What is the highest credit score possible?

The highest credit score possible is 850 on the base FICO and VantageScore models nearly everyone sees, and 900 on the industry-specific FICO scores that some auto and card lenders pull. The number you check in a banking app almost always runs on a 300 to 850 scale, so for practical purposes 850 is the perfect score (myFICO, CFPB).

A credit score is a three-digit number lenders use to estimate how likely you are to repay borrowed money on time. The word "possible" in this question has two honest answers, because the ceiling depends on which model is scoring you:

| Scoring model | Where you see it | Range | Highest score |

|---|---|---|---|

| FICO Score 8 / 9 / 10 | Bank apps, free monitoring | 300 - 850 | 850 |

| VantageScore 3.0 / 4.0 | Credit Karma, many free tools | 300 - 850 | 850 |

| FICO Auto Score 8 | Auto-lender pulls | 250 - 900 | 900 |

| FICO Bankcard Score 8 | Card-issuer pulls | 250 - 900 | 900 |

So the short answer is 850 for the score you can see and track yourself, and 900 as the absolute maximum on the industry scores working behind the scenes. For the full model-by-model ceiling breakdown, including the retired VantageScore scale that once reached 990, see the highest credit score you can have. The more useful questions for most readers are how rare a perfect score really is, who reaches it, and whether it is realistic for you.

How rare is a perfect credit score?

A perfect 850 is rare: about 1.76% of US consumers held a FICO Score of 850 as of March 2025, the highest share since 2009, according to Experian. That works out to roughly one in every 57 scored adults (Experian).

Rarity is the part most articles skip, and it reframes the whole question. "Excellent" credit is common; a literally perfect number is not. Roughly 23% of consumers with a credit score sit at 800 or above (Experian), yet fewer than 2% reach the ceiling. The gap between "top band" and "perfect" is where years of extra discipline go.

The perfect-score share has also been climbing. Experian notes the 1.76% figure is the highest since 2009, a rebound driven by low delinquency rates and years of consumers paying down revolving balances. That trend matters for context: a perfect score is more attainable today than it was a decade ago, but it is still something fewer than one in 50 scored adults holds at any given moment. Reaching it is a long game measured in years of clean history, not weeks of optimization.

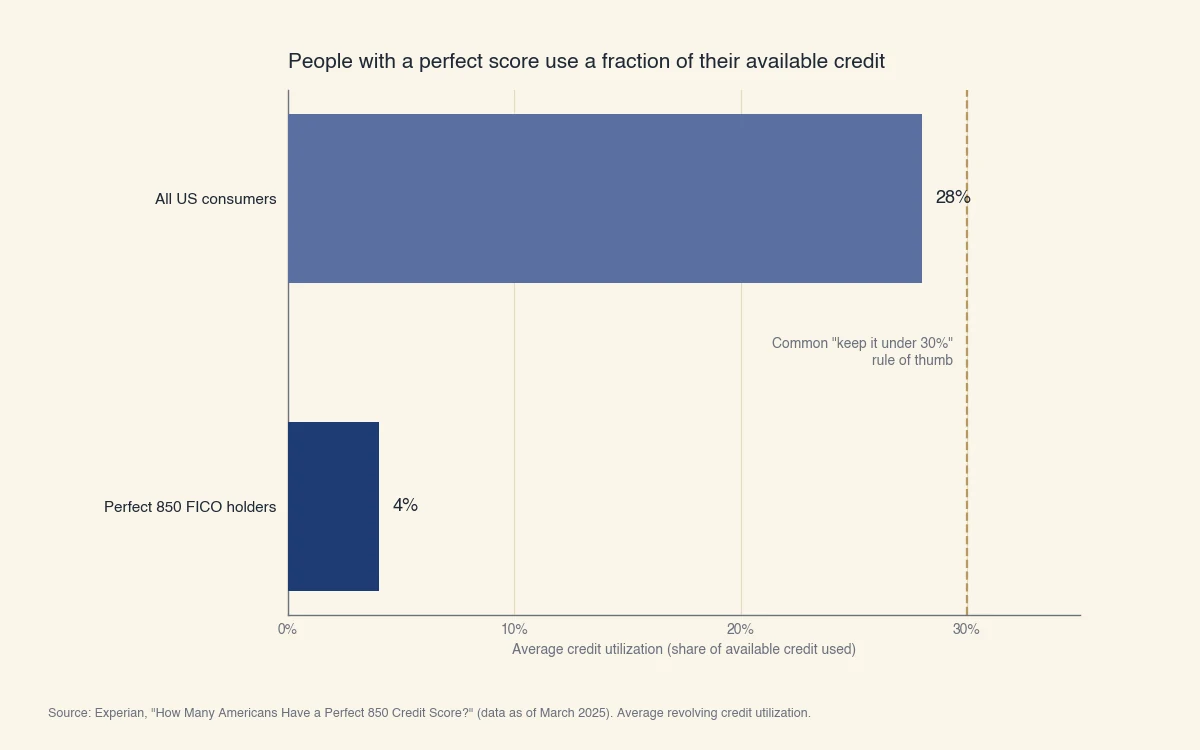

One behavior separates the perfect-score group from everyone else more than any other: how little of their available credit they use. Credit utilization is the share of your credit limits you are carrying as a balance, and people at 850 keep it far below the common "under 30%" rule of thumb.

Source: Experian, "How Many Americans Have a Perfect 850 Credit Score?" (data as of March 2025). Average revolving credit utilization for FICO 850 holders vs. all US consumers.

Perfection is also a moving target. An 850 is a snapshot, not a permanent rank. A new account, a higher statement balance, or one missed payment can knock a perfect score down, and many people cross 850 one month and slip back the next. The ceiling is reachable; staying pinned to it is the rare part.

Who actually reaches the highest credit score?

People with a perfect 850 share a clear profile: very low utilization, several long-held accounts, a spotless payment record, and no derogatory marks. Experian's March 2025 data shows the perfect-score group looks measurably different from the average consumer (Experian).

| Metric | Perfect 850 holders | All US consumers |

|---|---|---|

| Average credit utilization | 4% | 28% |

| Average number of credit cards | 5.7 | 3.7 |

| Average credit card balance | $3,028 | $6,618 |

| Average delinquent accounts | 0 | 1.6 |

Two details stand out. First, 850 scorers carry more cards than average, not fewer, which shows that having several accounts is not the problem; carrying high balances on them is. Second, their utilization sits near 4%, not "under 30%." They are not hugging the rule-of-thumb line, they are nowhere near it.

Geography tracks with financial stability rather than any credit trick. The West (2.1%) and Northeast (2.01%) have the highest share of perfect scores, ahead of the Midwest (1.83%) and South (1.33%). At the metro level, Boulder, Colorado leads at 3.25%, followed by the Silicon Valley metros of San Jose (3.18%) and San Francisco (3.12%) (Experian). Higher incomes and older, more established credit files cluster in these areas, which is what the score is really measuring.

Is a perfect credit score possible for you?

Whether 850 is realistically within reach depends less on effort and more on how old and clean your credit file is. Because length of credit history is 15% of a FICO score and the top band rewards decades of accounts, the honest answer varies by borrower profile (myFICO).

- Thin or young file (history under 5 years). Reaching 850 soon is unlikely, because the score has not yet credited you for a long track record. A realistic near-term target is the high-700s. On-time payments and utilization under 10% will get you into the excellent band; time does the rest.

- Thick, long-standing file (10+ years, no missed payments). A perfect score is genuinely reachable. Keep utilization near or below 5%, avoid new applications before a big loan, and let your oldest accounts stay open. Many people in this group touch 850 without trying.

- Recovering from a late payment. A single 30-day late payment resets progress toward the top band. Lenders weight a recent missed payment heavily for 12 to 24 months, and the record stays on your report for up to seven years. There is no way to speed this up beyond consistent on-time payments and time.

The five factors that decide where you land are the same for everyone: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%). For a step-by-step routine that moves a score fastest, see how to raise your credit score fast. If your scores differ across apps and you are not sure which "highest" applies, whether a FICO score is the same as a credit score explains why.

Is chasing the highest possible score worth it?

For almost everyone, no: the best interest rates arrive well before 850, so the final points buy nothing. Most lenders quote their top pricing to borrowers in the high-700s, which means a 760 to 800 score and a perfect 850 usually earn the identical rate, monthly payment, and lifetime interest (Experian).

The practical target is not the maximum. It is the lowest score that still reaches the top pricing tier, which is roughly 760 to 780 for most mortgage and loan pricing. We walk through the exact dollar math on a $400,000 mortgage, showing why a 780 and an 850 cost the same to borrow, in is the highest credit score worth chasing.

There is one good reason to aim higher anyway: a perfect score is a useful personal benchmark. If tracking the number keeps you disciplined about paying in full and keeping balances low, the habit is worth far more than the last 70 points. The score is a signal of that discipline, not the reward itself. At Sphera Credit, we build credit-decisioning tools for lenders precisely because a single number never tells the whole story of a borrower, and the same is true when you look at your own.