How do you become an underwriter?

Two paths get you to a US underwriter desk: the long-form path is a bachelor's in finance or business plus an entry-level analyst role plus a certification, taking three to five years; the short-form mortgage path is a loan-processor role plus the NAMU Certified Mortgage Underwriter program, taking twelve to eighteen months. Most published career guides describe only the long-form path, but mortgage lenders routinely hire underwriters off the loan-processor bench without a four-year degree (NAMU).

An underwriter is the person who decides whether a lender or insurer takes on the risk of a particular borrower, policyholder, or security issuer. They do not sell the product. They apply documented rules to documented facts and write a defensible yes-or-no decision that the lender can defend in a CFPB exam or an investor audit (CFPB).

The role splits into three big specializations:

- Insurance underwriters evaluate applications for property, casualty, life, or health policies and set premiums and coverage limits. Around 127,000 work in the US as of 2024 (BLS).

- Mortgage and loan underwriters evaluate applications for home loans, auto loans, personal loans, and small-business credit. They live under the Fannie Mae Selling Guide, the Freddie Mac Single-Family Seller / Servicer Guide, or the FHA Single Family Housing Policy Handbook depending on the loan program.

- Securities underwriters work at investment banks pricing and placing new equity or debt issuances. This is the smallest of the three by headcount and the most credential-gated.

The rest of this guide focuses on insurance and mortgage underwriting, since that is where almost every entry-level seat sits.

Which underwriter path matches your starting point?

| Your starting point | Fastest realistic path | Time to signing authority |

|---|---|---|

| Bachelor's in finance or business, no industry experience | Junior underwriter or analyst at a P&C insurer; pursue AINS and CPCU | 3 - 5 years |

| Bachelor's in any field, willing to start in operations | Loan processor at a mortgage lender; pursue NAMU-CMU | 12 - 18 months |

| Associate's degree or high school plus 2 years in insurance customer service | Junior insurance underwriter trainee; pursue AINS | 2 - 4 years |

| Associate's degree or high school plus 2 years as a loan processor | Mortgage underwriter trainee; pursue NAMU-CMU | 12 - 18 months |

| Mid-career switch from accounting or banking | Credit analyst on a commercial lending desk | 1 - 2 years |

The mortgage path is shorter because the rulebook is published and finite. The Fannie Mae Selling Guide is a public document; the FHA Handbook is a public document; the underwriter's job is to apply them. A loan processor who already touches those rulebooks daily can move into the underwriter seat once they pass an internal scorecard and the NAMU certification.

What does an underwriter actually do?

An underwriter spends most of the day reviewing files: pulling credit reports, reading income documents, checking the appraisal or actuarial inputs, computing the qualifying ratios, clearing or adding conditions, and writing a documented decision. The role is heavily structured: every decision must cite the rule it applies. Notes on a mortgage file have to reference the program, the section, and the supporting document. Notes on an insurance file have to reference the rate manual, the actuarial table, and any binding authority.

A typical day on a US conforming-mortgage desk:

- Open eight to fifteen new or returning files in the lender's loan origination system.

- Run each through the relevant automated underwriting system (AUS) -- Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor -- and read the findings. Most underwriters spend a few minutes per file on this step (Fannie Mae, Freddie Mac).

- Verify that the documents in the file match what the AUS believed when it scored: income on pay stubs against the AUS-assumed income, debts on the credit report against the AUS-assumed debts, assets on bank statements against the AUS-assumed reserves.

- Add conditions for anything missing or inconsistent. A typical conditional approval has six to twelve conditions: a recent pay stub, an updated bank statement, a gift letter, hazard insurance, the appraisal, a verification of employment within ten days of closing.

- Clear conditions as the loan processor returns the requested documents.

- Issue the final decision: clear to close, declined with a HMDA reason code, or counter-offered with revised terms.

A typical day on an insurance underwriting desk follows the same shape with different inputs: instead of a credit report and an appraisal, the underwriter reads the application, the inspection report, the loss-history database, and the rate manual. The constants are the structure, the documentation discipline, and the requirement that every decision be reviewable.

What types of underwriting jobs exist in the US?

- Property and casualty insurance: the largest single bucket. Most P&C underwriters start as trainees at a regional or national carrier (Travelers, Chubb, Liberty Mutual, Berkshire affiliates).

- Life and health insurance: smaller. Requires more clinical knowledge for life and disability lines.

- Conforming mortgage: the biggest seat in mortgage lending. Files run through DU or LPA and conform to Fannie or Freddie rules.

- Government mortgage: FHA, VA, and USDA Rural. Higher documentation burden, lower minimum credit thresholds.

- Non-QM and jumbo mortgage: files outside the agency boxes. Higher pay, more judgment, more exception writing.

- Commercial credit: business loans, lines of credit, asset-based lending. More qualitative, more relationship-driven, often higher pay than residential.

- Securities: investment banking. Different skill stack -- modeling, valuation, capital markets -- and a separate credentialing path (Series 79, Series 24).

What education and certifications do you need?

The most common formal credential is a bachelor's in finance, business, accounting, or economics; the most valuable certifications are CPCU and AINS for insurance underwriting and NAMU-CMU for mortgage underwriting. Certifications are not legally required to be an underwriter in the US, but they materially raise compensation and are usually the gate to senior roles. The BLS reports a bachelor's as the typical entry-level credential, while noting that relevant work experience can substitute (BLS).

The credential stack by track:

| Track | Entry credential | Mid-career certification | Senior certification |

|---|---|---|---|

| P&C insurance | Bachelor's + AINS | CPCU | ARM, AU, CIC |

| Life and health | Bachelor's + ALMI | FLMI | FALU |

| Mortgage (residential) | NAMU-CMU | NAMU-CMMU | NAMU-CAMU |

| Mortgage (commercial / asset-based) | Internal lender training | Internal senior credit officer | Bank-specific signing authority |

| Securities | Bachelor's + Series 79 | Series 24 | Internal MD title |

The Chartered Property Casualty Underwriter (CPCU) designation from The Institutes is the gold standard in P&C insurance. It requires passing eight exams covering insurance principles, commercial underwriting, personal lines, ethics, and risk management. Most candidates complete it over two to four years while working full time (The Institutes).

The NAMU Certified Mortgage Underwriter (NAMU-CMU) is the most direct mortgage credential. NAMU's curriculum covers conforming, FHA, VA, USDA, non-QM, and jumbo underwriting. The certification is built around online coursework that most candidates complete in a few months alongside their day job (NAMU).

What skills matter more than the degree?

The credential gets you the interview. The skills get you signing authority:

- Document literacy. You will read pay stubs, W-2s, 1099s, K-1s, P&Ls, tax transcripts, bank statements, appraisal reports, and insurance binders every day. Speed and accuracy here are the single largest determinant of files-per-day throughput.

- Math fluency. Debt-to-income ratios, loan-to-value, qualifying income from variable comp, depreciation add-backs, residual income on VA loans. None of it is hard; the volume is what challenges most new underwriters.

- Rule-citation discipline. Every decision must cite the rule. New underwriters who write "approved, looks fine" instead of "approved per Fannie B3-3.1-09 with two-year average self-employed income" do not last.

- Written communication. A clean conditional-approval note tells the loan officer exactly what is missing and exactly how to satisfy it. Ambiguous condition language is the largest cause of file ping-pong and the second-largest cause of borrower frustration.

How do you become an underwriter with no experience?

The realistic entry-level seat is loan processor at a mortgage lender or customer service representative at a P&C insurer; both feed directly into a junior underwriter role within twelve to twenty-four months. Lender job postings for "loan processor" rarely require more than a high school diploma and basic computer literacy. Insurance carriers run formal trainee programs that hire bachelor's-degree candidates directly into a learning rotation.

The mortgage-side bench-to-underwriter pipeline:

- Months 0 - 3. Start as a loan processor or processor assistant. Learn the lender's LOS (Encompass, Empower, Byte). Read your first batch of FHA and conforming files alongside the senior processor.

- Months 3 - 9. Run an active pipeline of fifteen to thirty files at any given time. Order appraisals, request conditions from borrowers, follow up with insurance agents and title companies. Read every condition the underwriter writes on your files.

- Months 9 - 12. Pass the lender's internal scoring test, start the NAMU-CMU coursework, and pick up "underwriter assistant" tasks: pre-checking files before they hit the underwriter, clearing simple stipulations.

- Months 12 - 18. Earn the NAMU-CMU. Move into a junior underwriter seat with signing authority on conforming files up to a per-loan limit set by the lender. Continue under senior-underwriter QC review on every file for another three to six months.

The insurance-side trainee pipeline is similar but more structured. Most large carriers run formal underwriter-trainee programs that last six to twenty-four months and combine classroom training with rotations through claims, agency, and underwriting. The CPCU coursework typically starts during this period.

Can you become an underwriter without a degree?

Yes for mortgage and commercial credit roles; harder but not impossible for insurance. Mortgage lenders prioritize document literacy and program knowledge over the degree itself; a strong loan processor with two years of clean work and a NAMU-CMU certification is a competitive underwriter candidate at most US mortgage lenders. Insurance carriers tend to prefer the bachelor's because their underwriter-trainee programs are explicit pipeline hires from college recruiting cycles, but smaller regional carriers and independent agencies hire underwriters with associate's degrees plus operational experience.

How long does it take to become an underwriter and what does it pay?

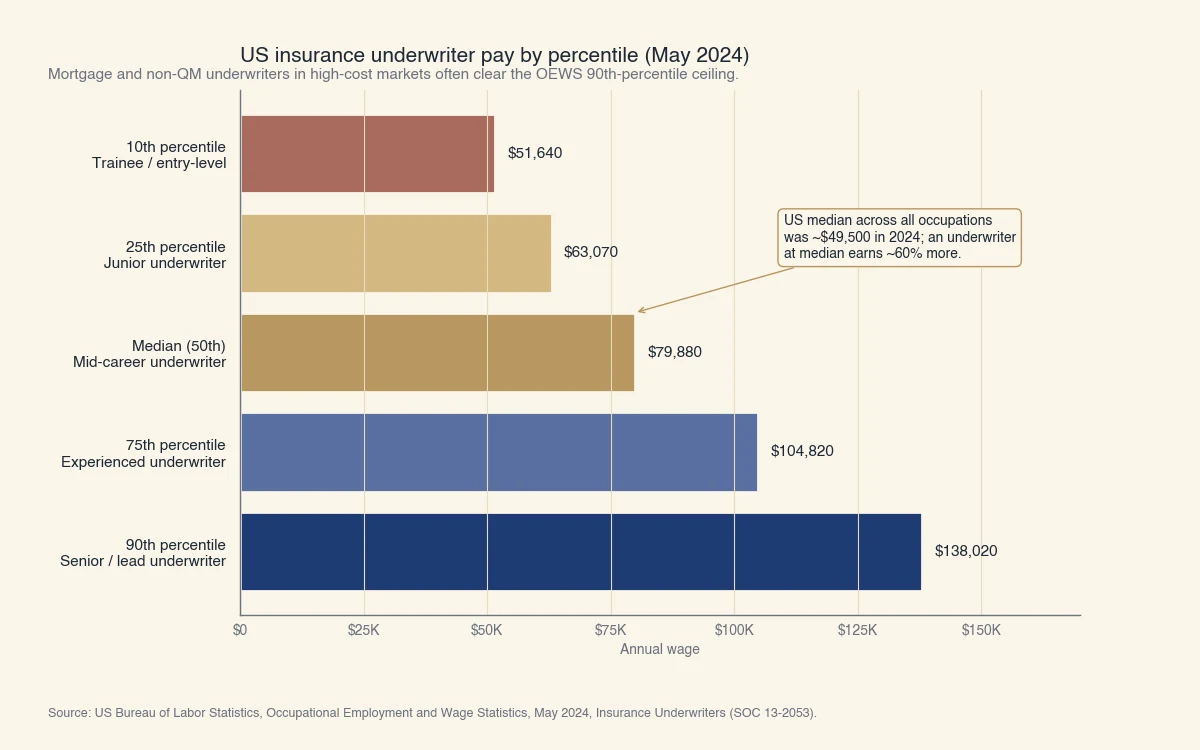

The full career path runs about seven to ten years from entry-level to senior underwriter; pay scales from roughly $51,640 at the 10th percentile to $138,020 at the 90th percentile based on the May 2024 BLS OEWS data for insurance underwriters. Mortgage underwriters in high-cost-of-living markets and with non-QM or jumbo experience routinely earn above the OEWS 90th percentile because the BLS code only tracks insurance underwriters explicitly (BLS OEWS).

Source: US Bureau of Labor Statistics, Occupational Employment and Wage Statistics, May 2024, Insurance Underwriters (SOC 13-2053).

The career-progression timeline that the chart maps to in practice:

| Years of experience | Typical title | Typical comp band (BLS OEWS percentile) | Signing authority |

|---|---|---|---|

| 0 - 1 | Loan processor / junior analyst / underwriter trainee | P10 to P25 ($51K - $63K) | None; supervised review only |

| 1 - 3 | Junior underwriter | P25 to P50 ($63K - $80K) | Conforming files up to a per-loan limit |

| 3 - 6 | Underwriter | P50 to P75 ($80K - $105K) | Conforming, FHA, VA, USDA; some non-QM |

| 6 - 10 | Senior underwriter | P75 to P90 ($105K - $138K) | Jumbo, non-QM, exception files |

| 10+ | Lead underwriter / chief credit officer | Above OEWS ceiling at most lenders | Full authority; QC and exception sign-off |

Three calibrations on the BLS numbers: the OEWS code is for insurance underwriters only, so mortgage and commercial salaries are not directly captured; the median is heavily location-dependent (a P50 underwriter in Des Moines is not paid the same as a P50 underwriter in San Francisco); and most published total comp figures exclude annual bonuses, which often add 10% to 25% on top of base at mortgage lenders.

How does pay change once you earn a certification?

Industry hiring surveys consistently show a 7% to 15% compensation premium for the CPCU on the insurance side and a similar premium for NAMU-CMMU on the mortgage side. The premium is larger at smaller lenders and carriers where the certification signals an externally verified skill bar; at the largest carriers and lenders, the credential is essentially required for promotion to senior, so it gates the higher tier rather than adding a premium on top of it.

Will AI and automated underwriting replace underwriters?

Automated underwriting systems already approve the straightforward files; what underwriters get paid for is the exceptions, conditions, and judgment that systems cannot resolve, and US adverse-action law requires a human decision-maker on declines. The BLS projects a 3% decline in insurance underwriter employment from 2024 to 2034 but still expects roughly 8,200 annual openings driven by replacement demand (BLS).

Three reasons the career is not disappearing the way generic "AI will replace X" articles imply:

- AUS systems have been deployed since the 1990s. Fannie Mae's Desktop Underwriter launched in 1995, Freddie Mac's predecessor to LPA in 1995, FHA's TOTAL Scorecard in 2004. The 3% projected decline reflects the steady automation of easy files over decades, not a recent shock.

- Adverse-action documentation is regulated. Under the Equal Credit Opportunity Act and Regulation B, a lender that declines an application must give the applicant a specific reason within 30 days, signed by a person, defensible in a fair-lending exam. CFPB guidance has consistently held that "the algorithm declined you" is not an acceptable adverse-action notice. A human underwriter has to own the decline (CFPB).

- The exception files do not shrink. Self-employed income, non-occupying co-borrowers, condotels, rural properties, gift funds with paper trails, credit events inside the look-back window: these are precisely the files the AUS cannot resolve. As AUS systems improve, exception files become a higher share of the underwriter's caseload, not a lower one.

The realistic 2026-and-beyond change is not "AI replaces underwriters" but "AI co-pilots make the underwriter's caseload bigger." Lenders deploying generative-AI assistants alongside DU or LPA report files-per-day throughput increases of roughly 20% to 40%; the underwriter still owns the decision, but spends less time gathering documents and more time on the judgment portion of the file.

What skills hedge against further automation?

The skills that are hardest for a system to absorb are also the ones that compound:

- Exception writing. Documenting a non-QM compensating factor or a manual FHA approval in language that survives investor audit. Junior underwriters cannot do this; senior underwriters charge for it.

- Adverse-action defensibility. Writing the decline reason in language that satisfies Regulation B, fair-lending exams, and the borrower's eventual appeal. This is a legal skill as much as a credit skill.

- Program breadth. The underwriter who can clean an FHA file, a VA file, a USDA file, and a non-QM file is more valuable than the underwriter who can only clean conforming.

- QC and exception oversight. Once you can underwrite, the higher-paid role is reviewing other underwriters' files. That career step does not automate, because someone has to sign the lender's quality reports.

For more on how underwriting decisions get made under modern guidelines, see what is underwriting and what is an underwriter in a mortgage loan. For where credit scores fit into the underwriter's checks on a home loan, see what credit score is needed to buy a house.