Does applying for a credit card affect your credit rating?

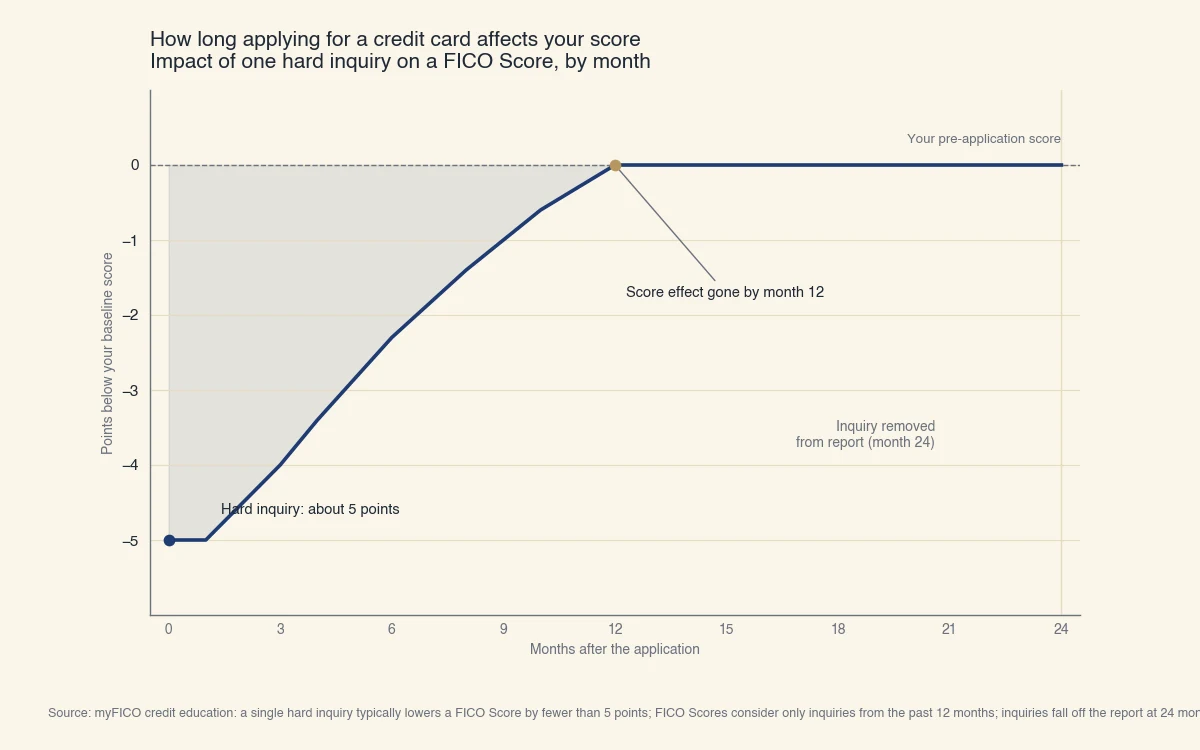

Yes, applying for a credit card affects your credit rating, but only slightly and only for a short time. The application triggers a hard inquiry that typically lowers your score by fewer than five points, and the effect fades within about a year. A hard inquiry is a record that a lender checked your credit because you applied for new credit (myFICO).

Most US readers use "credit rating" and "credit score" to mean the same thing: the three-digit number, usually a FICO Score or VantageScore on a 300 to 850 scale, that lenders use to predict whether you will repay. Applying for a card touches that number through one factor, new credit, which makes up only 10% of a FICO Score (myFICO). That is why the impact is small by design.

The confusion most people have is between the two kinds of credit check. The distinction decides whether your score moves at all.

| Soft inquiry | Hard inquiry | |

|---|---|---|

| What triggers it | Checking your own score, pre-approval offers, employer or insurer checks | A formal application for a card, loan, or line of credit |

| Affects your score | No | Yes, usually fewer than 5 points |

| Visible to lenders | No | Yes |

| Stays on your report | Up to 24 months | 24 months |

| Affects score for | Never | About 12 months |

The takeaway: shopping with a pre-approval tool, or checking your own credit, is a soft inquiry and never moves your score. Only submitting a real application creates the hard inquiry that does (myFICO).

How much does applying for a credit card lower your score, and how long does it last?

A single credit card application usually costs fewer than five points, and FICO returns all of those points within 12 months even though the inquiry stays visible on your report for 24. FICO Scores only count inquiries from the previous 12 months, so the score effect expires a full year before the inquiry itself disappears (myFICO).

Source: myFICO credit education. A single hard inquiry typically lowers a FICO Score by fewer than 5 points; FICO Scores consider only inquiries from the past 12 months; inquiries fall off the report at 24 months.

Here is the part competitor pages skip: the new card often helps your score more than the inquiry hurts it, once the math plays out.

Worked example. Say you have a 720 score and one card with a $4,000 limit carrying a $1,400 balance. Your utilization is 35% ($1,400 of $4,000), which is high enough to weigh on your score because credit utilization (the share of your available credit you are using) is 30% of a FICO Score.

- You apply for a second card with a $6,000 limit. The hard inquiry costs you roughly 3 to 5 points.

- Once the new card reports, your total available credit rises from $4,000 to $10,000. The same $1,400 balance is now 14% utilization instead of 35%.

- That utilization drop can add more points than the inquiry removed, because utilization carries three times the weight of new credit in the FICO model.

Net result: a small dip on application day, then a likely gain once the lower utilization reports, and full recovery of the inquiry points by month 12. The catch is the word "say." This only works if you do not run a balance up on the new card, which is the next section's warning. If you need the points sooner, how to boost your credit rating fast covers the levers that move a score in weeks rather than months.

If your score is already dropping for other reasons, the inquiry is rarely the culprit. See why is my credit score going down for the factors that move scores far more than an application does.

Does applying for loans, bank loans, or an overdraft affect your credit rating?

Yes. Any formal application for a personal loan, bank loan, or overdraft line of credit triggers a hard inquiry, exactly like a credit card, and lowers your score by a few points. The important difference is that loan inquiries can be bundled, while credit card inquiries cannot. This is the single most useful rule most pages on this topic leave out.

When you shop for one auto loan, mortgage, or student loan and apply to several lenders, the scoring models treat those multiple inquiries as a single event, because you are clearly seeking one loan, not five new debts. This is called rate-shopping or de-duplication:

- FICO collapses same-type loan inquiries inside a 45-day window in current score versions (14 days in older versions) into one inquiry (myFICO).

- VantageScore uses a rolling 14-day window for the same purpose (VantageScore).

- The federal Consumer Financial Protection Bureau confirms that shopping for a mortgage within a focused window counts as one inquiry, so comparing lenders does not stack penalties (CFPB).

Credit cards are the exception. Card applications are not bundled, so two card applications in the same week are two separate hard inquiries. That is why rate shopping for a mortgage is safe, but collecting sign-up bonuses across several cards in a short span adds up.

An overdraft line of credit behaves like any other credit account. Applying for it is a hard inquiry; using an overdraft you already have is not. Missed overdraft repayments, however, can be reported as late payments, which hurt far more than the original inquiry.

Does closing, canceling, or losing a credit card affect your credit rating?

Losing a card and getting a replacement does nothing to your score, but closing or canceling a card can quietly hurt it. This is the opposite of what most people assume. A common belief is that closing an old or unused card "cleans up" your credit. In practice it usually does the reverse.

Three different events, three different outcomes:

- Losing a card (replaced): No effect. Reporting a card lost or stolen keeps the same account open with the same number internally, so there is no new inquiry and no change to your history.

- Closing or canceling a card: Potentially negative. The card's limit disappears from your total available credit, so your utilization jumps even if your balances do not change. Over years, closing your oldest card can also shorten your average account age, the length-of-history factor worth 15% of a FICO Score.

- A card you keep but stop using: Safest. The limit stays in your utilization math and the account keeps aging, so your score benefits from leaving it open with a zero balance.

Reverse the earlier worked example to see the closing trap. If you close that $6,000 card and still owe $1,400 on the remaining $4,000 card, your utilization snaps back from 14% to 35%, which can cost more points than any single inquiry ever did. The card you opened helped you; closing it later is what does the damage.

For the broader playbook on raising a score rather than protecting it, see how to boost your credit score.

How to apply for credit without hurting your credit rating

Space out applications, use soft-inquiry pre-approval tools before you commit, and avoid applying for new credit in the months before a major loan. Because new credit is only 10% of your score, careful timing keeps the impact close to zero.

- Pre-qualify first. Pre-approval and pre-qualification tools use soft inquiries, so you can see your odds without a hard pull. Apply only when you are confident (myFICO).

- Space card applications about six months apart. Several card inquiries in a short window compound the dip and read as risk to lenders, since card inquiries are not bundled.

- Do your loan rate shopping in a tight window. Group auto, mortgage, or student loan applications inside 14 days to stay safe across both FICO and VantageScore.

- Do not apply for new cards right before a mortgage. A fresh inquiry and a lower average account age can affect the rate you are quoted on a much larger debt.

- A denial does not add a separate penalty. Being turned down does not hurt your score on its own; only the hard inquiry from applying counts, whether you are approved or not.

Used this way, a credit card application is a minor, recoverable event, and often a net positive once the added limit lowers your utilization. The mistakes that genuinely damage a credit rating are missed payments and running up balances, not the act of applying. For how the pieces fit together, see is your FICO score the same as your credit score.