Does overdraft affect your credit rating in Canada?

No. In Canada, an overdraft on your chequing account does not directly affect your credit rating, because a chequing account is a deposit account rather than a credit account, and banks do not report your day-to-day balance to Equifax Canada or TransUnion Canada. The money in your chequing account is your money, so the bureaus never see it go negative. Your credit rating only takes a hit if you leave the negative balance unpaid, your bank closes or defaults the account, and the debt is sent to a collection agency.

That distinction is the whole answer, and most competing pages stop there. This page goes further: it separates the three different things the word "overdraft" can mean in Canada, shows exactly which events reach your credit file, walks one overdraft from day zero to a collection with real numbers, and covers the March 2026 federal cap that cut non-sufficient-funds fees from roughly $48 to $10.

The 30-second version

- An arranged overdraft you repay quickly: no report, no score impact, just interest and fees.

- Overdraft protection tied to your chequing account: not a credit account, not reported to the bureaus.

- Overdraft protection set up as a line of credit: this one is a credit account and it does report.

- An unpaid negative balance sent to collections: this is what actually damages your rating, and it stays six years.

What is an overdraft, and what is overdraft protection?

An overdraft happens when you do not have enough money in your account to cover a payment or withdrawal, and the bank lets the transaction go through anyway, leaving your balance below zero. Overdraft protection is the optional product that authorizes this, so the payment clears instead of bouncing (FCAC).

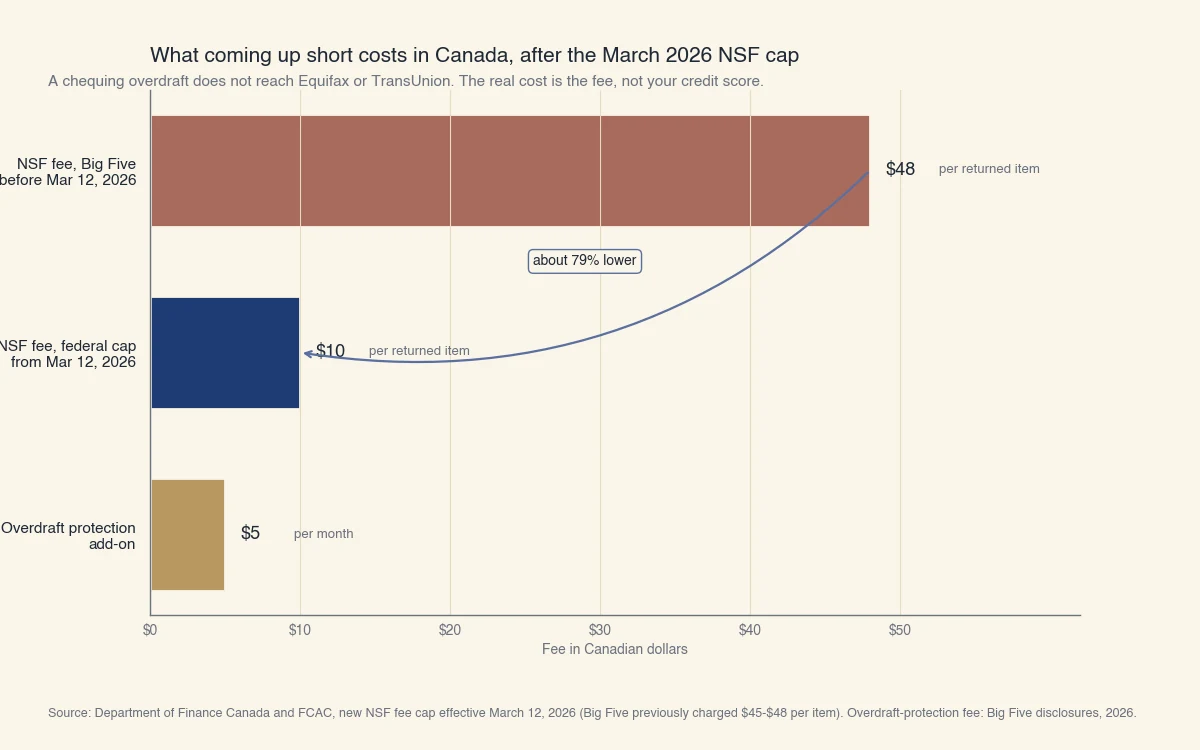

Overdraft protection helps you avoid three things: a declined transaction, a late-payment charge from whoever you were paying, and a non-sufficient-funds (NSF) fee, which is the penalty a bank charges when a payment is returned for lack of funds. In exchange, the bank charges its own fees. At the Big Five, overdraft protection typically costs about $5 per month, plus interest of roughly 19% to 22% on the amount you are overdrawn, charged until you bring the balance back to zero.

The Financial Consumer Agency of Canada is blunt about how to use it: overdraft protection "isn't meant to be an ongoing option to manage any money shortfall. It's meant to be a short-term solution." For longer-term needs, the FCAC points you to a credit product such as a line of credit or a personal loan (FCAC).

Two facts from that FCAC page matter for your credit file. First, many institutions reserve the right to cancel your overdraft protection without notice if you do not clear the balance by the deadline in your agreement. Second, the FCAC states plainly that your account "may default if you don't repay your overdraft balance by the deadline in your agreement," and that this "could hurt your credit score." That default is the bridge between a private banking event and your public credit report.

Which overdraft events actually reach your credit report?

Only events that turn your overdraft into reported credit reach the bureaus: a personal line of credit used for overdraft protection, a written-off balance, or a collection. Everyday overdraft use, overdraft fees, and NSF fees do not appear on your credit report at all. Use this table to see where each event lands.

| Overdraft-related event | Reported to Equifax / TransUnion? | Typical credit impact | How long it lingers |

|---|---|---|---|

| Going into overdraft within your limit, repaid within days | No | None | Not applicable |

| Paying the monthly overdraft-protection fee or overdraft interest | No | None | Not applicable |

| A returned payment and its NSF fee | No (the bank fee is not reported) | None from the fee itself | Not applicable |

| Overdraft protection set up as a personal line of credit | Yes, it is a credit account | Counts toward utilization; on-time helps, missed hurts | While open, plus 6 years for any negative marks |

| Unpaid negative balance the bank writes off | Yes, as a bad debt | Large drop | 6 years from first delinquency |

| Balance sent to a collection agency (about 60 to 90 days) | Yes | Severe drop (rated 9) | 6 years from first delinquency |

| A missed credit card or loan payment caused by a bounced payment | Yes, reported by that creditor | 30-day late mark or worse | 6 years from the missed payment |

The pattern is consistent. As long as the overdraft stays inside your deposit account and you clear it, it is invisible to lenders. The moment it converts into borrowed money that you fail to repay, it becomes a credit event.

How a collection shows up on a Canadian credit file

When a written-off or collected balance lands on your report, it carries a rating code. Equifax Canada uses a letter and a number: the letter is the account type and the number is the payment status. R is revolving credit, I is an installment loan, and O is open credit; the number runs from 1 (paid as agreed) to 9 (written off as bad debt or placed in collection) (Equifax Canada Consumer Credit Report User Guide). A collected overdraft typically shows as a 9, the worst possible status. If you want to see what living with a low rating looks like in practice, our guide on getting a mortgage with an R7 credit rating walks through the lending consequences.

That 9-rated entry stays on your Equifax Canada and TransUnion Canada files for six years from the date of first delinquency, and paying it later does not reset the clock (Equifax Canada).

A worked example: one overdraft from day zero to a collection

The realistic worst case is a small overdraft you forget about, which grows with fees and interest, defaults after about 90 days, and lands as a collection that drops a good score by 60 to 130 points. Here is the full chain with numbers.

Imagine Léa, a 31-year-old in Laval with an Equifax Canada score of 730. A pre-authorized $180 insurance payment clears on a Friday when her balance is only $40. Her chequing account has overdraft protection, so the payment goes through and her balance drops to negative $140.

- Day 0 to Day 14. Léa is overdrawn by $140. The bank charges the $5 monthly overdraft fee and starts accruing interest at about 21% a year. Nothing is reported to any bureau. Her score is still 730.

- Day 15 to Day 60. Léa does not notice the shortfall because her pay is direct-deposited elsewhere. Interest and a second monthly fee push the balance to roughly $160 negative. Still nothing on her credit file.

- Day 61 to Day 90. The balance passes the repayment deadline in her account agreement. Under FCAC-described terms, the bank can cancel the overdraft protection and treat the account as defaulted (FCAC). Her score is still 730, but the countdown has started.

- Day 91 onward. The bank writes off the roughly $170 balance and sells it to a collection agency. The agency reports a 9-rated collection to Equifax Canada. A single collection on a previously-good file commonly costs 60 to 130 points. Léa's 730 falls to somewhere around 620.

- The six-year tail. Even after Léa pays the $170, the collection entry stays on her file for six years from that first delinquency (Equifax Canada).

Now run the same story with one change. If Léa had spotted the shortfall and deposited $170 within two weeks, her total cost would have been about $5 in fees plus a couple of dollars of interest, and her credit rating would never have moved. The entire difference between a non-event and a six-year mark on your file is whether the overdraft gets repaid before it defaults. A sudden, unexplained drop like Léa's is one of the most common reasons a credit score falls.

Source: Department of Finance Canada and FCAC, new NSF fee cap effective March 12, 2026 (Big Five previously charged $45 to $48 per item). Overdraft-protection monthly fee from Big Five bank disclosures, 2026.

Overdraft, NSF, and overdraft protection: the distinction that trips people up

The single point competitors blur is that overdraft protection comes in two forms that behave in opposite ways on your credit file: an add-on to your chequing account (invisible to the bureaus) and a personal line of credit (a reported credit account). The word is the same; the credit consequence is not. Getting this right is the difference between a correct answer and a wrong one.

- Overdraft protection as a chequing add-on. This is the standard $5-per-month product. It sits with your deposit account, so no tradeline is opened and nothing is reported. Your arranged overdraft limit never appears on your credit report.

- Overdraft protection as a personal line of credit. Some banks cover shortfalls by linking a small line of credit to your chequing account. A line of credit is a credit account. It opens a tradeline, its balance counts toward your credit utilization (the share of available credit you are using), and every payment, on time or late, is reported. Here, staying constantly "in overdraft" does affect your rating, because a high utilization ratio pulls scores down even when you never miss a payment.

Then there is the NSF path, which is separate again. A non-sufficient-funds fee is charged when you have no overdraft protection and a payment is returned unpaid. The fee is a bank charge and is not reported to any bureau. The danger is indirect: a returned pre-authorized payment can mean you miss a credit card or loan payment, and that creditor can report a 30-day late mark. The bounced bank transaction is invisible; the missed obligation behind it is not.

This path became a lot cheaper in 2026. As of March 12, 2026, federal regulations cap NSF fees at $10, down from the $45 to $48 the Big Five charged, ban any NSF fee when the shortfall is under $10, and forbid more than one NSF fee per account within two business days (Department of Finance Canada). The rules apply to personal and joint accounts, and the government estimates they will save Canadians about $4.1 billion over ten years, given that more than one in three Canadians incurs an NSF fee each year (FCAC). Lower fees do not change the credit rule, but they shrink the odds that a small shortfall snowballs into an unpaid, collectable balance.

How to keep an overdraft from ever touching your credit

Keep overdrafts short and repaid, watch for the ones you cannot see, and never let overdraft protection become a permanent way of banking. A short checklist that keeps every overdraft in the invisible column:

- Turn on a low-balance alert so you learn about a shortfall the day it happens, not 60 days later.

- Keep a small cash buffer of $100 to $200 in your chequing account for timing gaps between bills and pay.

- Know your repayment deadline. It is written in your account agreement, and missing it is what triggers default (FCAC).

- If a shortfall does happen, clear it within a couple of weeks, well before the 60-to-90-day collection window.

- Confirm which kind of overdraft protection you have. If it is a linked line of credit, treat it like any credit account and keep the balance low.

- For a recurring shortfall, switch tools. A line of credit or a small emergency fund is cheaper and safer than living in overdraft month after month.

If you are not sure whether a past overdraft ever reached your file, request your free Equifax Canada or TransUnion Canada report and read the accounts and collections sections. Our guide on how to check your credit score in Canada walks through where to get it, and if a collection did land, how to increase your credit score covers the rebuild. Checking your own report is a soft pull and never lowers your score (FCAC).