What is the average credit score in Canada?

The average credit score in Canada is 679 according to Borrowell's 2026 data from more than four million members, while FICO reports a national average of 760 as of November 2024. Both numbers are correct. They simply measure different groups of Canadians using different scoring models (Borrowell, FICO).

Canadian credit scores run on a 300 to 900 scale at both Equifax and TransUnion, the country's two credit bureaus, so the highest credit score you can reach in Canada is 900. A higher number signals to lenders that you are more likely to repay borrowed money on time (Equifax Canada).

Here is how the two published averages compare and what each one actually measures:

| Source | Average score | Population measured | As of |

|---|---|---|---|

| Borrowell | 679 | 4M+ Borrowell members (Equifax Risk Score) | 2026 |

| FICO | 760 | Full file of scored Canadian consumers | November 2024 |

The score bands lenders use are the same regardless of which average you compare against:

| Range | Label | What it means for borrowing |

|---|---|---|

| 760 - 900 | Excellent | Best rates and straightforward approval |

| 725 - 759 | Very good | Most prime products available |

| 660 - 724 | Good | Mainstream qualification range |

| 560 - 659 | Fair | Limited prime options; alternative lenders likely |

| 300 - 559 | Poor | Secured or subprime products only |

Why is the average credit score higher than a good one?

The "average" Canadian credit score lands in the excellent band (FICO 760) or comfortably inside good (Borrowell 679), which surprises people because both sit above the 660 mark that lenders treat as the floor for good credit. The gap is not a contradiction. It comes from two things: which population you measure, and the fact that scored Canadians cluster toward the high end.

FICO's 760 is the mean of the entire file of scored Canadian consumers. That file is dominated by people with long, clean repayment histories, because the longer you hold credit and pay on time, the higher you climb. Borrowell's 679 is the average of Canadians who actively sign up for free credit monitoring, a younger and more credit-curious group that naturally scores lower. Neither number is wrong. They answer different questions.

This matters for one practical reason: being below the average does not mean you have bad credit. If your score is 700, you are below FICO's 760 national mean but still above the Borrowell average, above the 660 good threshold, and eligible for prime mortgages and credit cards. Most Canadians read "below average" as a problem when it is often a perfectly healthy score.

The split between 679 and 760 also explains why people compare scores and feel confused. Your bank may quote one number, a free app another, and a lender a third. Each uses a different model and pulls on a different day. The takeaway is to track your own trend over time rather than chasing a single national figure, and to know why a score suddenly drops when it does.

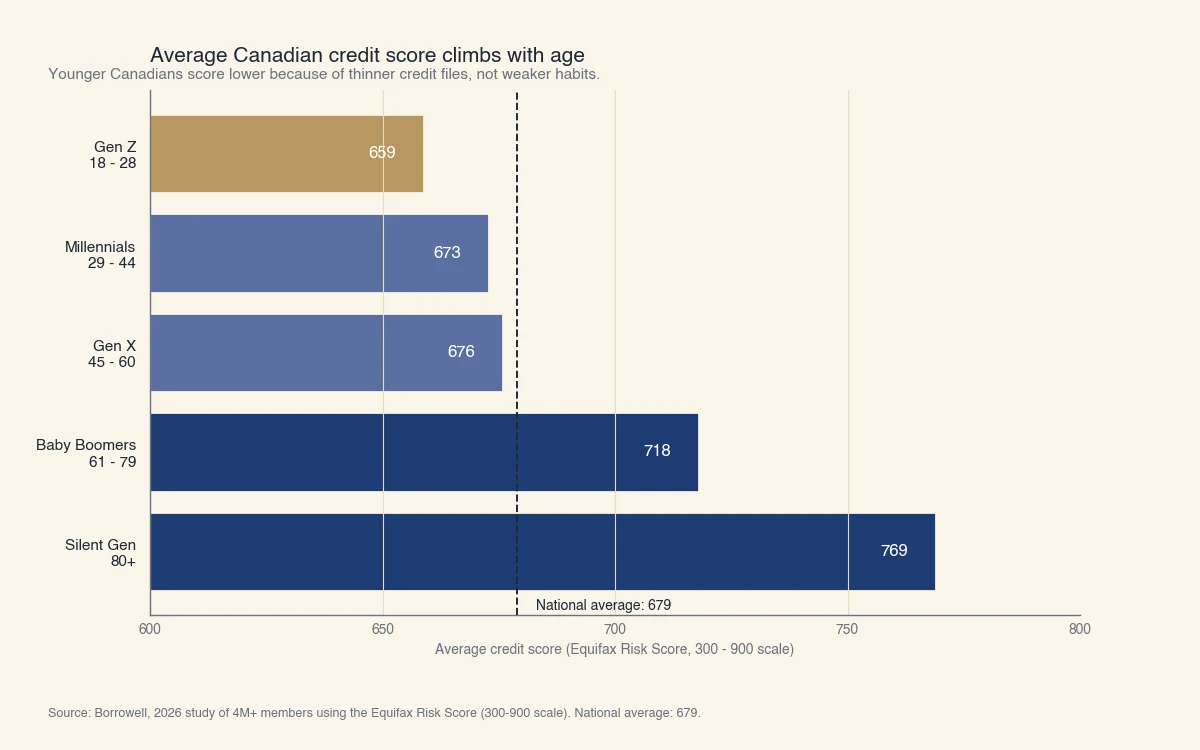

What is the average credit score by age in Canada?

Average credit scores rise steadily with age, from 659 for Gen Z (18 to 28) to 769 for the Silent Generation (80+), because length of credit history is one of the largest factors in any score. Older Canadians have simply had more years to build a track record (Borrowell).

Source: Borrowell, 2026 study of 4M+ members using the Equifax Risk Score. Generational averages on the 300 to 900 scale.

The pattern is consistent across every Canadian dataset: younger borrowers score lower not because they manage money poorly, but because they have thinner files. A 24-year-old with two years of credit history cannot yet score like a 65-year-old with three decades of on-time payments, no matter how responsible both are.

That said, age is not destiny. The single fastest lever at any age is credit utilization, the share of your available credit you actually use. Keeping balances under 30% of your limits, and ideally under 10%, can move a score within one or two billing cycles, far faster than waiting for your history to age.

Newcomers to Canada are the clearest example of why a low number is not the same as bad credit. Someone who arrives with a strong financial record abroad still starts with a thin or empty Canadian file, because credit history rarely transfers across borders. Their first Canadian score can sit well below the Gen Z average for a year or two, then climb quickly once a secured card or small installment loan establishes a domestic track record. The same logic applies to any borrower rebuilding after a setback: the score reflects the length and recency of your Canadian credit data, not your character or your income.

What is the average credit score by city in Canada?

Among major Canadian cities, Quebec City posts the highest average credit score at 723, followed by Montreal at 716 and Markham at 714, while scores cluster tightly across the country. Borrowell's 2026 data shows most large cities falling within a roughly 20-point band rather than the wide gaps people expect (Borrowell).

| City | Average credit score |

|---|---|

| Quebec City, QC | 723 |

| Montreal, QC | 716 |

| Markham, ON | 714 |

| Vancouver, BC | 704 |

| Laval, QC | 704 |

The bureaus do not publish a clean province-by-province average every quarter, and city-level figures shift with the sample, so treat these as directional rather than precise. The useful signal is the spread: a strong score in one city is a strong score everywhere, because lenders apply the same national bands no matter where you live.

What does an average credit score actually get you in Canada?

An average Canadian score of 679 or 760 both clear the prime lending threshold, so the real cost difference is not between those two numbers but between any prime score and a subprime one. In Canada, mortgage pricing barely changes once you are above roughly 660. The expensive cliff is the drop from prime lenders to alternative or B-lenders, which serve borrowers with fair or poor credit at materially higher rates.

Consider a $500,000 mortgage on a 25-year amortization. The numbers below use illustrative rates anchored to mid-2026 levels: a discounted prime rate near 4.5% versus an alternative-lender rate near 8.5% (Bank of Canada).

| Borrower profile | Illustrative rate | Monthly payment | Total interest over 25 years |

|---|---|---|---|

| Prime (score 660+, includes 679 and 760 averages) | 4.5% | ~$2,770 | ~$330,000 |

| Alternative lender (score ~600) | 8.5% | ~$3,975 | ~$693,000 |

The difference is about $1,200 more per month and roughly $363,000 in extra interest over the life of the mortgage. This is the practical lesson hidden inside the average-score question: improving from 679 to 760 changes very little on a Canadian mortgage, but crossing from a fair score into the good range, above 660, can change everything. (Rates are illustrative for comparison only; actual offers depend on the lender, the product, and the rate environment at the time.)

How do you check your score against the average?

You can check your own credit score for free through Borrowell, Equifax, or TransUnion, and doing so is a soft inquiry that never lowers your score. Once you know your number, compare it to the 660 good threshold first, then to the averages, in that order (FCAC).

A few things to keep in mind when you compare:

- Your Equifax and TransUnion scores will differ. Each bureau holds slightly different data and updates on its own schedule, so a 20-point gap between them is normal (TransUnion Canada).

- Free monitoring apps may show a different number than a lender. Apps often display an educational score, while lenders may pull a FICO or a bureau risk score. Use the app to track your trend, not to predict an exact lender decision.

- Checking your own score is always a soft pull. Only applications you submit to a lender create hard inquiries, and those cost a few points temporarily (FCAC).

The most useful comparison is not against the national average at all. It is against the threshold your next goal requires: 660 for most mainstream credit, 680 and up for the smoothest mortgage approval. If a home is the goal, the credit rating you need for a mortgage breaks those thresholds down by lender tier. Hitting those gates matters far more than matching a 760 mean.