| R0 | Account approved but not yet used |

| R1 | Paid on time, within 30 days of billing |

| R2 | Paid 31 to 59 days late |

| R3 | Paid 60 to 89 days late |

| R4 | Paid 90 to 119 days late |

| R5 | Paid 120 days or more late, not yet a write-off |

| R7 | Debt settled through a consumer proposal, debt management plan, or consolidation order |

| R8 | Repossession or surrender of secured property |

| R9 | Bad debt, sent to collections, or bankruptcy |

An R7 most often comes from a consumer proposal, a legal agreement filed through a Licensed Insolvency Trustee where you repay part of what you owe over a set period. Once the arrangement appears, it does not stay forever. At TransUnion, an R7 from a consumer proposal generally drops off three years after you complete it, or six years from the filing date, whichever comes first. Equifax Canada applies a similar rule. The exact timing depends on the bureau and the arrangement, so check both reports directly through the Financial Consumer Agency of Canada guidance on credit reports.

How does an R7 affect mortgage approval?

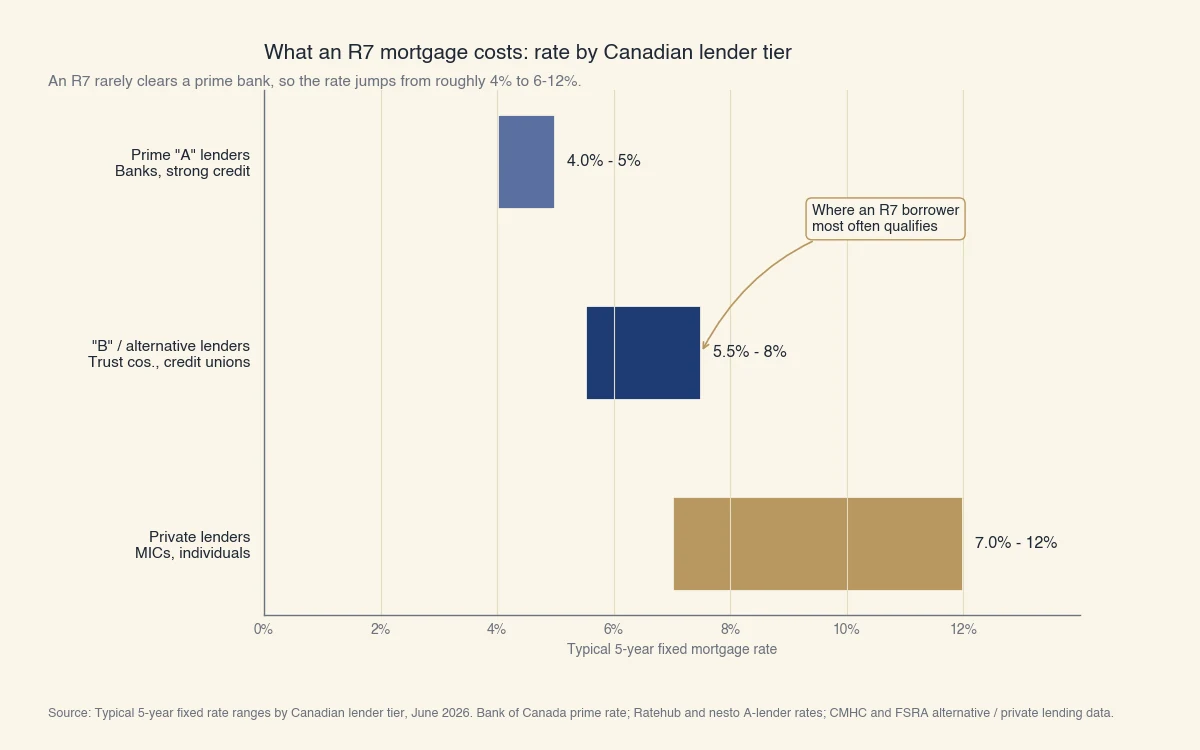

An R7 affects approval by pushing your file down a three-tier lender ladder: prime "A" lenders usually decline, "B" or alternative lenders and credit unions price the risk, and private lenders backstop the rest. Understanding the ladder is the difference between thinking a mortgage is impossible and knowing exactly who to ask.

- Prime "A" lenders are the big banks and large credit unions. They offer the lowest rates because they fund insured and low-risk mortgages. Default insurance from CMHC, Sagen, or Canada Guaranty generally requires clean recent credit, so an active R7 normally fails the insurer's test, and the bank declines a high-ratio file (CMHC).

- "B" or alternative lenders include trust companies and many credit unions. They are not bound to insure every mortgage, so they can approve an R7 borrower by charging a higher rate and requiring more equity. This is where most R7 borrowers land.

- Private lenders are mortgage investment corporations (MICs) and individual investors. They lend mostly on the value of the property, accept the weakest credit, and charge the highest rates and fees.

Two rules shape every tier. First, federally regulated lenders must apply the mortgage stress test, qualifying you at the higher of your contract rate plus 2% or 5.25%, under OSFI Guideline B-20. Second, your loan-to-value ratio (LTV), the size of the loan against the home's value, drives how much risk the lender takes. A bigger down payment lowers the LTV and is the most direct way an R7 borrower offsets the rating.

How much more does an R7 mortgage cost?

An R7 mortgage costs more because you move from a prime rate near 4.5% to an alternative rate of roughly 6.5%, or a private rate of 7% to 12%. On a $400,000 mortgage, that gap adds hundreds of dollars a month. No general advice page tells you the dollar figure, so here is a concrete Canadian example.

Take a $500,000 home with 20% down, leaving a $400,000 mortgage over a 25-year amortization. Using the standard Canadian semi-annual-compounding formula, the monthly payment lands at:

- Prime "A" lender at 4.5%: about $2,214 a month

- "B" or alternative lender at 6.5%: about $2,679 a month

- Private lender at 10%: about $3,578 a month

Source: Typical 5-year fixed rate ranges by Canadian lender tier, June 2026. Bank of Canada prime rate; Ratehub and nesto A-lender rates; CMHC Residential Mortgage Industry Report and FSRA alternative and private lending data. Ranges are typical, not quotes.

The B-lender pays about $465 more a month than the prime borrower, roughly $5,600 a year, or close to $28,000 over a five-year term. The private-lender path adds more than $1,300 a month. The prime rate tracks the Bank of Canada's policy decisions, which set the prime rate at 4.45% as of June 2026 (Bank of Canada). These rates are typical ranges, not quotes, and your own offer depends on your down payment, income, and the lender.

Do you have to wait for the R7 to fall off your report?

No. You do not have to wait the full three to six years for the R7 to disappear before you can finance a home. This is the most common misunderstanding, and it costs people years of waiting they did not need. B-lenders and many credit unions underwrite current R7 files every day.

What these lenders actually weigh:

- Time since the event. The further you are past the consumer proposal or settlement, the better. Even one year of clean history after the fact shifts the file.

- Fresh on-time payments. New tradelines repaid on time, such as a secured credit card, show the rating reflects the past, not the present.

- Down payment and provable income. Strong equity and steady income do more to win approval than waiting for the code to age off.

In other words, an R7 describes where you were, and a lender who specializes in these files cares more about where you are heading. This is precisely the situation where a borrower falls outside the standard credit box yet is a sound risk on the full picture, and where a careful, accurate assessment matters more than a single code.

How do you improve your odds of mortgage approval with an R7?

You improve your odds by lowering the lender's risk: a larger down payment, a co-signer, provable income, and a few months of fresh on-time payments do the most work. Each one gives an alternative lender a reason to say yes at a better rate.

- Save a larger down payment. Aim for at least 20%, and ideally 35%, to cut the loan-to-value ratio and reach more lenders.

- Add a co-signer or guarantor. A co-signer with strong credit shares responsibility for the mortgage and reduces the lender's risk.

- Document stable income. Two years of consistent income, low other debts, and a healthy debt-to-income ratio reassure an underwriter that the R7 was a one-time setback.

- Rebuild before you apply. A secured credit card or a small installment loan, paid on time, builds a fresh layer of R1 history over the old R7.

- Use a mortgage broker who knows B-lenders. Brokers place files with alternative and private lenders that do not deal with the public directly.

An R7 narrows your options, but it does not close the door. With the right lender tier, a solid down payment, and a few months of clean payments, a mortgage is well within reach.