Why did my credit score drop?

Your credit score dropped because at least one of the five scoring factors changed against you: a late or missed payment, higher credit utilization, a new hard inquiry, a closed account or reduced limit, or a new negative mark like a collection. In Canada, Equifax and TransUnion recalculate your score every time your file is updated, so even a routine change to a reported balance can move the number (FCAC).

A credit score is a three-digit number, from 300 to 900 at the Canadian bureaus, that estimates how likely you are to repay borrowed money on time. It is rebuilt from your credit report data, not stored as a fixed value, so it rises and falls as that data changes. The question is never really "why did it drop" in the abstract. It is "which line on my report changed, and by how much."

Most competing pages give you a list of causes and stop. This page does three extra things: it shows how many points each cause typically costs and how long it lingers, it explains the silent drops that happen when you did nothing wrong, and it separates the causes by borrower profile, because a thin newcomer file and a thick 20-year file react to the same event very differently.

The five factors, and which one moved

Every score drop traces back to one of these five inputs. The weights below are FICO's published model weights; the Canadian bureau models (Equifax ERS, TransUnion) use the same factors with similar emphasis.

| Factor | Rough weight | What a drop here looks like |

|---|---|---|

| Payment history | 35% | A payment reported 30+ days late; a collection or default |

| Credit utilization (amounts owed) | 30% | A higher reported balance, or a lower total credit limit |

| Length of credit history | 15% | An old account closed; average account age shortened |

| Credit mix | 10% | Paying off and closing your only installment loan |

| New credit | 10% | A hard inquiry from a new application |

If you can identify which of these five changed since your last score, you have found your answer. The rest of this page helps you do exactly that.

Why did my credit score drop for no reason?

A score almost never drops "for no reason." It drops for a reason you cannot see, because the event happened inside your lender's or the bureau's systems rather than in your own spending. Four silent mechanisms explain the large majority of "for no reason" drops, and none of them require you to have missed a payment or made a mistake.

1. The statement balance, not the balance you think you have. Your card issuer reports the balance on your statement closing date, not the balance after you pay. If you charged $2,400 on a $3,000 limit and paid it in full three days after the statement closed, the bureau still received an 80% utilization reading for that month. Your score drops even though you owe nothing. Pay before the statement closes, not just before the due date, and the reported balance stays low.

2. A lender lowered your limit or closed an old card. Banks periodically cut credit limits or close inactive accounts on their own. If your $10,000 limit becomes $6,000 while you carry a $3,000 balance, your utilization jumps from 30% to 50% with no action from you. Closing an old card also shortens your average account age. Both push the score down, and both are triggered by the lender, not by you.

3. A positive account aged off, or the file simply refreshed. Closed accounts in good standing eventually drop off your report, and when they do you can lose some length-of-history and available-limit benefit. Month-to-month, your file is a moving snapshot, so small wobble of a few points is normal even in a clean file.

4. Equifax and TransUnion disagree. The two Canadian bureaus hold different data and update on different days. A lender might report a new balance or a late mark to only one of them, so the score in your app can differ from the score a lender pulls, and one can drop weeks before the other. A gap of a few dozen points between the two is ordinary, not a mistake.

The practical test for a "no reason" drop is simple: pull both your Equifax Canada and TransUnion Canada reports and compare them to last month. One line will have changed. It is usually a reported balance or a limit, not something you did.

How much does each cause lower your score, and how long does it last?

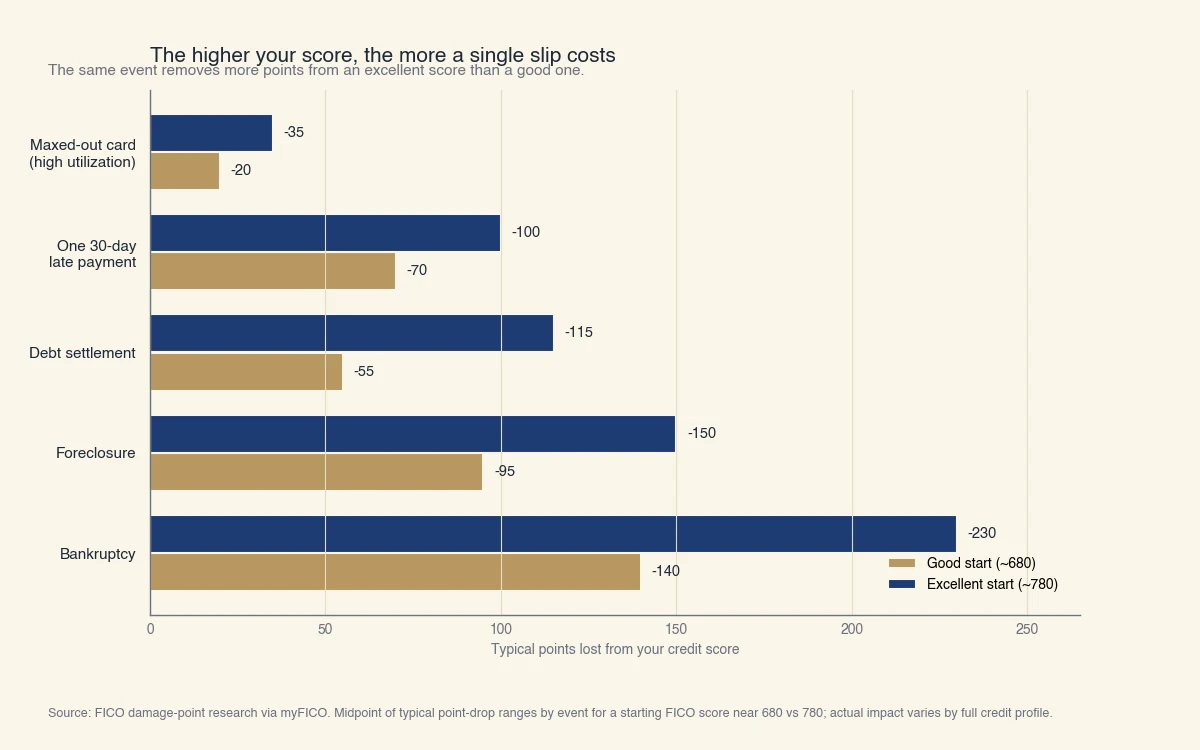

The size of a drop depends heavily on where you started: the higher your score, the more points a single slip removes, because you have more to lose. FICO's own research shows a 30-day late payment costs a borrower near 680 about 60 to 80 points, while the same late payment costs a borrower near 780 roughly 90 to 110 points (myFICO). That is the counterintuitive part most guides miss: a strong score is not a cushion against damage, it is a bigger target.

Source: FICO damage-point research via myFICO. Typical point-drop ranges by event for a starting FICO score near 680 versus 780; actual impact varies by full credit profile. Canadian bureau models behave similarly.

The other half of the question is how long the drop lasts. That depends on the cause, not the point size:

| Cause | Typical point impact | How long it stays on your Canadian file | First recovery step |

|---|---|---|---|

| Higher reported utilization | 10 to 45 points | Clears next statement once balance drops | Pay down below 30%, before the statement date |

| One hard inquiry | A few points, under ~10 | Visible 3 years; impact fades after ~12 months | Stop applying; batch rate-shopping into one window |

| A closed account or lower limit | 10 to 40 points | Ongoing while utilization stays high | Ask to keep the card open or request a limit increase |

| One 30-day late payment | 60 to 110 points | About 6 years | 12 to 24 months of on-time payments |

| A collection or default | 60 to 150 points | About 6 years from first delinquency | Pay or settle; rebuild with on-time credit |

Utilization and inquiry drops are the recoverable ones: they lift within a cycle or two once new data reports. Late payments and collections carry a small immediate hit that heals with time, plus a six-year record on your report (Equifax Canada). Hard inquiries stay visible on your Equifax file for three years but stop affecting the score after about a year, and same-purpose rate shopping inside a short window counts as one inquiry (Equifax Canada).

Why your score dropped depends on your profile

The same event moves different files by wildly different amounts, and the profiles most vulnerable to a surprise drop are the ones with thin or unusual credit files, which generic advice ignores. Find yourself below.

-

Newcomer to Canada with a thin file. If your report holds one or two accounts, a single hard inquiry or one month of higher utilization can swing your score 30 to 60 points, far more than it would move a thick file. There is less positive history to average against, so each new data point carries outsized weight. Building a second or third on-time account is what stabilizes the number over time. If you are still learning where your score sits, start with how to check your credit score in Canada.

-

Self-employed with one high-limit card. Running business expenses through a single personal card spikes your reported utilization near the statement date, even when you pay it off monthly. Because 30% of the score is utilization, this is the most common reason a self-employed borrower sees a score sink and recover in a sawtooth pattern. Spreading charges across two cards, or paying mid-cycle, keeps the reported balance low.

-

In a consumer proposal or recently discharged. A consumer proposal is filed under the Bankruptcy and Insolvency Act and reports as an R7 rating; a bankruptcy reports as R9. These sit on your file for years and are usually the dominant reason the score is low. Rebuilding runs through secured credit and time, not through disputing accurate entries. Our guide on getting a mortgage with an R7 credit rating walks through what borrowing looks like from there.

-

Someone who just paid off a loan. Clearing and closing an installment loan removes an active on-time tradeline and can trim your credit mix and average account age. The drop is small and temporary. Paying off debt is still the right call; the score dip is a reporting artifact, not a penalty.

The through-line is that a drop is only meaningful against your own baseline. A 40-point fall on a thin newcomer file and a 40-point fall on a thick 20-year file mean very different things about risk.

How do I find out what caused the drop, and fix it?

To diagnose a drop, pull both Canadian credit reports, compare them line by line to last month, and match the one account that changed to the five factors above. The change is almost never mysterious once you have both reports side by side.

Work through this order:

- Get both reports. Order your Equifax Canada and TransUnion Canada reports (free by request), and check them against each other, since a change often shows on one before the other (FCAC). Checking your own report is a soft pull and never lowers your score.

- Find the one line that moved. Scan for a new late-payment marker, a higher balance, a reduced limit, a closed account, a new inquiry, or a new collection. That line is your cause.

- Match it to a factor. A balance change is utilization; a late marker is payment history; an inquiry is new credit; a closed account is length and mix. Now you know both the cause and roughly how long it will last, from the table above.

- Dispute anything wrong. If the entry is not yours, has the wrong amount, or was already paid, file a dispute with each bureau where it appears. Correcting an inaccurate negative can restore the points immediately.

- Fix the fixable. Pay balances below 30% before the statement date, stop new applications while you recover, and keep old accounts open. For a full rebuild plan, see how to increase your credit score, and to know what you are aiming for, what counts as a good credit score in Canada.

A single drop is a data point, not a verdict. Most drops from routine activity heal within a billing cycle or two, and even a serious mark loses its weight as fresh on-time history accumulates. At Sphera Credit, we build credit-decisioning tools for lenders that read the full context behind a score rather than a single number, because one month's dip rarely tells the whole story of whether someone can repay.