Educational only: please read first

The information below is for general educational purposes and is not financial advice, credit counselling advice, legal advice, or a recommendation to take any specific action. Credit scoring is governed by federal law and a small number of scoring models, but how those rules apply to any individual depends on facts this article cannot know. For guidance on your situation, consult a licensed financial advisor, a non-profit credit counsellor, or, for disputes and rights questions, a consumer-protection attorney.

What "boosting" your credit score actually means

A credit score is a 300-to-850 number generated by a statistical model from your credit-report data, and "boosting" it means changing the inputs the model rewards. In the United States, the dominant models are the FICO Score (versions 8, 9, and 10 are most current) and the VantageScore (3.0 and 4.0). Each model assigns weights to a small number of factors drawn from the data the three nationwide credit bureaus (Equifax, Experian, TransUnion) hold on you (Fair Isaac methodology).

The phrase "how to boost credit score" hides three different questions that have different answers:

- Boost from low to fair (say, 540 to 640): the borrower has serious negative items and is rebuilding. Different tactics work here than for higher tiers.

- Boost from fair to good (640 to 720): the borrower has a thin or mid-range file and needs to add positive history while keeping utilization low. For where the tier cutoffs come from, see what counts as a good credit score.

- Boost from good to excellent (720 to 800+): the borrower already qualifies for prime credit and is optimizing the last factors. Most "quick fixes" do little here.

Knowing which tier you are starting from determines which tactics are likely to help, which are likely to do nothing, and which can briefly hurt before they help. The rest of this article is organized around that logic. If you specifically need the quickest wins, how to raise your credit score fast ranks the levers by how soon each one moves your score.

What this article does not cover

This article does not recommend any specific bank, lender, fintech app, credit-monitoring service, or credit-builder product. It does not tell anyone to apply for, sign up for, or close any specific account. The categories of tools mentioned below (secured cards, credit-builder installment products, alternative-payment-reporting services, authorized-user piggybacking) are described at the category level only, with their general mechanics and trade-offs, so readers can evaluate any specific provider on their own.

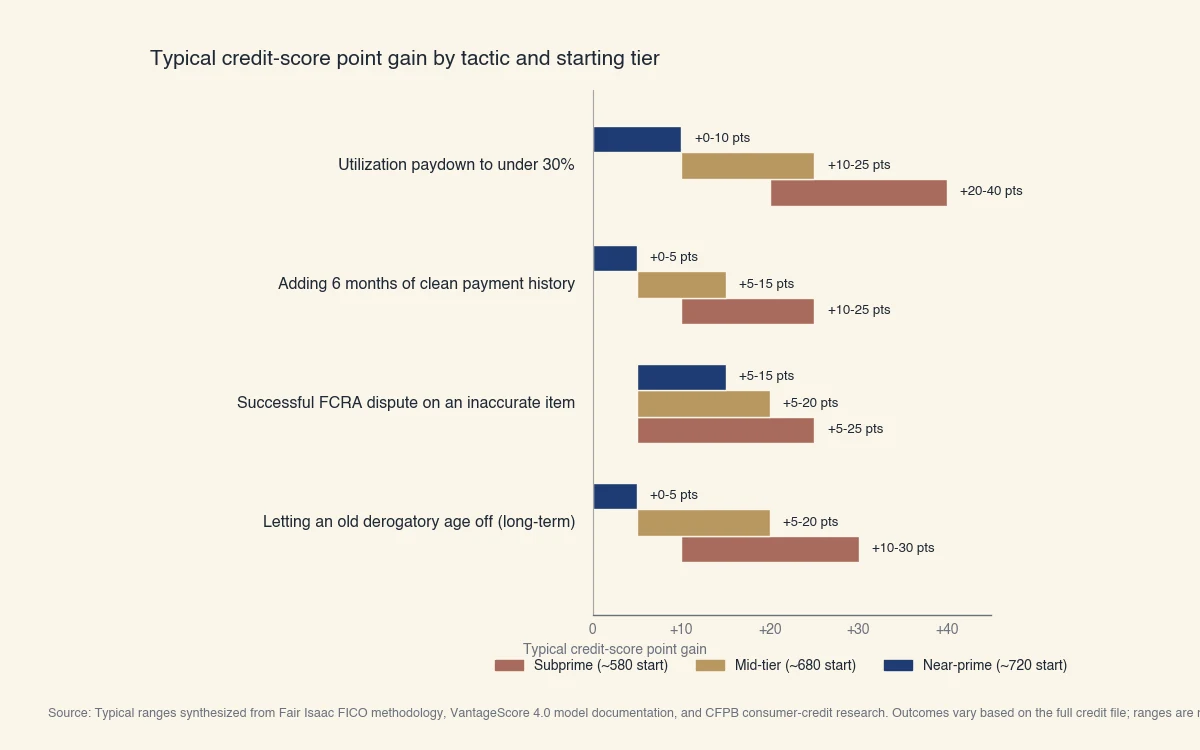

How much will each tactic actually move your score?

The size of the score change from any given tactic depends almost entirely on the borrower's starting point and current file composition, so a tactic that moves a 580 score by 40 points may move a 740 score by 5 points or zero. This section walks through three representative scenarios with the kind of point ranges that scoring-model documentation supports. None of these are guaranteed outcomes for any individual.

Source: Typical ranges synthesized from Fair Isaac FICO methodology documentation, VantageScore 4.0 model documentation, and CFPB consumer-credit research. Outcomes for any individual depend on the full credit file and cannot be predicted from this chart alone.

Scenario A: starting around 580 (subprime)

A borrower at this tier typically has at least one of: a recent late payment within the past 24 months, an active collection or charge-off, very high utilization, or a thin file with limited positive history. Two tactics tend to move the score the most:

- Utilization paydown. Bringing a maxed-out card from 95% utilization down to under 30% (or, more aggressively, under 10%) often shows in the next statement cycle. Typical gains in this tier: 20 to 40 points within 30 to 45 days. To plan a specific paydown trajectory, the credit card payoff calculator projects how many months and how much interest the paydown will cost at your current balance and APR.

- Adding positive payment history. A secured-card category product, used for small recurring purchases and paid in full each month, can add 6 to 12 months of clean payment history that the scoring model rewards. Typical gain after 6 months of perfect payment: 10 to 25 points, depending on what else is on the file.

Tactics that tend to do less at this tier: optimizing credit mix (the file is too thin for mix to matter much), and chasing rapid disputes for cosmetic items (legitimate disputes still help, but the highest-leverage moves are utilization and payment history).

Scenario B: starting around 680 (mid-tier)

A borrower at this tier usually has a clean recent payment history but is held back by one or two specific factors: a single old derogatory, mid-range utilization across several cards, or a short average account age. The most useful tactics:

- Targeted utilization sculpting. Spreading balances across cards to push every individual card under 30% can help. The AZEO method (All Zero Except One: zero balance on every card except one with a small balance under 10%) is a more aggressive variant. Typical gain: 5 to 15 points.

- Time and patience for account age. Average-account-age is computed monthly. Keeping older cards open and not opening unnecessary new ones lets time work. Typical gain over 12 months: 5 to 15 points, holding everything else steady.

- Resolving any single old derogatory. If a paid collection or a 30-day late from years ago is dragging the file, disputing it (if inaccurate) or letting it age past the 7-year FCRA reporting window removes it.

Scenario C: starting around 720 (near-prime to prime)

This is the diminishing-returns tier, and most of the tactics that move a 580 score barely move a 720 score. The reason is mathematical: the scoring model has already given the borrower most of the credit it can give for the strong inputs. What remains is the small fraction of points tied to the model's most-tightly-graded factors:

- Account age, mix, and inquiry-free time. A borrower who keeps their oldest accounts open, holds a mix of revolving and installment credit, and goes 12+ months without a hard inquiry will gradually drift up. Typical gain over a year: 5 to 15 points.

- Disputing legitimate inaccuracies. If a hard inquiry is unauthorized or a payment is misreported, disputing it under the FCRA's process can help. A successful dispute on a single item can yield 5 to 25 points depending on what was reported.

Tactics that rarely help at this tier: opening new accounts (the inquiry and lower account age usually cost more than the new credit limit gains), paying off installment loans early (the closure can lower mix and average age), and most paid-credit-monitoring features.

Putting the tactics in one table

| Tactic | Typical point range | Time to first effect | Whose tier it usually helps most |

|---|---|---|---|

| Utilization paydown to under 30% | 10 to 40 points | 30 to 45 days | Subprime, mid-tier |

| Utilization paydown to under 10% / AZEO | 5 to 20 points | 30 to 60 days | Mid-tier, near-prime |

| Adding 6 months of clean payment history | 10 to 25 points | 3 to 6 months | Subprime, thin-file |

| Successful FCRA dispute on inaccurate item | 5 to 25 points | 30 to 45 days | All tiers |

| Letting a 7-year-old derogatory age off | 5 to 30 points | Long-term | Any borrower with old derogatories |

| Opening a new account | Usually negative short-term, neutral to positive long-term | 1 to 12 months | Thin-file borrowers, used cautiously |

| Closing a credit card | Usually negative | 30 to 60 days | Almost no one |

Ranges are typical, not guaranteed. Outcomes vary based on the rest of the credit file.

Where to start based on your situation

Different starting positions call for different tactics, so the same generic "pay on time and keep utilization low" advice will help some readers a lot and barely help others. Five common situations and what scoring-model documentation suggests works in each.

Recent graduate or thin file

A thin file is one with fewer than three reporting trade lines or less than 6 months of credit history. Scoring models cannot generate a confident score from very little data, so the priority is adding positive trade lines without taking on cost.

Common starting tactics: a secured-card category product (where the borrower funds a security deposit equal to the credit line), used for small recurring purchases and paid in full each month. After 6 to 12 months of clean payment history, the score has data to work with. Some borrowers add an alternative-payment-reporting tool to capture rent or utility payments as positive trade lines, with the trade-offs noted in the FAQ.

Gig worker or 1099 income

A self-employed or gig-income borrower faces a quirk: business credit cards from many issuers do not report to consumer credit bureaus, so even years of perfect business-card payment history may not show on the consumer credit file. The score is still built from consumer trade lines.

Common starting tactics: maintain a personal-card portfolio in parallel with any business cards, and check whether each business card is reporting to consumer or business bureaus before relying on it for personal credit-building. The credit-builder installment-product category is sometimes used to add a reporting installment trade line without the income-verification hurdles of a traditional loan.

Recently divorced

Divorce often leaves a credit file with joint accounts that report to both ex-partners. Late payments by one party hit the other's credit file too, regardless of who was responsible under the divorce decree.

Common starting tactics: separate any remaining joint accounts (close them, refinance into one name, or remove the non-responsible party), then dispute any post-separation late payments under the FCRA process if the divorce decree assigns the debt to the other party. The FCRA dispute is to the credit bureau, not to the divorce court, and bureaus must investigate within 30 days under 15 U.S.C. § 1681i.

Post-bankruptcy or active collections

A Chapter 7 bankruptcy stays on the credit report for 10 years from the filing date; Chapter 13 stays for 7 years. Individual collections stay for 7 years from the original delinquency date. The score recovers gradually as positive history accumulates and the negative items age toward removal.

Common starting tactics: small secured-card or credit-builder installment-product category use to rebuild positive history; pay-for-delete negotiation with collection agencies (offering payment in exchange for the agency requesting removal of the trade line, which is at the agency's discretion and is not guaranteed); and avoiding new derogatories during the recovery period. FICO 9 and VantageScore 4.0 ignore paid medical collections, which can matter for borrowers whose collections are medical in origin.

Subprime rebuild

A borrower in the 500-to-580 range with active negative items on the file is rebuilding. The most-weighted scoring factors at this tier are payment history (35% of FICO) and utilization (30% of FICO).

Common starting tactics: stop the bleeding (no new late payments, no new collections), then drive utilization down on any active revolving accounts. The AZEO method, where applicable, can squeeze out a few points by exploiting how the scoring model treats utilization. Patience matters: most of the score recovery from this tier comes from negative items aging off the report on the FCRA's 7-year clock, not from any single quick action.

The five FICO factors and their weights

The FICO 8 model assigns 35% of the score to payment history, 30% to amounts owed (utilization), 15% to length of credit history, 10% to credit mix, and 10% to new credit. These weights, published by Fair Isaac, are the foundation of every tactic in the previous sections.

| Factor | Weight (FICO 8) | What it measures |

|---|---|---|

| Payment history | 35% | On-time vs late vs missed payments across all reporting accounts |

| Amounts owed | 30% | Utilization on revolving accounts and balance-to-loan ratios on installment accounts |

| Length of credit history | 15% | Age of the oldest account, age of the newest, and average account age |

| Credit mix | 10% | Whether the file has a mix of revolving and installment trade lines |

| New credit | 10% | Recent hard inquiries and recently opened accounts |

VantageScore 4.0 weights these factors differently and adds trended data (how balances change over time, not just the current snapshot). The 4.0 model documentation describes payment history, balance trends, age and type of credit, and credit utilization as "extremely influential" or "highly influential" without publishing percentage weights (VantageScore 4.0 documentation).

Hard inquiries, dispute rights, and what to ignore

A hard inquiry typically lowers a score by less than 5 points and falls off the report after 2 years; a successful FCRA dispute on an inaccurate item can yield 5 to 25 points, and most "credit repair" services charge for work the borrower can do for free. This section pulls together the parts of credit-building that are governed by federal law rather than scoring-model behavior.

What the FCRA actually says

The Fair Credit Reporting Act, 15 U.S.C. § 1681, gives every consumer:

- The right to a free credit report from each of the three nationwide bureaus, available at AnnualCreditReport.com under federal law.

- The right to dispute inaccurate or incomplete information directly with the credit bureau. The bureau must investigate within 30 days (45 days in some cases) under § 1681i.

- A 7-year limit on most negative items remaining on the report (10 years for Chapter 7 bankruptcy), measured from the original delinquency date.

- The right to place a security freeze on the credit file at no charge, which prevents new credit from being opened.

Disputing through the bureau is free. Disputing inaccurate items is the single highest-leverage tactic available to almost any borrower with derogatories on file, and it does not require any paid service.

What "credit repair" services typically do

Most paid credit-repair services file the same FCRA disputes a borrower can file directly. Some send aggressive volumes of disputes, which may force the bureau to remove items the original creditor does not respond to in time but which can also be reinserted later if the creditor verifies. The CFPB's research on credit repair describes the industry as one where outcomes are difficult to attribute to the service itself rather than time or borrower-led action.

What rarely helps

- Closing old credit cards to "clean up" the file. This shortens average account age and reduces total available credit, both of which usually lower the score.

- Paying for a higher score in a single month through products that promise instant boosts. Score gains take time and are tied to the underlying file.

- Co-signing for someone else as a way to show "credit-mix" diversity. Co-signed accounts appear on both files identically; one missed payment hits both.

The patterns that consistently show up in scoring-model documentation are the ones in the previous sections: pay on time, keep utilization low, dispute inaccuracies, let time pass.