What credit rating do you need for a mortgage in Canada?

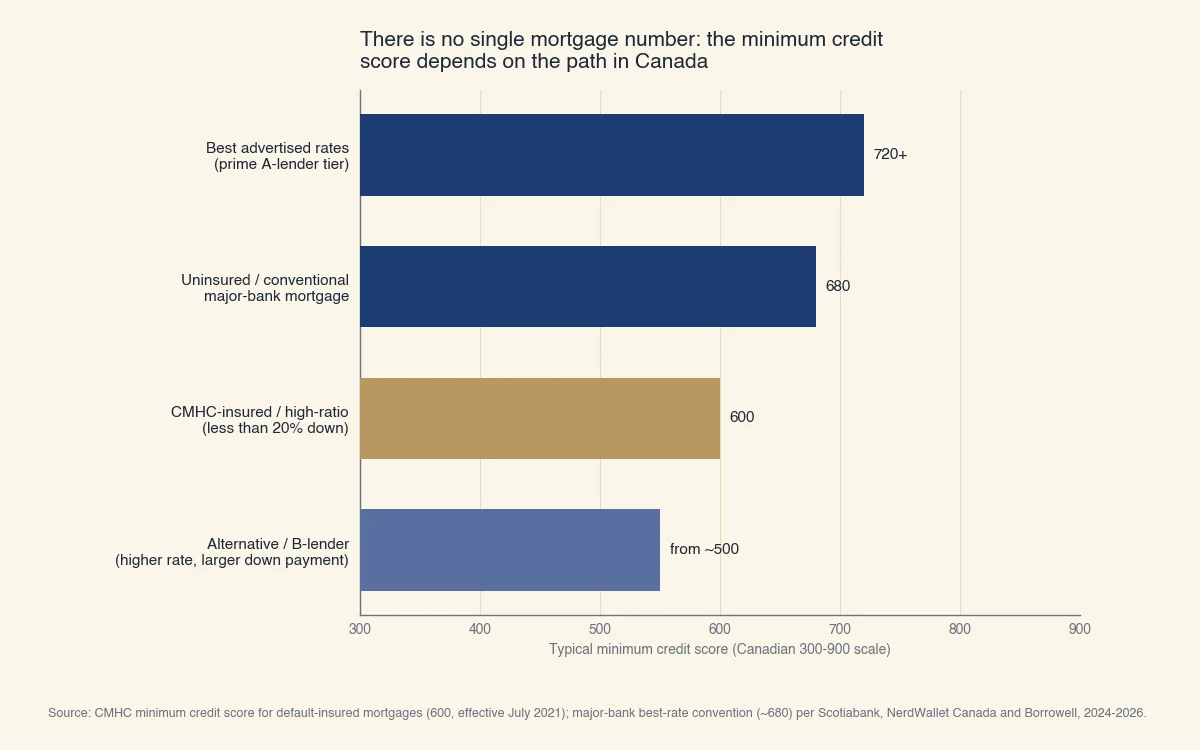

Most major Canadian banks want a credit score of about 680 for their best mortgage rates, but you can qualify for a default-insured mortgage with a score as low as 600, and B-lenders approve borrowers below 600 at a higher cost. There is no single legal minimum. The number you need depends on which mortgage path you take (FCAC).

Your credit rating is a snapshot of how reliably you have repaid past debt, expressed in Canada as a three-digit score from 300 to 900. Lenders read it to decide whether to approve you and what rate to charge. Because a mortgage is the largest and longest loan most people ever take, lenders hold it to a higher standard than a credit card or car loan.

Here is the practical breakdown by path:

Source: CMHC minimum credit score for default-insured mortgages (600, effective July 2021); major-bank best-rate convention (~680) per Scotiabank, NerdWallet Canada and Borrowell, 2024-2026.

- 720 and up: the tier where the best advertised prime rates typically open up.

- 680: the common floor for an uninsured (conventional) mortgage at a major bank.

- 600: the minimum credit score for a default-insured mortgage, the kind you need when your down payment is under 20%. The Canada Mortgage and Housing Corporation lowered this floor to 600 (from 680) in July 2021 (CMHC).

- Below 600: possible through alternative or B-lenders and private lenders, but expect a higher interest rate, larger down payment, and extra fees.

A default-insured mortgage (also called a high-ratio mortgage) is one where you put down less than 20% and the loan is backed by mortgage default insurance. That insurance is what lets the 600 floor exist. A conventional mortgage is one with 20% or more down and no default insurance, which is why banks apply their own, stricter 680 standard.

Your score is only part of the decision. Lenders also weigh your income, down payment, and debt-service ratios, and every insured mortgage must pass the federal mortgage stress test, which checks that you could afford payments at a higher qualifying rate (FCAC).

Credit rating vs credit score: what Canadian lenders actually read

In Canada, "credit rating" means two things: the 300-to-900 score, and the R-scale rating attached to each individual account on your credit report. Lenders read both, and a strong score can still be undercut by a poor R-scale rating on even one account. This is the detail most mortgage guides skip, and it matters because you searched for "credit rating," not just "credit score."

The R-scale rates how you have handled each revolving account (the "R" is for revolving, such as a credit card or line of credit). Installment loans use an equivalent "I" scale. The number runs from 1 (best) to 9 (worst) (Equifax Canada):

| Rating | What it means |

|---|---|

| R1 | Pays within 30 days of billing, as agreed |

| R2 | Pays in 30 to 60 days; one payment past due |

| R3 | Pays in 60 to 90 days; two payments past due |

| R4 | Pays in 90 to 120 days; three payments past due |

| R5 | Pays in 120+ days but the account is not yet a bad debt |

| R7 | Paying through a consolidation order, consumer proposal, or similar arrangement |

| R9 | Bad debt: placed for collection, or included in a bankruptcy |

An account marked R1 helps you. An R7 signals you are repaying under a formal arrangement such as a consumer proposal, and an R9 is the most damaging mark, standing for a written-off debt or bankruptcy. A single R7 or R9 can push a mortgage application to an alternative lender even if your overall score still looks acceptable. If that is your situation, our guide on whether you can get a mortgage with an R7 credit rating walks through the options.

The three-digit score, by contrast, blends your whole file into one number. Equifax Canada and TransUnion build it from five factors: payment history, how much of your available credit you use, the length of your history, your credit mix, and recent applications (Equifax Canada). We break the formula down in how credit ratings are calculated.

The takeaway: when a lender says "your credit rating," they may mean your score, your R-scale marks, or both. Pull your full report, not just the number, before you apply.

What a lower credit rating actually costs you

A lower credit rating rarely blocks a mortgage outright, but it raises your interest rate, and on a mortgage that difference compounds into tens of thousands of dollars. The score is better understood as a price than as a pass-or-fail gate.

Consider a $500,000 mortgage amortized over 25 years, using Canadian semi-annual compounding. Watch how the monthly payment and lifetime interest move as the credit tier drops:

| Credit tier | Illustrative rate | Monthly payment | Total interest over 25 years |

|---|---|---|---|

| Excellent (720+) | 4.8% | $2,851 | $355,408 |

| Good (660-719) | 5.3% | $2,994 | $398,200 |

| Fair / alternative (600-659) | 6.5% | $3,349 | $504,736 |

Moving from the excellent tier to the fair tier adds about $498 to every monthly payment and roughly $149,000 in total interest across the life of the loan. That gap is often larger than the down payment itself. The rates above are illustrative spreads for comparison, not quotes; actual rates move with the market and the lender.

This is why waiting a few months to lift your score from 650 to 680 before you apply can pay for itself many times over. A small change in the rating changes the rate, and a small change in the rate changes the payment for 25 years.

One nuance worth stating plainly: a higher score does not guarantee approval, and a lower score does not guarantee rejection. A 720 score paired with a high debt load can be declined, while a 620 score with a large down payment and steady income can be approved through an insured or alternative channel. Lenders read the whole file.

What credit rating do you need for a car loan or credit card?

A mortgage sets the highest credit bar of the three: car loans are usually attainable from the mid-600s, and many credit cards approve well below that, including secured cards that require almost no score at all. The larger and longer the loan, the higher the rating a lender expects.

| Product | Typical minimum credit rating | Notes |

|---|---|---|

| Mortgage (best bank rates) | ~680 | ~600 with default insurance; below 600 via B-lenders |

| Car loan | ~660 | Subprime auto lenders approve lower, at higher rates |

| Credit card (mainstream) | ~660 | Entry-level and student cards approve lower |

| Secured credit card | No minimum | You post a deposit; used to build or rebuild credit |

The reason a mortgage is stricter comes down to size and duration. A car loan might be $30,000 over five years; a mortgage is often $500,000 over 25. A default costs the lender far more, so they demand a stronger repayment record. That is also why the same score can get you a car loan easily but leave a mortgage priced at an alternative-lender rate.

If your rating is not there yet, a secured card or a car loan repaid on time is a common way to build the R1 history that a mortgage lender wants to see. Our guide on what credit score you need for a car covers the auto side in detail.

How to check and improve your credit rating before you apply

Check your credit rating for free a few months before you apply, then focus on the two factors that move it fastest: paying every bill on time and keeping your credit-card balances low. Payment history and credit utilization together drive most of your score (FCAC).

You can see your score and full report at no cost through:

- Borrowell and Credit Karma, which pull soft data that does not affect your score.

- Several Canadian bank apps, which now show a free TransUnion or Equifax score.

- Equifax Canada and TransUnion directly, for the complete report including your R-scale marks.

To lift your rating before a mortgage application:

- Pay on time, every time. A single missed payment can drop your score by 60 to 100 points and lands an R2 or worse on the account.

- Keep utilization under 30%. If your card limit is $10,000, keep the balance under $3,000. Under 10% is better still.

- Avoid new applications in the months before you apply. Each hard inquiry can shave a few points, and a cluster of them looks like distress to a lender.

- Keep old accounts open. Length of history helps, so do not close your oldest card right before applying.

- Fix errors. Dispute any account you do not recognize; a wrongly reported late payment or R-mark is worth correcting before a lender sees it.

Building credit from a thin file takes longer. If you are starting out or new to Canada, our guide on how to build a credit rating lays out the realistic timeline.

Before you sit down with a lender, it is worth understanding what happens next. If underwriting feels like a black box, should you be worried about underwriting explains how a lender actually reviews your file.

How Sphera Credit thinks about credit ratings near the line

Sphera Credit builds AI underwriting tools for lenders, and the borrowers we focus on are the ones whose credit rating sits just outside a standard cutoff, where a single number decides too much. The 640 score that a rigid rule would auto-decline is exactly the file that deserves a closer read. A number on its own is a blunt instrument. Read alongside income, the R-scale detail, and the reason behind a past late payment, the same file often tells a very different story. Our work is about reading that fuller picture accurately, so decisions rest on evidence rather than a single cutoff.