What is the highest credit score?

The highest credit score in Canada is 900, the top of the 300 to 900 range used by both Equifax and TransUnion consumer scores. A credit score is a three-digit number that lenders use to estimate how likely you are to repay borrowed money on time, and 900 is the theoretical ceiling on the Canadian bureau scales (Equifax Canada, FCAC).

That ceiling is mostly theoretical. Almost no one reaches 900, and you do not need to. A score is a moving number that updates every time your credit report changes, so hitting the exact maximum and holding it is nearly impossible. What matters far more is which lending tier you fall into, and the top tier begins well below 900.

Here is where the Canadian bands sit for most lenders:

| Range | Label | What it means for you |

|---|---|---|

| 760 - 900 | Excellent | Best advertised rates; approval is straightforward |

| 725 - 759 | Very good | Most prime products available |

| 660 - 724 | Good | Mainstream qualification range |

| 560 - 659 | Fair | Limited prime options; alternative lenders likely |

| 300 - 559 | Poor | Secured or subprime products only |

Notice that "excellent" starts at 760 and runs all the way to 900. To a lender, a 765 and a 900 sit in the same box. That single fact reshapes the real question behind "what is the highest credit score," which is usually "how high do I actually need to go?"

Is the highest credit score 900 or 850?

Both 900 and 850 are correct, because Canada has two different maximums depending on which score is being used. The consumer scores you see for free top out at 900, while many lenders pull a FICO-based score that tops out at 850. Seeing both numbers is the single most common source of confusion, and no one is wrong.

The free score in your banking app or on a service like Borrowell is usually the Equifax Risk Score or the TransUnion CreditVision score, both built on a 300 to 900 scale. When you actually apply for a mortgage, car loan, or credit card, the lender may instead order a FICO score, which Fair Isaac builds on a 300 to 850 scale from the same credit-report data (Fair Isaac). Same file, different model, different maximum.

| Score you might see | Provider | Scale | Maximum | Where you see it |

|---|---|---|---|---|

| Equifax Risk Score | Equifax Canada | 300 - 900 | 900 | Free apps, Borrowell, direct from Equifax |

| TransUnion CreditVision | TransUnion Canada | 300 - 900 | 900 | Free apps, Credit Karma, direct from TransUnion |

| FICO Score | Fair Isaac (via a bureau) | 300 - 850 | 850 | Pulled by many lenders at application |

This is why the number in your app and the number a lender quotes can differ by 20 to 60 points even though nothing in your history changed. The bureaus and Fair Isaac each chose their own scale and never standardized a single ceiling. For a deeper US and Canada comparison of the two maximums, see what is the max credit score. If you want to know whether the Canadian 900 is ever reached at all, see is a 900 credit score possible.

How rare is a 900 credit score in Canada?

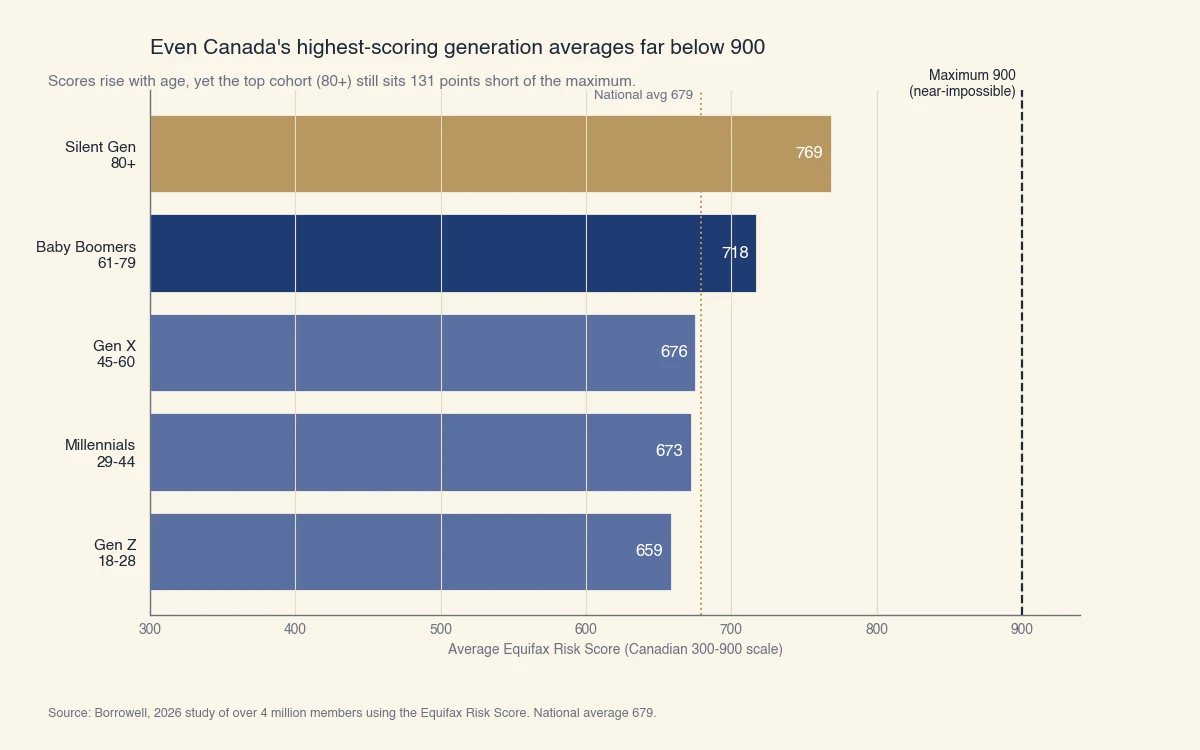

A 900 is extraordinarily rare, and even the highest-scoring group of Canadians averages far below it. According to Borrowell data drawn from more than 4 million members using the Equifax Risk Score, the average Canadian credit score is 679, and adults aged 80 and over, the top-scoring cohort, average just 769 (Borrowell).

Scores climb with age because length of credit history counts for roughly 15% of a score, and older Canadians have simply had more decades to build a clean record. Yet even that lifetime of history only lifts the average to 769, which is 131 points short of the maximum.

Source: Borrowell, 2026 study of over 4 million members using the Equifax Risk Score.

The takeaway is not that Canadians have poor credit. It is that the top of the scale is built to be nearly untouchable. A model that let large numbers of people reach 900 would lose its ability to separate the very best files from the merely excellent ones. The maximum exists as a boundary, not as a realistic target.

What separates a very high score from a perfect one?

Not behaviour, mostly data depth and timing. A borrower in the low 800s already pays every bill on time and keeps balances low. Reaching the last stretch toward 900 typically requires:

- A credit history measured in decades, not years.

- Zero late payments on any account across the full reporting window.

- Credit utilization, the share of your available credit you are using, under 10% and often under 5% on the day the score is generated.

- A healthy mix of revolving credit (credit cards) and installment credit (loans with fixed payments).

- Almost no new applications in the past year or two.

Every one of those factors has to line up at the same moment the bureau calculates the score. That is why disciplined borrowers often plateau in the low-to-mid 800s rather than touching the ceiling.

Is a perfect credit score worth chasing?

For almost everyone, chasing a perfect 900 is not worth it, because lenders stop rewarding higher scores once you reach the excellent tier around 760. The common belief that a bigger number always unlocks a better deal is the most expensive myth about credit scores, and it is wrong in a specific, measurable way.

Canadian lenders sort applicants into pricing tiers rather than pricing each point individually. Clear the top tier and you receive the best rate the lender offers, whether your score is 765 or 900. The extra points are real, but they buy nothing.

Consider two borrowers applying for the same mortgage:

- Borrower A has a score of 765. She lands in the lender's top tier and receives the best posted rate.

- Borrower B has a score of 850. He also lands in the top tier and receives the same best posted rate.

Borrower B spent years earning 85 additional points, and on this mortgage they save him nothing. His extra effort produced a better-looking number, not a better loan. This is why the practical ceiling for a Canadian borrower is closer to 760 than to 900.

It also matters because a score is only one input. Lenders assess the whole file: income, employment stability, existing debt, and the ratios between them. This is exactly where Sphera Credit focuses, helping lenders read the full picture of a borrower accurately rather than reducing a person to the last few points of a score. When a borrower sits just outside a tier or just outside the usual credit box, the accurate read is what protects both the borrower and the lender, not a hunt for a perfect number.

There is one honest exception. If the score itself keeps you motivated to stay disciplined, treating it as a long-term game is harmless and even useful. Just do not expect the jump from 800 to 900 to save you money.

How do you reach the highest credit score?

Reaching the top of the range takes a long, clean, low-utilization file built over many years, with the five scoring factors near their best at the same time. There is no shortcut and no product you can buy to get there faster (Equifax Canada, TransUnion Canada).

The realistic path looks like this:

- Years 1 to 2. Open a starter card or a credit-builder product and pay every bill on time. Most new files reach 660 to 700 in this window.

- Years 3 to 5. Add a second credit product to build mix, and keep utilization under 30% on every card. Scores commonly reach 720 to 760.

- Years 6 to 10. Hold the same accounts, push utilization under 10%, and avoid applications outside genuine need. Scores often reach 780 to 820.

- Years 10 and beyond. A long history compounds. With utilization under 5%, no new accounts, and zero late payments, scores can reach the mid-800s and, rarely, approach 900.

A single missed payment resets the clock on several factors. A hard inquiry, the credit check a lender runs when you apply, trims a few points temporarily, and a 30-day late payment can cost far more and stays on your report for six to seven years. For the full mechanics of how the number is built, see how is credit rating calculated. For faster, practical gains rather than a run at the ceiling, see how to increase your credit score.

What does not help you climb

A few widespread myths to drop:

- Carrying a small balance to "show activity." Paying your statement in full does not hurt your score, and carrying a balance raises utilization. Pay in full.

- Closing old credit cards. Closing your oldest card lowers your average account age and cuts your available credit, which pushes utilization up. Both hurt.

- Checking your own score often. Viewing your score is a soft inquiry with zero impact. Only lender hard inquiries cost points.

- Paying for credit repair. These services cannot do anything you cannot do yourself for free, and both the FCAC and consumer advocates caution against them (FCAC).

The number is a signal, not the goal. Aim for the excellent band, keep your habits steady, and let the score take care of itself.