How is a credit rating calculated?

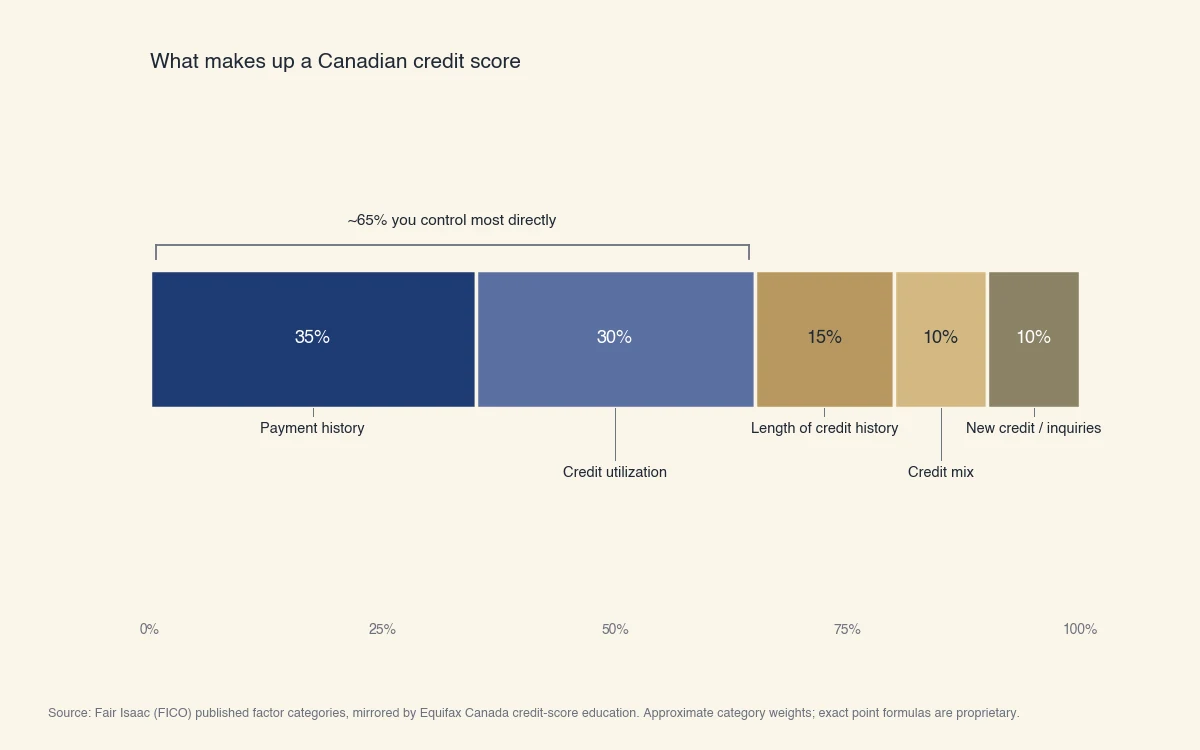

Equifax and TransUnion calculate your credit rating from five factors, led by payment history at about 35%, then credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit or inquiries (10%). The bureaus feed the data on your credit report into a statistical model, most often a version of the FICO score, and the model returns a three-digit number between 300 and 900 (Equifax Canada).

Two things are worth clearing up before the details. First, "credit rating" in Canada means two related but different things: the 300 to 900 credit score, and the R-scale rating (R1 to R9) attached to each individual account. This page covers both and shows how they connect. Second, the bureaus publish the approximate weight of each factor, but they do not publish the exact point formula. Anyone claiming a precise "credit rating calculator" is estimating, not reproducing the real model.

Here is how the five factors break down.

- Payment history (about 35%) is whether you pay each account on or before its due date. It is the single largest input, because past repayment behaviour is the strongest predictor of future repayment.

- Credit utilization (about 30%), sometimes called your debt-to-credit ratio, is how much of your available revolving credit you are using. Using $6,000 of a $20,000 total limit is 30% utilization. Below 30% is generally safe; below 10% is ideal.

- Length of credit history (about 15%) is the average age of your accounts and the age of your oldest account. Older accounts help the score.

- Credit mix (about 10%) is the variety of credit you manage, such as a mix of revolving credit (credit cards) and installment credit (a car loan or line of credit).

- New credit and inquiries (about 10%) counts recent applications and newly opened accounts. Several hard inquiries in a short window can signal risk.

Source: Fair Isaac (FICO) published factor categories, mirrored by Equifax Canada credit-score education. Approximate category weights; exact point formulas are proprietary.

The chart makes the practical point clear. Payment history and utilization together account for roughly 65% of the score, and those are the two factors you control most directly from one month to the next. The other three move slowly and largely take care of themselves as your file ages.

What score range counts as good in Canada?

Most Canadian lenders read the 300 to 900 range in five bands, with 660 and up treated as good and 760 and up treated as excellent. The bands below follow the Equifax Canada scale; TransUnion uses similar cutoffs.

| Range | Label | What it usually means |

|---|---|---|

| 760 - 900 | Excellent | Best advertised rates; approval is routine |

| 725 - 759 | Very good | Most prime products available |

| 660 - 724 | Good | Mainstream qualification range |

| 560 - 659 | Fair | Limited prime options; alternative lenders likely |

| 300 - 559 | Poor | Secured or subprime products only |

The average Canadian score sits around the high 600s, which lands in the "good" band rather than higher. A good score is common; an excellent one is not.

The R1 to R9 rating scale, and how it feeds your score

The R-scale is a rating from R1 to R9 attached to each account on your report, where R1 means you pay on time and R9 means the debt has gone to collection or bankruptcy. Every account also carries a letter for its type: R for revolving credit (like a credit card), I for installment credit (like a car loan), and O for open credit. So an "R2" is a revolving account paid up to 60 days late, and an "I9" is an installment account written off as bad debt (FCAC).

This is the part most guides skip, and it is exactly what confuses people who search "how is a credit rating determined." The R-scale is not a separate score. It is the raw material the payment-history factor reads. Each account's R-rating tells the model how well you handled that account, and those ratings roll up into the 35% payment-history slice of your number.

| Rating | What it means |

|---|---|

| R0 | Account approved but not yet used |

| R1 | Paid within 30 days of the due date, or as agreed |

| R2 | Paid 30 to 60 days late (one to two payments behind) |

| R3 | Paid 60 to 90 days late (two to three payments behind) |

| R4 | Paid 90 to 120 days late (three to four payments behind) |

| R5 | At least 120 days late, but not yet rated R9 |

| R6 | Rarely used (partial or irregular payment arrangement) |

| R7 | Paying through a special arrangement, such as a consumer proposal or debt-settlement plan |

| R8 | Repossession, voluntary or involuntary |

| R9 | Bad debt, sent to collection, or included in a bankruptcy |

How bad is an R7 credit rating?

An R7 is a serious negative mark, because it signals that you could not meet the original terms and are now settling the debt through a special arrangement. It sits near the bottom of the scale, just above repossession (R8) and bad debt (R9). An R7 usually appears when you enter a consumer proposal or a formal debt-management program, and it stays on the account until the arrangement is complete plus the standard reporting period. Because payment history drives about 35% of the score, even one R7 can move a rating from "good" into "fair" or lower. We cover the mortgage side of this in Can you get a mortgage with an R7 credit rating?.

Anatomy of a credit score: a worked Canadian example

Because the bureaus keep the exact point formula private, the honest way to show how a rating is calculated is to walk one realistic file factor by factor and land on a plausible band, not a false exact number. Take a Canadian borrower with this profile:

- Two credit cards with a combined $20,000 limit and a $6,000 balance (30% utilization)

- One car loan, three years into a five-year term, paid on time

- Oldest account opened six years ago; average account age about four years

- One late payment 14 months ago (a single R2 that has since returned to R1)

- One hard inquiry in the past year, from shopping for the car loan

Here is how each factor pushes the number.

- Payment history (35%): Mostly strong. Years of on-time payments help, but the single late payment from 14 months ago still sits on the file and caps this factor below perfect. Directional effect: slightly negative, fading.

- Utilization (30%): At 30%, this borrower is right at the edge of the "safe" zone. Paying the balance down to $2,000 (10%) would be the single fastest lever to lift the score. Directional effect: neutral to slightly negative.

- Length of history (15%): A six-year oldest account and a four-year average are moderate. Time is the only fix here. Directional effect: neutral.

- Credit mix (10%): Revolving cards plus an installment car loan is a healthy mix. Directional effect: slightly positive.

- New credit (10%): One hard inquiry in a year is minor and its impact fades after about 12 months. Directional effect: slightly negative, fading.

A file like this typically lands in the high-600s to low-700s, the "good" band. The takeaway is not a magic number but a priority list: the borrower's two quickest wins are paying the cards down under 10% and letting the lone late payment keep aging. Everything else is already working in their favour.

Why Equifax and TransUnion calculate different scores

Equifax and TransUnion often give the same person two different numbers on the same day, because they keep separate databases and run different scoring models. They are two private companies, not one shared registry. A lender that reports to only one bureau leaves a gap in the other bureau's file, so the inputs are rarely identical (TransUnion Canada).

Three things drive the gap.

- Different data. Not every lender reports to both bureaus, and they report on different schedules. One bureau may already show your latest payment while the other has not updated yet.

- Different models. Each bureau uses its own scoring versions (for example, Equifax's risk scores and TransUnion's CreditVision), and each model weights the same behaviour a little differently.

- Different emphasis. In practice, Equifax tends to lean harder on public records and derogatory items, while TransUnion pays closer attention to credit mix and trended behaviour over time.

The practical takeaway: check both, not just the one your free app shows, and know which bureau your lender pulls before a big application. A strong number at one bureau does not guarantee the same at the other. This is also why the "average" score you see quoted can differ from your own; averages blend both bureaus and many models.

How can you find, get, and fix your credit rating?

You can check your credit rating for free in Canada, you build one by using credit responsibly over time, and you fix a weak one by targeting the two factors that carry the most weight. These are three different questions that searchers often bundle together, so here is each in turn.

How to find and know your rating. Free services show your real bureau score without affecting it:

- Borrowell reports your Equifax score for free.

- Credit Karma reports your TransUnion score for free.

- You can request a free copy of your full credit report directly from Equifax and TransUnion.

All of these are soft inquiries, so checking as often as you like does no harm. To go deeper on the mechanics of self-checks, see How to check your credit score.

How to get a rating in the first place. If you have no credit history, the model has nothing to score. You build a file by opening one starter product, such as a secured credit card or a small installment loan, and paying it on time. A rating usually appears within a few months of your first reported account.

How to fix a weak rating. Because payment history and utilization drive about 65% of the number, that is where to spend effort:

- Pay every account on or before its due date. Even one missed payment creates a negative R-rating that lingers for years.

- Bring utilization below 30%, and below 10% if you can. This is the fastest lever, often visible within one or two billing cycles.

- Leave old accounts open so your average account age keeps climbing.

- Apply for new credit only when you need it, to limit hard inquiries.

For a fuller plan, see How to increase your credit score. None of this is instant, but most negative marks fall off after about six years, and consistent on-time payments rebuild a rating over 6 to 12 months.

Where SpheraCredit fits in: lenders use our AI underwriting to look past a single number when a borrower falls outside the standard credit box, weighing the full picture behind the rating rather than rejecting on the score alone. The goal is an accurate, explainable decision, not a faster one.