How do you raise your credit score fast?

The fastest ways to raise your credit score are disputing genuine errors on your credit report and lowering your credit card utilization, because both can update your score within a single statement cycle. Everything else, from on-time payment streaks to a longer credit history, helps over months rather than days. Speed depends on the lever you pull, so the goal is to start with the moves that report soonest and carry the most weight.

Your score is built from five factors. Payment history is the largest at 35% of a FICO Score, followed by amounts owed at 30%, length of credit history at 15%, credit mix at 10%, and new credit at 10% (myFICO). The two factors you can change quickly are amounts owed (your utilization) and any inaccurate data dragging down your payment history.

Here is how the common levers compare on speed, impact, and effort:

| Lever | Typical time to show up | Potential impact | Effort |

|---|---|---|---|

| Dispute a real report error | Up to 30 days (bureau must investigate) | High when the error is significant | Low |

| Pay down credit card balances | Next statement cycle (about 30 days) | High | Medium |

| Request a credit limit increase | 1 statement cycle | Medium | Low |

| Become an authorized user | 1 to 2 cycles | Medium | Low |

| Report rent and utility payments | 1 to 2 cycles | Low to medium | Low |

| Bring past-due accounts current | 1 to 2 cycles | High over time | Medium |

| Open a secured card or builder loan | 2 to 6 months | Medium over time | Medium |

Credit utilization is the share of your available credit you are using, measured both per card and across all cards. A credit report error is any inaccurate account, balance, or late mark that does not belong to you or is reported incorrectly. Start with these two because they move the needle fastest.

Which fast lever should you pull first?

Pull the lever that matches your situation: dispute first if you find an error, pay down balances if your utilization is high, and add positive history if your file is thin. There is no single fastest move for everyone, so match the action to what is actually holding your score back.

Pull your reports for free from all three bureaus at AnnualCreditReport.com, then work down this list:

- You spot an error (wrong balance, account that is not yours, a late mark you paid on time): Dispute it first. The Federal Trade Commission found that one in five consumers had an error on at least one of their three credit reports, and about 5% had errors serious enough to raise their borrowing costs (FTC). File the dispute with the bureau; it must investigate, usually within 30 days (CFPB).

- Your cards are above 30% utilization: Pay them down, starting with the card closest to its limit, because per-card utilization matters alongside your overall ratio.

- Your utilization is fine but you cannot pay more right now: Ask each issuer for a credit limit increase. A higher limit with the same balance lowers utilization without spending a dollar.

- You have a thin file or no recent positive history: Become an authorized user on a responsible person's old, low-balance card, or start reporting rent and utility payments.

- You have a past-due account: Bring it current immediately. A payment that is fewer than 30 days late often has not been reported yet, so acting now can keep it off your report entirely.

How much does paying down your balance actually move your score?

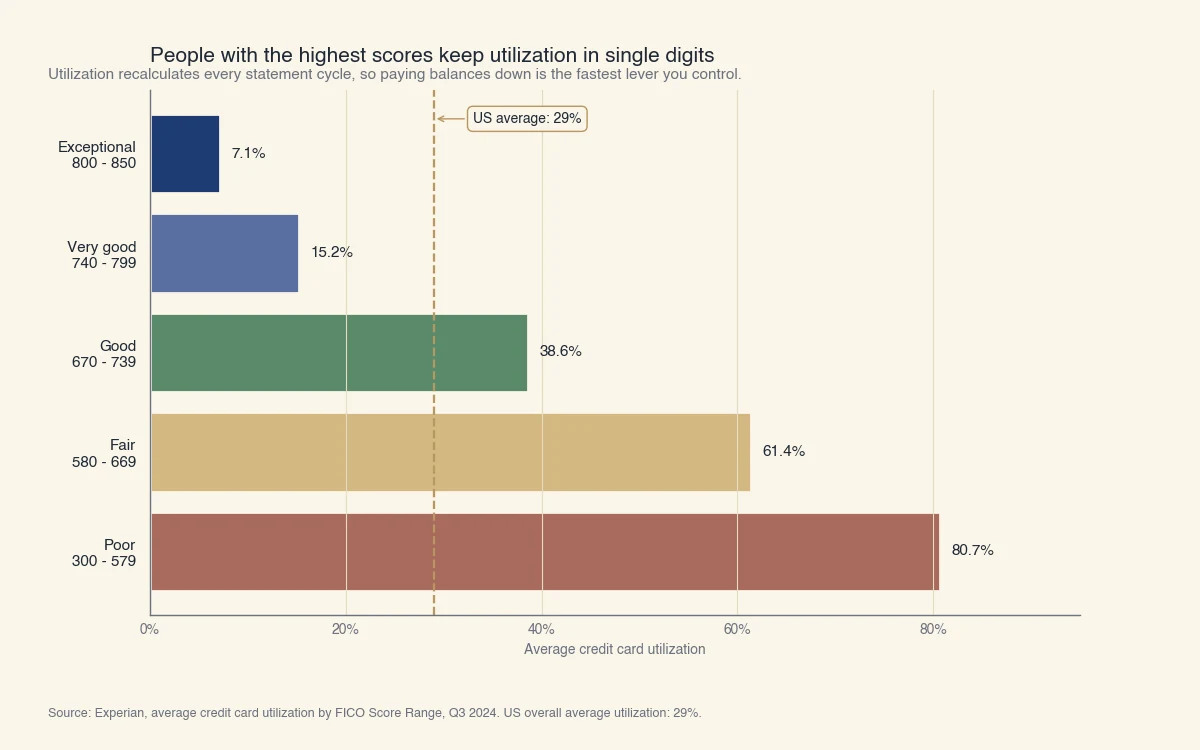

Cutting utilization is the fastest high-impact lever you control, because it recalculates every statement cycle and the score difference between high and low utilization is large. People with exceptional scores average about 7% utilization, while those with poor scores average above 80% (Experian). You cannot buy years of history overnight, but you can change your utilization before your next statement closes.

Source: Experian, average credit card utilization by FICO Score Range, Q3 2024. US overall average utilization: 29%.

Two worked examples show how this plays out.

Example 1: paying the balance down. Say you hold three cards with a combined limit of $12,000 and a total balance of $6,000. Your overall utilization is 50%, which sits in territory that holds scores down. Pay $3,600 toward the cards, prioritizing the one closest to its limit, and your balance drops to $2,400, or 20% utilization. Once those lower balances report at each card's statement date, your score can climb. A move from above 30% to around 20% commonly adds 20 points or more, though the exact gain depends on the rest of your file.

Example 2: raising the limit instead. Suppose you owe $2,000 on a card with a $5,000 limit, which is 40% utilization. You cannot pay it down this month. You ask the issuer to raise your limit to $10,000 and they agree. Your balance has not changed, but your utilization just fell to 20% because the denominator doubled. The score effect is similar to paying the balance down, achieved without spending anything. Request the increase as a soft-pull where possible so you avoid a hard inquiry.

The key is timing. Utilization is read from the balance your card reports, usually on the statement date, not the due date. Pay before the statement closes and the lower number is what the bureau sees.

What can you realistically expect in 30, 60, and 90 days?

A realistic fast result is 20 to 50 points over 30 to 90 days, not the 100-point overnight jump that viral posts promise. The average US FICO Score is about 715 (Experian), and most people raising a score from fair to good are working within that band, where steady moves add up quickly.

- Within 30 days: A removed error and lower utilization can both show up. This is where the largest fast gains live.

- 30 to 60 days: Authorized-user history and reported rent or utility payments begin to register. A credit limit increase has cycled through.

- 60 to 90 days: A second and third month of on-time payments start to build a visible pattern, and your earlier utilization drop is now well established.

Beyond 90 days, the slower factors take over: length of history, a healthy credit mix, and the steady fading of old negative marks. Negative items stay on your report for seven years from the missed payment, but their weight shrinks over time, so a two-year-old late payment hurts far less than a recent one.

Myths about raising your credit score fast

Most "fast credit" tricks online either do nothing or repackage utilization timing as a secret, so it is worth naming the common myths before you waste effort on them.

- The "15/3 payment trick" is not a secret hack. Making two payments before your statement date simply lowers the balance your card reports, which is ordinary utilization timing. It works because of utilization, not because of any special rule. You get the same effect by paying down before the statement closes.

- You do not need to carry a small balance to build credit. FICO does not reward you for carrying debt. Paying your statement in full every month still reports positive payment history and keeps utilization low. Carrying a balance only adds interest cost.

- Paying an old collection does not always cause an instant jump. Newer models such as FICO 9 and VantageScore 4.0 ignore paid collections, but older FICO versions still used in many mortgage decisions may not raise your score when you pay. Paying still reduces legal risk, so weigh the goal before assuming a score boost.

- Closing an old, unused card usually hurts, not helps. Closing a card removes its available credit, which raises your overall utilization, and over time shortens your average account age. Keep old no-fee cards open and active with a small recurring charge.

- Checking your own score never lowers it. Reviewing your own credit is a soft inquiry with zero score impact, so monitor as often as you like.

Raising a score fast is really about sequencing: fix what is wrong, lower what you owe, and let the slower factors compound. The borrowers who gain the most in 90 days are the ones who start with utilization and errors rather than chasing tricks.