Educational only: please read first

The information below is for general educational purposes and is not financial advice, credit counselling advice, legal advice, or a recommendation to take any specific action. Credit scoring in Canada is governed by federal law, provincial consumer-protection rules that vary across the country, and proprietary scoring models held by Equifax Canada and TransUnion Canada. How those rules apply to any individual depends on facts this article cannot know. For financial guidance, consult a licensed financial advisor or a non-profit credit counsellor. For legal questions about how a provincial statute applies to your specific situation, consult a lawyer licensed in your province.

What "increasing" your credit score actually means in Canada

A Canadian credit score is a 300-to-900 number generated by Equifax Canada or TransUnion Canada from data they hold on your borrowing and repayment behaviour, and "increasing" it means changing the inputs the scoring model rewards. The two national consumer bureaus operate under federal-level rules (FCAC) but their proprietary scoring models, including Equifax Risk Score 2.0 (ERS 2.0) and TransUnion's CreditVision NA, weigh the inputs slightly differently. Most people start somewhere near the average credit score in Canada and want to climb from there.

The phrase "how to increase credit score" hides three different starting positions that have different answers:

- Increase from low to fair (say, 540 to 640): the borrower has serious negative items and is rebuilding. Different tactics work here than for higher tiers.

- Increase from fair to good (640 to 720): the borrower has a thin or mid-range file and needs to add positive history while managing utilization. If your score recently fell, the diagnostic side of this question is covered in why credit scores fall and how to diagnose the cause.

- Increase from good to excellent (720 to 800-plus): the borrower already qualifies for prime credit and is optimizing the last factors. Most "quick wins" do little here.

Knowing your starting tier determines which tactics are likely to help, which are likely to do nothing, and which can briefly hurt before they help.

What this article does not cover

This article does not recommend any specific bank, lender, fintech app, credit-monitoring service, or credit-builder product available in Canada. It does not tell anyone to apply for, sign up for, or close any specific account. The categories of credit-building tools described below (secured cards, credit-builder installment products, alternative-payment-reporting services) are described at the category level only, with their general mechanics, typical cost ranges, and trade-offs, so readers can evaluate any specific provider on their own.

Provincial differences that affect your credit score

Credit-score calculation is national: Equifax Canada and TransUnion Canada apply the same scoring methodology coast to coast. The differences live in the laws around credit reporting, debt collection, and consumer credit, which are partly federal and partly provincial. Several of these provincial differences shape the path from a negative item to its eventual disappearance from the credit report. Citations below point to primary statutory text; they describe what the statutes provide, not how they apply to any individual situation.

Federal anchors that apply across all provinces

- FCAC supervision of federally-regulated financial institutions. The Financial Consumer Agency of Canada supervises federally-regulated banks and federal credit unions on consumer-protection compliance, including how lender disclosures interact with credit reporting.

- Section 347 of the Criminal Code: the federal interest-rate ceiling. Section 347 makes it a criminal offence to receive interest at an effective annual rate above a federally-set ceiling that includes most fees. The ceiling has been revised over time. Quebec also applies a separate framework under its provincial Consumer Protection Act in addition to Section 347.

- The Bankruptcy and Insolvency Act. The BIA governs personal bankruptcy and consumer proposals federally; the discharge dates and durations interact with credit-report aging.

Provincial differences that matter

| Province | Notable provincial rule that touches credit | Why it can matter |

|---|---|---|

| Quebec | Civil Code of Quebec and Consumer Protection Act govern consumer credit, disclosure, and language requirements separately from the rest of Canada | Different framework for credit-contract obligations, complaint processes through the Office de la protection du consommateur, and language-of-disclosure rules |

| Ontario | Limitations Act, 2002 sets a 2-year basic limitation period for most consumer debt actions | A debt-collection action filed beyond the limitation period may not be enforceable through the courts, though the underlying debt and credit-report notation can persist |

| British Columbia | Limitation Act, S.B.C. 2012, c. 13 sets a 2-year basic limitation period; older debts under prior law had a 6-year period | The transition between the old and new periods affects very old debts |

| Alberta | Limitations Act, R.S.A. 2000, c. L-12 sets a 2-year limitation for most consumer debt | Similar to Ontario; collection litigation outside the period may not be enforceable |

| Saskatchewan | The Limitations Act, S.S. 2004, c. L-16.1 sets a 2-year basic limitation period | Provincial debt-collection conduct is also governed by the Saskatchewan Collection Agencies Act |

The dates above describe when a creditor can still sue to collect a debt. They are different from how long a debt or default can appear on a credit report, which is generally 6 years from the date of last activity for most items under the federal-level reporting standards followed by Canadian bureaus.

Where the provincial framework matters most

The provincial framework matters most for borrowers whose credit problems involve:

- Old debts approaching or past the provincial limitation period. A debt past the limitation period in the relevant province may not be enforceable in court, even if it still appears on the credit report. This is a legal question, not a scoring question, and a lawyer licensed in the province is the right consultation.

- Debts disputed during a divorce or separation under provincial family law. The provincial family-law framework determines how shared debt is allocated, but the credit bureau's record reflects who signed the original contract. Aligning the two requires both a family-law process in the relevant province and an FCAC-style dispute with the bureau.

- Debt assigned to collection agencies. Each province licenses and regulates collection agencies under provincial legislation, with different rules around contact frequency, hours, and required disclosures.

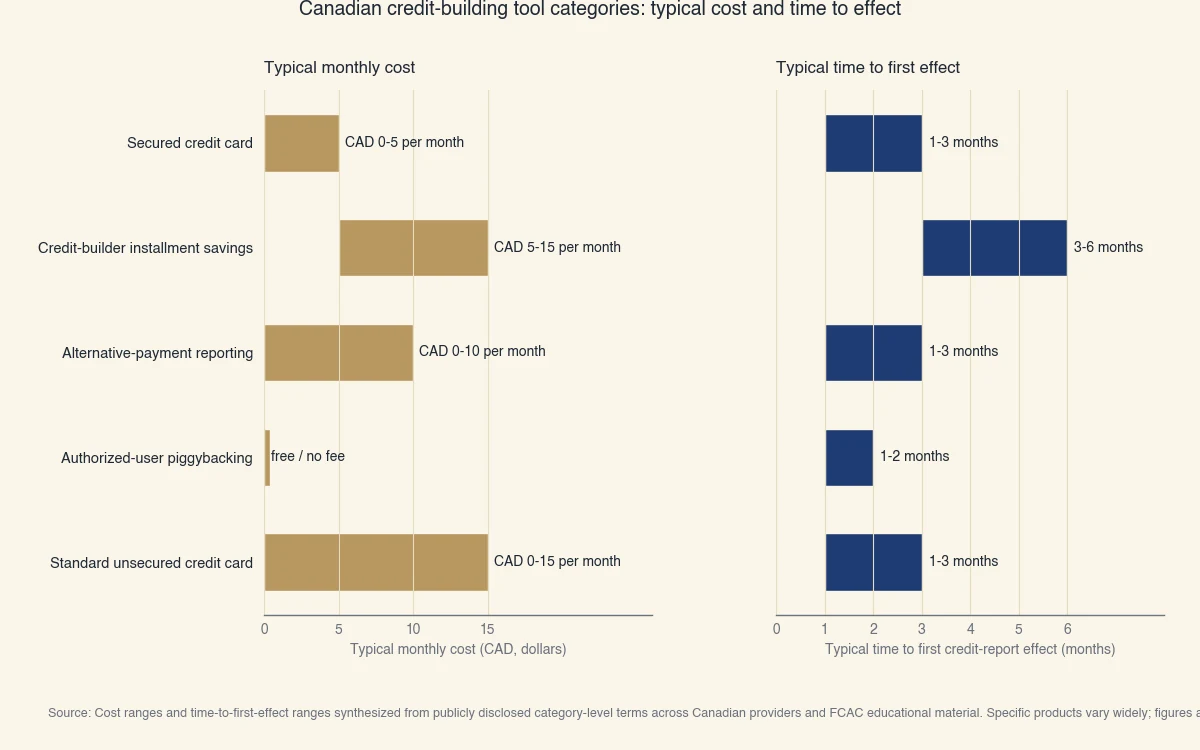

Types of credit-building tools in Canada

Several categories of credit-building tools exist in the Canadian market, each with different mechanics, costs, and credit-reporting behaviour. The table below describes the categories themselves, not specific products. Costs and time-to-impact ranges are typical industry ranges, not guarantees. Always read the terms of any specific provider before signing up.

| Tool category | How it works | Typical cost range | Time to first effect | Often used by | Risks to be aware of |

|---|---|---|---|---|---|

| Secured credit card | Borrower funds a security deposit roughly equal to the credit line; on-time payments report to bureaus as revolving credit | $0 to $60 annual fee, plus the deposit (refundable) | 1 to 3 statement cycles | Newcomers, post-bankruptcy, thin-file rebuild | Deposit is held until the account is closed in good standing; not all secured cards report to both bureaus |

| Credit-builder installment savings product | Borrower makes fixed monthly payments into a savings account they cannot access until the term ends; each payment reports as on-time installment activity | Varies; some products charge interest on the locked savings | 3 to 6 months for first reporting | Thin-file builders, those who want a forced-savings angle | Early termination usually forfeits some interest or returns the savings without the credit-history benefit; interest rates vary widely |

| Alternative-payment reporting (rent, utilities, telecoms) | Service connects to a bank or biller and reports on-time payments to a bureau as positive trade-line data | Free to ~$10 per month | 1 to 3 statement cycles | Renters and those with thin files who pay these bills regularly | Some services also report missed payments, which can hurt the score; not every scoring model weights alternative-payment data; cancellation may not remove already-reported history |

| Authorized-user piggybacking | Primary cardholder adds the borrower as an authorized user; the account history may report on the borrower's credit file | Often free to add | 1 to 2 statement cycles after the issuer reports | Thin-file family members of someone with a strong credit-card history | If the primary cardholder misses payments or runs up the balance, the negative history can flow to the authorized user too |

| Standard unsecured credit card (used responsibly) | Borrower applies for a regular credit card and uses it for small recurring purchases paid in full each month | Varies by card; many no-fee options | 1 to 3 statement cycles | Borrowers with established credit who can qualify | A hard inquiry on application; a denied application still creates a hard inquiry |

A simple decision flow

Where a borrower starts often points to a different category as the most useful first move:

- Score below 600 (or thin file with no score): the secured-card or credit-builder installment-savings categories are the most common starting points because they accept borrowers without strong existing credit.

- Score 600 to 680: the highest-leverage moves are usually utilization tactics on existing cards and disputing inaccurate items, not new accounts. Alternative-payment-reporting services may add a modest positive signal. The credit card payoff calculator projects how long a paydown takes at your current balance and APR.

- Score 680 or higher: time, mix, and account age matter more than any new tool. Opening new accounts at this tier often costs more in inquiry-and-age effects than it gains.

How a Canadian credit score is calculated

Both Equifax Canada and TransUnion Canada use proprietary scoring models built around five common factors: payment history, utilization (amounts owed), length of credit history, credit mix, and new credit. The exact weights are model-specific and not always published in full, but the general framework is consistent across both bureaus.

| Factor | Approximate influence | What it measures |

|---|---|---|

| Payment history | Largest single factor | On-time vs late vs missed payments across all reporting accounts |

| Amounts owed (utilization) | Second-largest factor | Utilization on revolving accounts and balance-to-loan ratios on installment accounts |

| Length of credit history | Moderate | Age of the oldest account, age of the newest, and average account age |

| Credit mix | Smaller | Whether the file has a mix of revolving and installment trade lines |

| New credit | Smaller | Recent hard inquiries and recently opened accounts |

Source: Cost ranges and time-to-effect ranges synthesized from category-level industry data and FCAC educational material. Specific products vary widely; figures are typical and not guaranteed for any individual provider.

The FCAC's "Improving your credit score" guidance summarizes the same five factors in its consumer materials. Population-level credit data appears in the Bank of Canada Financial System Review and the Statistics Canada Survey of Financial Security.

Disputing inaccurate items and exercising your rights

Borrowers in Canada can dispute inaccurate or incomplete information directly with Equifax Canada and TransUnion Canada at no cost, and the bureau is required to investigate the dispute under federal-level reporting standards. This is the single highest-leverage action available to most borrowers with derogatories on file, and it does not require any paid service.

Steps the FCAC describes for disputing a credit-report error:

- Pull the report from each bureau. Each Canadian consumer is entitled to a free credit report on request from both Equifax Canada and TransUnion Canada under the federal-level reporting standards.

- Identify the specific error. Errors include accounts that do not belong to the borrower, incorrectly-reported late payments, balances that do not match statements, accounts incorrectly reported as in collection, or duplicate listings.

- File the dispute directly with the bureau. Disputes can be filed online, by phone, or by mail with each bureau separately. Both bureaus must investigate and respond within a defined timeframe.

- Provide supporting documentation. Receipts, statements, court documents, or correspondence with the original creditor strengthen the dispute.

Disputing through the bureau is free. Most paid "credit repair" services file the same disputes the borrower can file directly. The FCAC educational materials describe the dispute process as a consumer right that does not require professional intermediaries.

Patterns that consistently help, and patterns that rarely do

Across the published consumer guidance from FCAC, Equifax Canada, TransUnion Canada, and population-level credit research, the patterns that show up consistently are pay on time, keep utilization low, limit hard inquiries, build long credit history, and dispute inaccuracies. Many other tactics that get circulated as "tips to increase a credit score" do little or actively hurt:

- Closing old credit cards to "clean up" the file. This shortens average account age and reduces total available credit, both of which usually lower the score.

- Paying for an instant boost through products that promise rapid score gains. Score gains are tied to underlying file changes that take time to register.

- Co-signing for someone else as a way to demonstrate "credit-mix" diversity. Co-signed accounts appear on both files identically; one missed payment hits both.

- Closing a paid-off installment loan account early. The closure reduces credit-mix diversity and stops the account from aging.

The patterns that work are slow and unglamorous, and they are the ones in the FCAC's official guidance. Time is the single most reliable lever in credit-building, and most of the rest is letting the federal and provincial frameworks work as designed.