Does Affirm affect your credit score?

Affirm does affect what shows up on your credit file with Experian and TransUnion, but as of 2026 most Affirm activity is not yet weighted in your traditional FICO or VantageScore number. That gap between "appears on your file" and "moves your score" is the most important thing to understand about this question, and it is the change most existing articles miss.

The short version, current to 2026:

- Pay-in-4 (4 biweekly payments). A soft credit check at prequalification, no hard inquiry, no impact on your score from applying. The trade line is reported to Experian (since April 1, 2025) and TransUnion (since May 1, 2025). It is not reported to Equifax. The trade line appears on your file but is not yet factored into FICO 8 or VantageScore 4.0.

- Pay Monthly (6 to 60 months, 0 to 36% APR). Some applications trigger a hard inquiry, which can drop your score by a few points temporarily. The loan reports to Experian and TransUnion, including the monthly payment history. Late payments of 30 days or more behave like any other installment-loan delinquency and do affect your traditional score.

You can think of the Affirm question as two separate questions stacked together: what gets reported and what gets scored. Most readers conflate them. The rest of this page walks through the difference, the bureau-by-bureau picture, and what to monitor going forward.

What changed in 2025 with Affirm's bureau reporting

Between March 19 and April 22, 2025, Affirm rolled out two policy expansions that materially flipped the answer to this question, and most articles still online were written before those changes. The detail matters because the older advice ("Pay-in-4 has no credit reporting at all") is now factually wrong.

The timeline:

- March 19, 2025. Affirm and Experian jointly announced that Affirm would begin reporting all pay-over-time products to Experian, including Pay-in-4, for loans issued on or after April 1, 2025 (Affirm Holdings, March 19, 2025; Experian Global News Blog).

- April 22, 2025. Affirm and TransUnion announced an equivalent expansion: all Affirm pay-over-time products, including Pay-in-4, would be reported to TransUnion for loans issued on or after May 1, 2025 (Affirm Holdings, April 22, 2025; TransUnion Newsroom).

- As of 2026. Affirm has not announced equivalent reporting to Equifax. If your free credit-monitoring app pulls only Equifax data, you will not see Affirm activity at all.

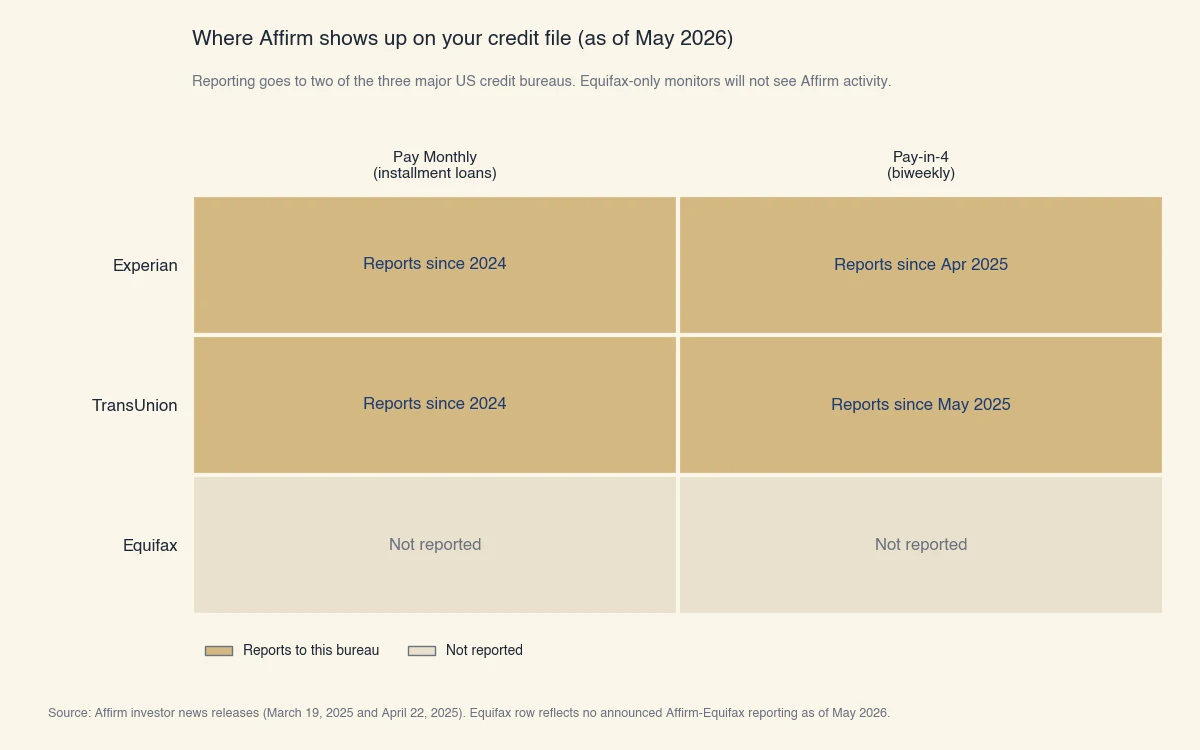

Here is the same information laid out by bureau and product:

| Bureau | Pay-in-4 (biweekly) | Pay Monthly (installment) |

|---|---|---|

| Experian | Reports loans issued from April 1, 2025 onward | Reports established before 2025 |

| TransUnion | Reports loans issued from May 1, 2025 onward | Reports established before 2025 |

| Equifax | Not reported | Not reported |

Source: Affirm investor news releases (March 19, 2025 and April 22, 2025). Equifax cell reflects no announced Affirm-Equifax data sharing as of May 2026.

The dates are not arbitrary. The bureaus and Affirm both staggered the rollout so that legacy loans (issued before the cutoff) would not retroactively change credit files. If you took out a Pay-in-4 loan in February 2025, that one is invisible to the bureaus. The next one in June 2025 is visible.

Reported to your file vs counted in your score

Appearing on a credit file and being weighted in a credit score are two separate things, and Affirm sits squarely in the gap between them right now. This is the single point where the SERP for this question is most misleading.

Both Experian and TransUnion confirmed in their 2025 announcements that the new BNPL trade lines will not be factored into traditional credit scores in the near term. Quoting TransUnion's newsroom directly: consumers will see Affirm transactions on their TransUnion credit files, "though these transactions will not be factored into traditional credit scores nor visible to lenders in the near-term" (TransUnion Newsroom).

Why? Traditional FICO 8 and VantageScore 4.0 scorecards were built before short-term BNPL was a meaningful product, and the models do not yet have a calibrated way to weight a six-week, four-payment installment with a $200 balance against a 60-month $20,000 personal loan. Treating them the same would distort scores in unpredictable ways. Until newer scorecards (FICO 10T, UltraFICO, VantageScore 5.0) are widely adopted by lenders, the BNPL trade lines essentially sit on the file as informational entries.

What this means in practice:

- Your FICO 8 score today. Adding three Affirm Pay-in-4 loans to your file will not change your score, even if you pay them all on time.

- A future FICO 10T or VantageScore 5.0 score. Newer trended-data models can read Affirm trade lines, and on-time payments will likely contribute positively when a lender uses one of these models.

- A late Pay Monthly payment. This is the exception. Pay Monthly is a regular installment loan and a 30-plus-day delinquency on it has always been factored into traditional scores, regardless of the BNPL-specific reporting changes.

This is the counterintuitive piece. "Affirm reports to bureaus" sounds like "Affirm affects your score." For Pay Monthly delinquencies, that's true. For everything else right now, it isn't.

The two ways Affirm can move your traditional score today

Even with the file-vs-score gap above, two specific Affirm activities still move your traditional FICO or VantageScore number on day one. These are the practical levers most readers care about.

Hard inquiry on a Pay Monthly application

When you apply for a Pay Monthly loan above a certain amount, Affirm runs a hard credit pull on Experian or TransUnion. A single hard inquiry typically lowers your FICO score by fewer than 5 points and the effect fades over a year, falling off entirely after two years (myFICO inquiries explainer).

If you apply for many Pay Monthly loans in quick succession, the inquiries stack and the cumulative effect can be larger. Pay-in-4 prequalification uses a soft inquiry only, so applying for or using Pay-in-4 will never trigger a hard pull.

A 30-day-or-longer delinquency on Pay Monthly

The strongest lever in either direction. A single 30-day late payment on a Pay Monthly loan is reported and treated like any other installment-loan delinquency. Industry consensus, confirmed by Fair Isaac's published methodology, is a typical drop of 40 to 110 points depending on your starting score and credit profile, with higher scores falling further in absolute terms (Fair Isaac, FICO methodology).

The delinquency stays on your report for up to seven years from the date of first missed payment, even after you pay it off. Recent payments matter more than old ones in scoring, so the impact fades over time, but the entry remains visible to lenders. For the full diagnostic of what can drop a US credit score and by how much, see why credit scores fall and how to diagnose the cause.

For Pay-in-4, late-payment reporting is now the same in principle, but because Pay-in-4 trade lines are not yet weighted in FICO 8 / VantageScore 4.0, the score impact is currently muted relative to a Pay Monthly delinquency. That is not a guarantee for the future. The recovery path after a missed-payment hit is covered in how to boost a US credit score.

How the three bureaus differ for an Affirm user

The bureau you happen to monitor changes whether you see Affirm activity at all, which is unusual for a consumer credit product and worth flagging directly. Most credit products report to all three bureaus simultaneously; Affirm does not.

- Experian users. Full visibility into Affirm activity from April 1, 2025 onward across both products. The free Experian app shows new Affirm trade lines as they are reported.

- TransUnion users. Full visibility from May 1, 2025 onward.

- Equifax users. Zero visibility into Affirm activity. Some of the most popular free credit-monitoring tools historically pulled Equifax data only (this has changed in places, but if your tool says "powered by Equifax" you may still be in this group).

If you want a complete picture of your file as it relates to Affirm, pull both Experian and TransUnion through annualcreditreport.com, the federally mandated free-disclosure portal. Pulling all three bureaus is free and the inquiries are soft, so it has no effect on your score.

How to monitor what Affirm has reported about you

A few minutes of monitoring once a quarter is enough to catch reporting errors and missed payments before they cause real damage. The mechanics are simple:

- Pull your free Experian and TransUnion reports through annualcreditreport.com. You can pull each bureau once per week at no cost.

- Check the trade-line listing for entries labeled "Affirm" or similar. Confirm the loan amount, original date, and payment status match what you expect.

- Use Affirm's app to compare against what you owe, what you have paid, and the reporting frequency.

- If a trade line is wrong, dispute it through both Affirm and the bureau directly. Federal Fair Credit Reporting Act rules give you the right to a 30-day investigation and a written response (CFPB on disputing credit-report errors).

The Equifax gap remains until Affirm announces reporting there. Until then, an Equifax-only check is incomplete for any user with Affirm activity.