Educational only: please read first

The information below is for general educational purposes and is not financial advice, credit counselling advice, legal advice, or a recommendation to take any specific action. Credit building in Canada depends on proprietary scoring models held by Equifax Canada and TransUnion Canada, federal reporting standards, and provincial consumer-protection rules that vary across the country. How those rules apply to any individual depends on facts this article cannot know. For financial guidance, consult a licensed financial advisor or a non-profit credit counsellor. For legal questions about how a provincial statute applies to your situation, consult a lawyer licensed in your province.

How do you build a credit rating from scratch?

You build a credit rating by opening at least one credit account, using only a small part of its limit, and paying the full balance on time every month; once that account reports to Equifax Canada and TransUnion Canada for a few months, the bureaus have enough history to calculate a score. A credit rating (in Canada, the same thing as a credit score) is a three-digit number from 300 to 900 that lenders use to estimate how likely you are to repay borrowed money on time (FCAC).

Before you have any account, you are what lenders call credit invisible: there is no file for a bureau to score. A credit bureau (Equifax Canada and TransUnion Canada are the two national ones) collects reports from lenders about how you handle credit, then a scoring model turns that file into a number. No file means no number, so the first job is simply to get one account reporting.

The score itself comes from five factors. These weights come from the FICO methodology that the Canadian bureaus mirror closely, and Equifax Canada publishes the same categories (Equifax Canada):

- Payment history (about 35%) is whether you pay on time. It is the single largest factor, so one missed payment early on can undo months of building.

- Amounts owed, or utilization (about 30%) is how much of your available credit you use. Keeping the balance under 30% of the limit is the common guidance, and under 10% is better.

- Length of credit history (about 15%) is the average age of your accounts. This is why your first account matters for years: keeping it open lengthens your history.

- Credit mix (about 10%) is having more than one type of credit, such as a card plus an installment loan.

- New credit (about 10%) counts recent applications. Several applications in a short window can hold the score back.

The takeaway for someone starting from zero: you only need one account to become scoreable, but you need on-time payments and low utilization on that account for the number to grow.

How long does it take to build a credit score in Canada?

In Canada you usually need at least one open account that reports to a bureau for three to six months before a score can be generated, and reaching the "good" range of 660 or higher typically takes one to two years of on-time payments. Building credit is a slow process by design, because the models reward a track record, and a track record only exists after time has passed (FCAC).

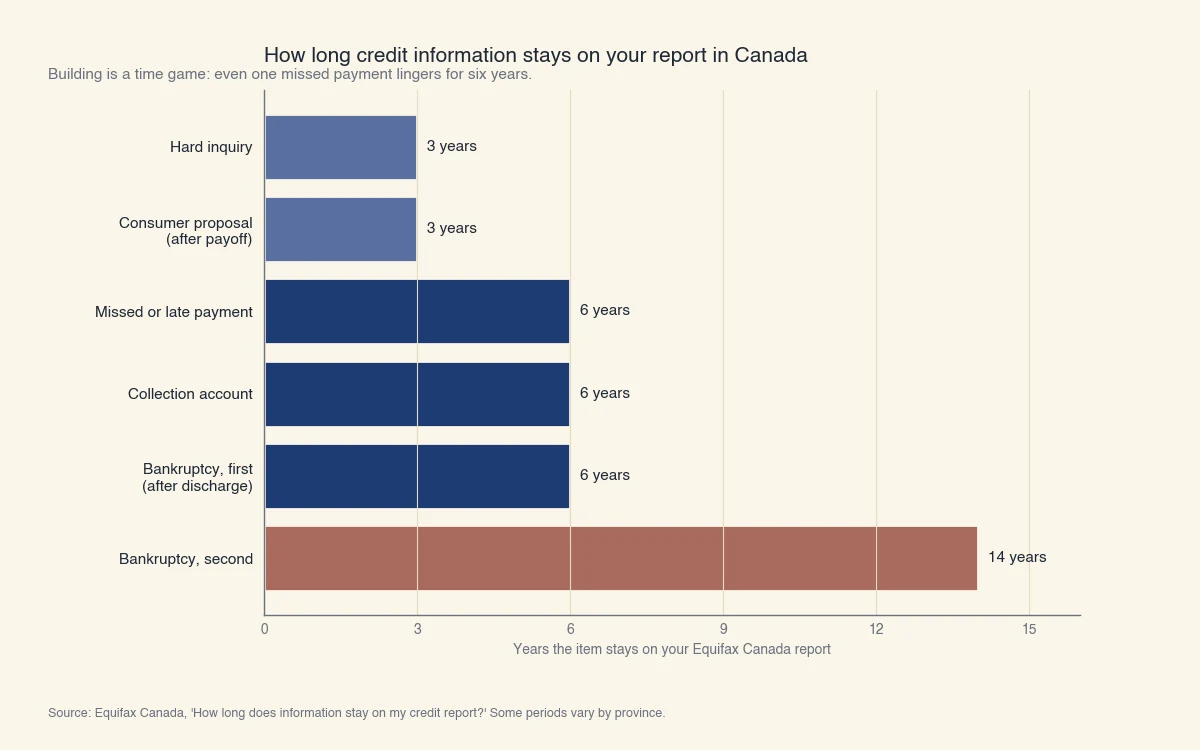

Two clocks run at the same time. The first is how long new positive history takes to build: a few months to become scoreable, then one to two years to reach a solid score. The second matters if you are rebuilding rather than starting fresh, because accurate negative marks stay on your file for years and cannot be removed early. Equifax Canada publishes exactly how long each kind of information lasts: a single missed payment stays six years from the date it was reported, a collection stays six years, and insolvency records stay longer still (Equifax Canada).

Source: Equifax Canada, "How long does information stay on my credit report?" Some periods vary by province.

The lesson for building and rebuilding is the same: start the positive history now, because time is the ingredient you cannot rush. This is also why the "newcomers start at 300" idea is wrong. A newcomer to Canada with no Canadian file has no score at all, because the bureaus do not import foreign credit history. A score of 300 would mean a long record of serious problems; no record simply means the model has nothing to work with yet. The fix is the same for a newcomer, a student, or anyone else with an empty file: open one reporting account and let time do the work.

What are the best tools to build credit in Canada?

The main tools to build credit in Canada are a secured credit card, a credit-builder or savings-secured loan, becoming an authorized user on someone else's card, and reporting rent or phone payments to the bureaus. Each one gets an account reporting to Equifax and TransUnion; they differ in cost and in how quickly they show up.

- A secured credit card requires a refundable cash deposit that usually becomes your credit limit. A $500 deposit gives a $500 limit, and the card reports to the bureaus exactly like a regular card. It is the most common first step because you control utilization directly.

- A credit-builder loan (also sold as a savings-secured loan) lends you a small amount that sits in a locked account while you make fixed monthly payments. Those installment payments report to the bureaus and add credit mix.

- Becoming an authorized user puts your name on a family member's existing card. Whether it helps depends on the issuer, because not every Canadian issuer reports authorized-user activity, and any missed payment by the primary cardholder can flow to your file too.

- Rent and phone reporting turns payments you already make into reported history, but only through a service that sends them to a bureau. Rent paid straight to a landlord is usually not reported on its own.

| Tool | Upfront cost | Reports to both bureaus | Typical time to first score | Best for |

|---|---|---|---|---|

| Secured credit card | Refundable deposit (often $200 to $500) | Usually yes | 3 to 6 months | Most people starting from zero |

| Credit-builder / savings-secured loan | Small locked payments | Usually yes | 3 to 6 months | Adding credit mix without a card |

| Authorized user on family card | None | Depends on the issuer | Varies | Young adults with a willing family member |

| Rent / phone reporting service | Low monthly fee | Depends on the service | Varies | Renters with steady on-time payments |

What building credit looks like month by month

A realistic build from zero uses a small secured card, kept well under its limit and paid off every cycle. Suppose you open a secured card with a $500 deposit, giving a $500 limit. You put about $75 of regular spending on it each month, which is 15% utilization, and you pay the statement in full before the due date.

- Months 1 to 3: the account starts reporting. You are still likely credit invisible or barely scoreable.

- Months 3 to 6: a score usually appears once the bureau has enough history.

- Months 12 to 24: with unbroken on-time payments and low utilization, the score commonly reaches the good range of 660 or higher.

One trap to plan around: bureaus often capture your balance on the statement date, not the due date. If you charge $450 on that $500 card and pay it in full a few days later, the bureau can still record 90% utilization for that month. Paying before the statement closes, or keeping the balance small all month, keeps the reported utilization low.

Where are you starting from?

The fastest first move depends on why you have no credit rating yet, so match the tool to your situation rather than copying a generic tip list. Four starting points cover most people who land on this page.

| Your situation | Best first product | Why it fits | Realistic timeline |

|---|---|---|---|

| Student or young adult, no file yet | Student credit card, or authorized user on a parent's card | Low limits and easy approval; a parent's long history can help if the issuer reports it | Score in 3 to 6 months; good range in 1 to 2 years |

| Newcomer to Canada | Secured credit card tied to your SIN | Foreign history does not transfer, so you start a fresh Canadian file | Score in 3 to 6 months once reporting begins |

| Self-employed or gig worker, thin file | Secured card plus a small credit-builder loan | Adds both revolving and installment history for a stronger mix | Score in 3 to 6 months; mix builds over the first year |

| Rebuilding after missed payments or a consumer proposal | Secured card, low utilization, patience | Old items age off over 6 to 7 years while new positive history accumulates | Gradual; visible gains in 12 months, full recovery takes years |

Rebuilding deserves one extra note. A consumer proposal (a formal debt settlement under the Bankruptcy and Insolvency Act) and most missed-payment records stay on your Canadian credit report for up to six to seven years. You cannot erase them early, but you can start building positive history right away so that when the old items age off, a healthy file is already in place.

Which credit-building mistakes should you avoid?

The most common credit-building mistakes are carrying a balance on purpose, applying for several products at once, and closing your first card once you qualify for a better one. Much of the advice that circulates about building credit is either a myth or actively harmful:

- "You must carry a balance to build credit." False. Paying in full every month builds history just as well and costs you no interest. The bureaus reward on-time payment, not unpaid debt.

- "You need to go into debt to build credit." False. Small purchases paid off in full report the same activity as large balances. Building credit is about consistent reporting, not borrowing heavily.

- Applying for several cards or loans at once. Each application can add a hard inquiry, and a cluster of them in a short window can hold your new score back. Space out applications.

- Closing your first card after you qualify for a nicer one. Closing it shortens your average account age and cuts your available credit, which usually lowers the score. Keep the first account open and active.

- Believing that checking your score hurts it. Checking your own score is a soft inquiry with no effect. Check it for free and dispute any errors you find with the bureau directly (FCAC).

Building a credit rating is slow and unglamorous, and that is the honest answer: one reporting account, low utilization, on-time payments, and time. Thin files are exactly where automated scorecards tend to say "no," because there is not enough history to score. At Sphera Credit, we build lending technology that helps lenders assess borrowers accurately and explain their decisions, including people whose files are still thin. The point is not a faster yes; it is a fair and well-reasoned one, so that a short credit history is understood in context rather than treated as an automatic rejection.