Is 700 a good credit score?

Yes, 700 is a good credit score in Canada. It falls inside the "good" band of 660 to 724 on the 300 to 900 scale that Equifax and TransUnion use, sits above the national average, and qualifies you for most mainstream loans, mortgages, and credit cards (Equifax Canada). What it does not do is get you the single lowest rate a lender advertises, because those best-rate tiers usually start around 760.

Your credit score is a three-digit number that lenders use to estimate how likely you are to repay borrowed money on time. It is generated from your credit report, the file each bureau keeps on your borrowing and repayment history. A 700 tells a lender you have a solid track record with very few problems, which is why it lands in the good range rather than the fair or excellent one.

Here is where 700 sits among the bands most Canadian lenders use. The exact cutoffs vary by lender and bureau, but this reflects the consensus from Equifax Canada and TransUnion Canada.

| Range | Label | Where 700 sits |

|---|---|---|

| 760 - 900 | Excellent | Above 700 |

| 725 - 759 | Very good | Above 700 |

| 660 - 724 | Good | 700 is here |

| 560 - 659 | Fair | Below 700 |

| 300 - 559 | Poor | Below 700 |

A 700 is comfortably inside "good" and only 25 points below "very good." For most borrowing decisions, lenders treat anyone in the good band as a prime, low-risk applicant. If you want the full breakdown of the bands, see what is a good credit score in Canada.

What does a 700 credit score get you in Canada?

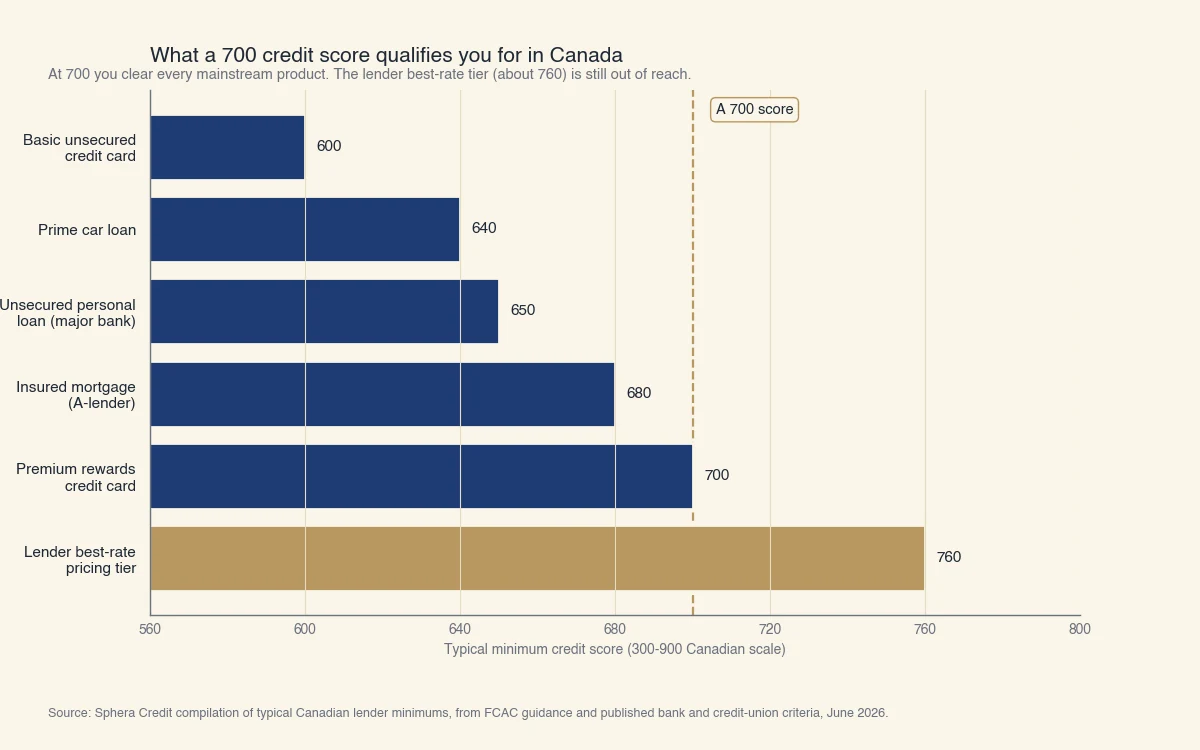

A 700 score qualifies you for essentially every mainstream Canadian credit product, including unsecured personal loans, prime car loans, most credit cards, and insured mortgages. The one thing it does not guarantee is the lowest advertised rate, which lenders reserve for their top pricing tier. The chart below shows the typical minimum score Canadian lenders look for by product, with a 700 marked.

Source: Sphera Credit compilation of typical Canadian lender minimums, from FCAC guidance and published bank and credit-union eligibility criteria, June 2026. Thresholds are representative and vary by lender.

The practical takeaway is the gap between 700 and the top tier. A 700 gets you approved; a 760 gets you the lowest price. On a small loan that gap is minor, but on a large or long loan it adds up.

The dollar cost of a 700 versus a higher score

Consider a $25,000 car loan over five years. A 700-tier borrower in mid-2026 might be offered around 6.99%, while a 760-plus borrower might be offered around 4.99%, given the rate environment set by the Bank of Canada policy rate of 2.25%. Running both through the standard amortization formula:

| Borrower | Representative APR | Monthly payment | Total interest |

|---|---|---|---|

| 700 (good) | 6.99% | about $495 | about $4,700 |

| 760+ (very good) | 4.99% | about $472 | about $3,300 |

The 700 borrower pays roughly $23 more a month and about $1,400 more in total interest on the same car. That is the real meaning of "good but not the best": you are approved at a fair price, with room to save more by climbing into the next band. (Figures are a Sphera Credit computation using the standard amortization formula with representative APRs; your actual rate depends on the lender, the product, and the rest of your application.)

What 700 means for different borrowers

The same number lands differently depending on your situation:

- First-time mortgage applicant. A 700 clears the roughly 680 minimum most banks look for on an insured mortgage, so approval is typically straightforward. You may not get the lowest posted rate, and lenders still check income, down payment, and your debt service ratios before approving.

- Car buyer. A 700 qualifies for prime auto financing rather than subprime, which is the difference between a single-digit rate and a low-teens one.

- New to credit. A 700 built on a thin file (one or two accounts, short history) can behave more cautiously in a lender's model than a 700 built on a long, varied history, even though the number is identical.

- Rebuilding after a setback. A 700 on the way up, with a recent late payment still on file, may face more manual review than a long-stable 700, because lenders read the trend, not just the snapshot.

Why do sources disagree on whether 700 is "good"?

Sources disagree because there is no single, official 700. Your number depends on which bureau pulled it and which score version they used, and the "good" and "fair" labels are lender conventions rather than regulated thresholds. Read two articles and you can get two different answers, which is confusing but explainable.

Three things drive the disagreement:

- Two bureaus, two files. Equifax Canada and TransUnion Canada each keep their own copy of your credit history, and lenders do not always report to both. Your Equifax and TransUnion scores can differ by 20 to 50 points because the underlying data differs (TransUnion Canada).

- Different score versions. Each bureau sells several score models, and a number is only meaningful next to the model that produced it. A 700 on one version is not strictly the same as a 700 on another.

- Bands are conventions, not law. No Canadian regulator defines where "good" begins. Most lenders place the good band at 660 to 724, which is why a 700 is almost universally called good, but a minority of sources draw the line differently, which is where the occasional "700 is fair" claim comes from. Treat 660 to 724 as the mainstream convention (FCAC).

The practical lesson: a 700 is a strong score on any mainstream Canadian scale, but the exact number you see can move depending on where you check it. If your score recently shifted without explanation, the cause is usually a data change at one bureau, not an error. See why your credit score goes down for the common triggers.

How does 700 compare to other scores?

A 700 is above the average Canadian score, which sits roughly between 660 and 675, and it is close enough to the "very good" band that small improvements move you up quickly. Here is how nearby numbers are generally read by Canadian lenders.

| Score | Band | What changes versus 700 |

|---|---|---|

| 600 | Fair | Below the good threshold; higher rates or alternative lenders likely |

| 700 | Good | Approved for mainstream products at fair rates |

| 720 | Good (top) | Stronger approvals; closer to best-rate pricing |

| 734 | Very good | Crosses into the very good band; better card and loan offers |

| 740 | Very good | Comfortably very good; most premium products open up |

| 750 | Very good | Typically clears best-rate mortgage and card tiers |

| 780 | Very good to excellent | Lowest advertised rates on nearly everything |

| 800 | Excellent | Top tier, though the gain over 760 is small in practice |

The pattern is steady: every step up the ladder lowers your borrowing cost a little, with the biggest single jump happening when you cross from "good" into "very good" around 725, because that is where many lenders set their best-rate cutoff. Moving from 700 to 725 is therefore often worth more in saved interest than moving from 760 to 800.

For context on where most people land, the average Canadian credit score is roughly 660 to 675 depending on the bureau and the year (Borrowell). A 700 puts you ahead of the typical Canadian. You can see the full picture in the average credit score in Canada.

How do you move a 700 score higher?

The fastest way to push a 700 into the very good band is to lower your credit utilization, keep every payment on time, and avoid new applications for several months. These three habits address the highest-weighted factors in the scoring models, and from a 700 starting point they can add 20 to 40 points within a few billing cycles.

- Lower utilization. Keeping your credit-card balances below 30% of your limit, and ideally below 10%, is the single fastest lever from a 700. If your $10,000 of total limits carries a $4,000 balance, paying it down toward $1,000 can move your score within one or two statement cycles.

- Protect payment history. Set automatic minimum payments on every account so a single missed due date cannot undo months of progress. Payment history is the largest factor in the score.

- Let your file age. Avoid opening several new accounts at once, and keep your oldest cards open. Closing an old card shortens your average account age and raises utilization, both of which can pull a 700 down.

From 700, reaching 760 typically takes 6 to 18 months of consistent activity, faster if high utilization is the main thing holding you back, slower if you are waiting for a negative item to age off. For the full playbook, see how to increase your credit score in Canada.

A 700 is a position of strength, not a problem to fix. It already opens the doors that matter. The reason to keep climbing is simple: every band you gain trims a little more off the price of every dollar you borrow.