What credit score is needed for a car?

In Canada you generally need a credit score of about 660 to qualify for a prime car loan rate, though approval is common from around 630, and borrowers below that can still finance a car through alternative or in-house lenders at a higher rate. There is no legislated minimum: each lender sets its own bar, so the "score you need" depends on whether you want the lowest rate or simply an approval (FCAC).

Your credit score is a three-digit number from 300 to 900, calculated by Equifax Canada and TransUnion Canada from your credit report, that lenders use to estimate how likely you are to repay (Equifax Canada). For a car loan, the score does two jobs at once: it decides whether you are approved, and it sets the interest rate you pay.

Here is how Canadian credit tiers map to typical auto-loan rates and approval odds:

| Credit tier | Score range | Typical auto-loan APR | Approval outlook |

|---|---|---|---|

| Excellent | 760 - 900 | 6% - 7% | Best rates, easy approval |

| Very good | 725 - 759 | 7% - 8% | Prime rates available |

| Good | 660 - 724 | 8% - 10% | Mainstream prime approval |

| Fair | 560 - 659 | 11% - 15% | Often approved, higher rate |

| Poor | 300 - 559 | 15% - 30% | Alternative or in-house lenders |

APR ranges are typical 2026 market ranges and vary by lender, vehicle age, and loan term. The blended national average across all tiers was about 6.5% in late 2025 (Statistics Canada, Table 10-10-0060-01). For a broader view of where rates sit today, see what the interest rate is in Canada.

The takeaway: 660 is the practical line for a good rate, but it is a sliding scale, not a cutoff. A 640 score does not block you from a car loan; it just costs more than a 720 score would.

How much does your credit score change a $30,000 car loan?

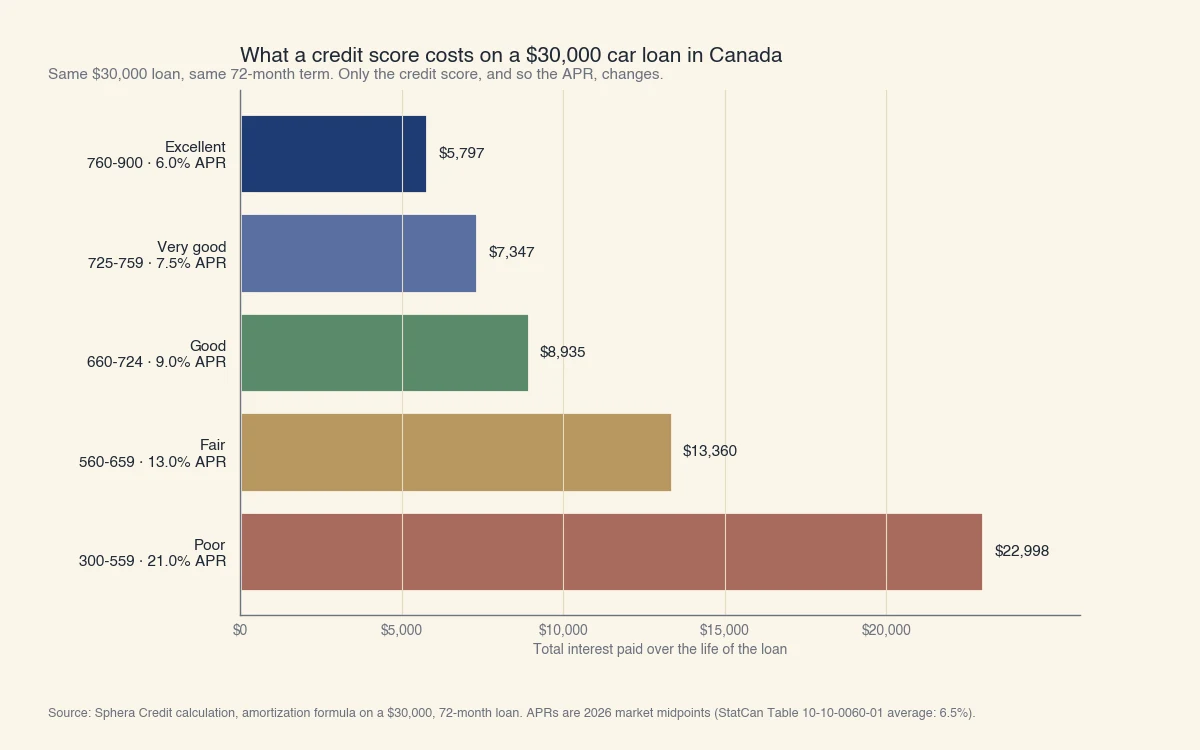

On a $30,000 car loan repaid over 72 months, moving from poor credit to excellent credit saves roughly $17,000 in interest, because the rate falls from about 21% to about 6%. The score does not change the price of the car, but it changes the price of borrowing for it, and on a five-figure balance that gap is large.

The chart below runs the same $30,000 loan over the same 72-month term at the typical APR for each credit tier, and shows the total interest paid:

Source: Sphera Credit calculation using the standard loan amortization formula on a $30,000, 72-month loan. Tier APRs are representative 2026 Canadian market midpoints consistent with the 6.5% national average reported by Statistics Canada (Table 10-10-0060-01).

The monthly payment tells the same story from the buyer's side:

- Excellent (6%): about $497 per month, roughly $5,800 in total interest.

- Good (9%): about $541 per month, roughly $8,900 in total interest.

- Fair (13%): about $602 per month, roughly $13,400 in total interest.

- Poor (21%): about $736 per month, roughly $23,000 in total interest.

A fair-credit buyer pays about $105 more every month than an excellent-credit buyer for the identical vehicle, and nearly $7,600 more over the life of the loan. This is why raising your score even one tier before you apply can be worth more than haggling on the sticker price.

What can you do if your credit score is below 660?

If your score is below 660, you can still finance a car by strengthening the parts of the application a lender weighs alongside the score: a co-signer, a larger down payment, stable income, and a manageable debt load. Lenders, especially alternative and in-house dealer lenders, look at the whole file, not the score alone.

The most effective levers:

- Add a co-signer. A co-signer with strong credit lets the lender price the loan against their profile, which can open up approval or a lower rate. The co-signer is legally responsible if you miss payments.

- Put more money down. A larger down payment lowers the lender's loan-to-value risk and shrinks the balance you pay interest on. It is the single most reliable way to offset a weaker score.

- Show stable income and a low debt load. Lenders check your debt-to-income ratio, the share of your gross monthly income that goes to debt payments. A lower ratio reassures a lender that you can absorb the new payment, even if your score is only fair.

- Use alternative or in-house lenders. Subprime and dealer in-house lenders specialize in scores from 300 to 559. They approve more applicants but charge more, so treat their rate as a starting point to refinance away from once your score recovers.

A car loan can also rebuild credit. Because it is an installment loan reported monthly to Equifax and TransUnion, a year of on-time payments adds positive history and can move you up a tier, at which point refinancing to a lower rate becomes realistic.

Does shopping around for a car loan hurt your credit score?

Comparing several car lenders does not meaningfully hurt your score, because Canadian scoring models de-duplicate multiple auto-loan inquiries made within a short shopping window and count them as a single inquiry. The myth that "every application drops your score" stops people from comparing rates, which is exactly the behaviour that would save them money.

Two misconceptions are worth correcting directly:

- "Each lender I apply to wrecks my score." A single hard inquiry typically costs only a few points, and the rate-shopping window means a cluster of auto-loan checks over roughly two weeks is treated as one event by the scoring model (Equifax Canada). Spreading the same applications across two months, by contrast, can register as separate inquiries.

- "There is a hard minimum score, and below it I am locked out." Lenders do not switch from "yes" to "no" at a single number. They tier the risk and adjust the rate. A 655 score is not rejected; it is simply priced a notch above a 665 score. Approval and rate are a gradient, not a gate.

The practical move: get pre-approved by your bank or a credit union first to set a baseline rate, then let the dealer try to beat it, and keep all the inquiries inside the same two-week window.

How to raise your credit score before you apply

The fastest way to qualify for a better car-loan rate is to lower your credit utilization and make every payment on time in the months before you apply, since payment history and amounts owed are the two largest factors in your score. Even a 20 to 40 point gain can move you across a tier boundary and into a lower rate band.

What moves the number, in order of impact:

- Pay every bill on time. Payment history is the single biggest factor. One missed payment can drop a good score by 60 points or more and lingers for six years (FCAC).

- Lower your credit-card balances. Getting utilization below 30%, and ideally below 10%, of your limits can lift a score within one or two billing cycles. This is detailed in our guide on how to increase your credit score.

- Avoid opening new accounts right before applying. New credit applications add hard inquiries and lower your average account age, both small negatives at the worst possible time.

- Check your report for errors. Dispute incorrect late payments or accounts that are not yours. You can pull your report free from Equifax and TransUnion; see how to check your credit score.

If you are not sure which tier you are in today, start with what counts as a good credit score in Canada, then time your car purchase for after your next reported balance update.

At Sphera Credit, our work is making lending decisions more accurate and fair, especially for borrowers who sit just outside a lender's standard credit box. A 640 applicant with steady income and a solid down payment is often a better risk than the score alone suggests, and that is exactly the kind of nuance a careful assessment is built to catch.