Educational only: please read first

The information below is for general educational purposes and is not financial advice, credit counselling advice, or legal advice. How a student loan affects any one person depends on the loan type, the province, the lender, and proprietary scoring models held by Equifax Canada and TransUnion Canada. The mechanics described here are drawn from public sources; the worked-example numbers are illustrative and rounded. For guidance on your situation, consult a licensed financial advisor or a non-profit credit counsellor.

Does a student loan affect your credit rating?

Yes. A student loan affects your credit rating because it reports to Equifax Canada and TransUnion Canada as an installment account, so on-time payments build your score and missed payments lower it. A credit rating (in Canada, the same thing as a credit score) is a three-digit number from 300 to 900 that lenders use to estimate how likely you are to repay borrowed money on time (FCAC).

The direction of the effect is entirely in your hands. The loan itself is neutral: it is a line on your credit report. What the scoring model reacts to is your behaviour on that line. Pay every installment on time and the loan quietly strengthens your file for years. Miss payments and the same account becomes one of the most damaging marks you can carry.

An installment account is a debt you repay in fixed scheduled payments, such as a student loan, a car loan, or a mortgage. This is different from revolving credit like a credit card, where the balance moves up and down. The distinction matters because a student loan adds installment history to your file, which contributes to the credit-mix part of your score.

How a student loan actually moves your credit score

A student loan moves your score through the same five factors that drive every Canadian credit score, and payment history, worth about 35% of the total, is the one it touches most. The five factors are payment history (about 35%), amounts owed (about 30%), length of credit history (about 15%), credit mix (about 10%), and new credit (about 10%). You can see the full breakdown in how a credit rating is calculated.

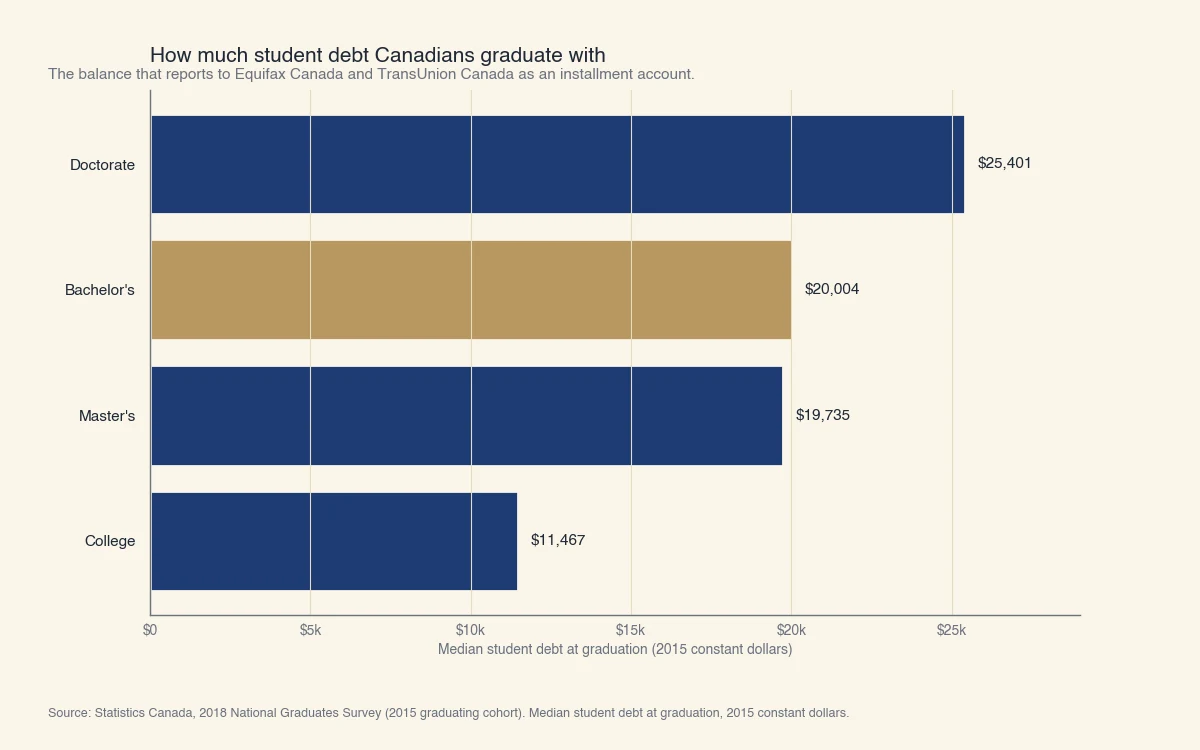

Here is what that looks like with real numbers. A typical bachelor's graduate in Canada leaves school with a median government student loan around $20,000 (Statistics Canada). The chart below shows how that balance compares across credential levels.

Source: Statistics Canada, 2018 National Graduates Survey (2015 graduating cohort), median student debt at graduation in 2015 constant dollars.

What happens when you pay on time

Every on-time payment on a student loan adds a positive record to the largest part of your score, and the balance falling over time is treated as a healthy sign. Say your $20,000 federal loan is on a standard 10-year schedule. Because Canada Student Loans stopped charging interest on the federal portion on April 1, 2023, a payment of roughly $170 a month goes almost entirely to principal (Government of Canada).

- After the six-month non-repayment period ends, the loan enters repayment and starts reporting (NSLSC).

- Each month you pay on time adds one more on-time mark to your payment history, the factor worth about 35%.

- The shrinking balance sits in "amounts owed," and a falling installment balance is read favourably.

- Because it is an installment account, the loan also improves your credit mix if the rest of your file is credit cards.

The result over a year of clean payments is a stronger, deeper file, which is exactly what a future car or mortgage lender wants to see.

What happens when you miss payments

Missed payments turn the same loan into a serious drag on your score, and after 270 days of non-payment a federal loan goes into default, which is one of the worst marks a Canadian credit file can carry. The damage escalates in stages:

- A payment 30 or more days late can be reported to Equifax Canada and TransUnion Canada. Late payments hit the payment-history factor, the single most influential one (Equifax Canada).

- 60 and 90 days late add heavier marks. The later and more frequent the misses, the larger the score drop.

- At 270 days (nine months) past due, the federal loan is in default and is sent to the Canada Revenue Agency or your province for collection (Government of Canada).

- In collection, the CRA can offset your tax refunds, garnish wages, and block further student aid. The account can be rated R9, the worst rating on the Canadian scale.

- The negative marks stay about six years from the date they are reported before they fall off your Equifax report (Equifax Canada).

This is why the honest answer to "does a student loan hurt my credit" is: only if you let it go unpaid. If money gets tight, acting before day 270 is what protects your score.

Government or private: which student loan touches your credit?

Both government and private student loans report to the credit bureaus once you are repaying them, but they differ sharply in how you get them and how default works. A government student loan comes through the Canada Student Financial Assistance Program and provincial programs such as OSAP in Ontario. A private student loan is usually a student line of credit from a bank or credit union.

| Feature | Government student loan | Private loan or student line of credit |

|---|---|---|

| Credit check to qualify | Generally none | Yes, a hard inquiry |

| Interest on the federal portion | None since April 1, 2023 | Set by the lender |

| Reports to Equifax and TransUnion | Yes, once in repayment | Yes |

| Default point | 270 days (nine months) past due | At the lender's discretion |

| Help if you cannot pay | Repayment Assistance Plan | Depends on the lender |

One provincial note: Quebec, the Northwest Territories, and Nunavut run their own student aid programs instead of the federal Canada Student Financial Assistance Program, so the interest and default rules can differ there (Government of Canada).

Three things about student loans and credit that surprise people

Most guidance repeats "pay on time, it helps," but three facts about Canadian student loans catch borrowers off guard. Each one changes how you should think about the loan on your file.

- Applying for a government student loan does not create a hard inquiry. Federal and provincial student aid is assessed on financial need, not credit, so most students face no credit check at all. Since Budget 2023, even mature students aged 22 or older no longer need credit screening to qualify for federal grants and loans for the first time (Government of Canada). The application itself cannot lower your score.

- An interest-free loan still builds credit. Canada Student Loans have charged no interest on the federal portion since April 1, 2023, which saves the average borrower about $520 a year. The loan still reports as an installment account, so your on-time payments still build payment history even though the loan costs you nothing in interest.

- Paying a student loan off early can briefly nudge your score down. Closing the installment account removes it from your credit mix and, over time, lowers your average account age. The dip is usually small and temporary, and paying off debt is still the right financial call. It is just worth knowing the score can wobble for a cycle or two, so you are not alarmed by it. This is the same mechanism behind why a credit score can drop right after you do something responsible.

What to do if you cannot repay your student loan

If you cannot make a payment, act before the 270-day default line, because the tools that protect your credit only work while the loan is still in good standing. The federal Repayment Assistance Plan can reduce or pause your payments based on income, and enrolling keeps the loan out of default (Government of Canada).

- Contact the NSLSC early. Repayment Assistance and revised terms are available while you are current, not after collection starts.

- Keep other accounts current. Even if the loan is a problem, protecting your credit cards and other payments limits the damage to your overall score.

- Check your report for errors. If a payment is reported wrong, dispute it directly with Equifax Canada or TransUnion Canada, and learn how to check your credit score for free first.

A student loan is one of the first real credit accounts many Canadians ever hold, which means it is often where a thin file starts to grow into a real one. That is also where automated lending decisions tend to be least accurate, because a short history gives a scorecard little to work with. At Sphera Credit, we build lending technology that helps lenders read files like these in context and explain their decisions, so a borrower with a young but well-managed student loan is understood fairly rather than rejected by default. The goal is an accurate decision, not a rushed one.