What is the highest credit score you can have?

The highest credit score you can have is 850 on the base FICO Score and VantageScore models, or 900 on industry-specific FICO scores like the FICO Auto Score and FICO Bankcard Score. Which ceiling applies depends entirely on which model is reading your file (myFICO).

The number you see in your banking app or a free monitoring service almost always comes from a base model that tops out at 850. The score a lender pulls when you actually apply for a car loan or a credit card may come from an industry-specific model that runs to 900. Same credit history, different ceiling. That is why the honest answer to "what is the highest score" is a question back: which score are you looking at?

For the companion question of the US 850 ceiling versus the Canadian 900 scale, see what is the max credit score. This page covers the full range from floor to ceiling and whether reaching the top is worth the effort.

What is the highest credit score on each scoring model?

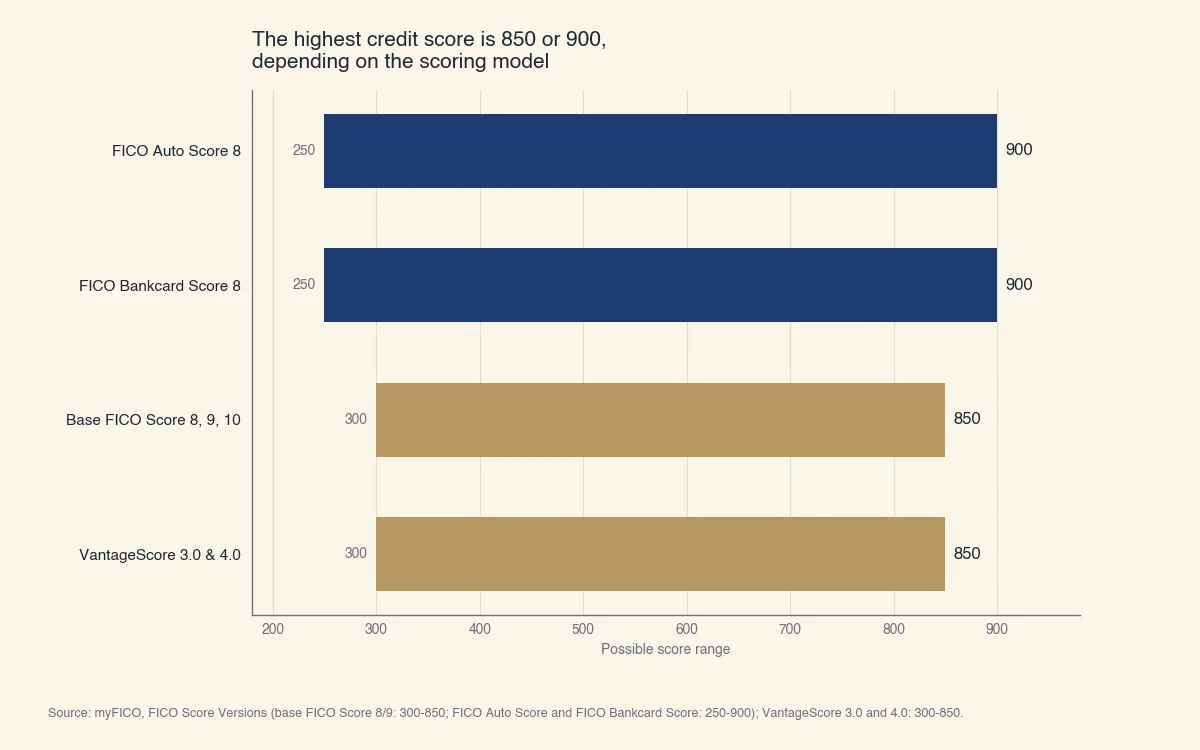

On the two models almost everyone sees, base FICO and VantageScore, the highest score is 850. On the industry-specific FICO Auto Score 8 and FICO Bankcard Score 8, the highest score is 900. The 50-point gap is not a measure of a better borrower. It is just a wider scale that those two models use to spread out applicants for a single product type (myFICO).

| Scoring model | Where you see it | Range | Highest score |

|---|---|---|---|

| FICO Score 8 / 9 / 10 (base) | Bank apps, free monitoring | 300 - 850 | 850 |

| VantageScore 3.0 / 4.0 | Credit Karma, many free tools | 300 - 850 | 850 |

| FICO Auto Score 8 | Auto-lender pulls | 250 - 900 | 900 |

| FICO Bankcard Score 8 | Card-issuer pulls | 250 - 900 | 900 |

| VantageScore 1.0 / 2.0 (retired) | No longer used | 501 - 990 | 990 |

Source: myFICO, FICO Score Versions (base FICO Score 8/9: 300-850; FICO Auto Score and FICO Bankcard Score: 250-900); VantageScore 3.0 and 4.0: 300-850.

Why people think scores go above 850

Two reasons. First, the industry-specific FICO models genuinely reach 900, so a lender quoting your "auto score" can name a number above 850. Second, the original VantageScore models (versions 1.0 and 2.0, now retired) used a 501 to 990 scale (VantageScore). Anyone who remembers a credit score in the 900s from a decade ago saw a real VantageScore number, just from a model no bureau uses today. Current VantageScore 3.0 and 4.0 both moved to 300 to 850 to match FICO.

What is the lowest credit score you can have?

The lowest credit score you can have is 300 on the base FICO and VantageScore models, or 250 on the industry-specific FICO Auto and Bankcard scores. Almost nobody actually sits at the absolute floor, because reaching 300 requires a deeply damaged file rather than simply having no credit (myFICO).

There is an important distinction the ceiling question hides. A very low score and no score are not the same thing:

- A low score (300 to 579) means you have a credit file, and the data in it is poor: missed payments, collections, high balances, or a bankruptcy.

- No score at all means there is not enough information to generate one. The Consumer Financial Protection Bureau estimated that about 26 million U.S. adults are "credit invisible," with no record at any of the three nationwide bureaus, and another 19 million have files too thin or stale to score (CFPB).

Being credit invisible is not the floor of the scale. It is being off the scale entirely, which often hurts a thin-file or new-to-credit borrower more than a measurable low score would. For why a brand-new file does not begin at 300, see what does your credit score start at.

How many people reach the highest credit score?

About 1.76% of U.S. consumers held a perfect 850 FICO Score as of March 2025, the highest share since 2009, and roughly 22.8% sit in the 800 to 850 "exceptional" band. The average FICO Score is far lower, at 713 in 2025 (Experian).

So a perfect score is rare, but the top band is not. Nearly one in four scoreable Americans already qualifies as "exceptional" without ever touching 850. The model is calibrated so that small, normal imperfections hold most disciplined borrowers just short of the ceiling: one slightly higher utilization month, one account opened in the past year, or one card under three years old is enough to keep an otherwise flawless file at 830 instead of 850 (Experian).

| Score band | Label | Share of U.S. consumers |

|---|---|---|

| 800 - 850 | Exceptional | 22.8% |

| 740 - 799 | Very good | about 23% |

| 670 - 739 | Good | about 21% |

| 580 - 669 | Fair | about 17% |

| 300 - 579 | Poor | about 16% |

For a deeper look at whether the very top of a 900-point scale is even reachable, see is a 900 credit score possible.

Is the highest credit score worth chasing?

No. On the myFICO Loan Savings Calculator the top mortgage pricing tier starts at 780, which means a borrower at 780 and a borrower at a perfect 850 are quoted the identical rate, the identical monthly payment, and the identical lifetime interest. Every dollar of benefit your score can buy is already captured before you reach the ceiling (myFICO).

Here is the mechanism in concrete terms. The calculator sorts borrowers into pricing tiers and assigns one rate per tier, using national-average rate data from Curinos for an 80% loan-to-value, owner-occupied single-family home:

- The highest tier is 780 and above. Scores from 780 to 850 all land here and receive the same rate.

- The next tier down is 760 to 779, priced slightly higher.

- Tiers continue downward at 740 to 759, 720 to 739, 700 to 719, and so on.

So on a $400,000 30-year fixed mortgage, moving from 760 to 780 is the last time a higher score saves you money. After 780, the lender stops rewarding the number. Going from 780 to a perfect 850 costs the same to borrow, which means the years of extra discipline required to chase the final 70 points return exactly zero on your mortgage. The same tier logic applies to auto loans and credit cards: once you clear the top pricing band, the rate stops improving.

This is why the practical target is not the highest possible score. It is the lowest score that still reaches the top pricing tier, which is 780 for most mortgage pricing and around 760 for many other products.

How do you reach the highest credit score range?

Reaching the 780-plus top tier, and eventually the 800s, comes down to the same five factors that drive every FICO and VantageScore: payment history, amounts owed, length of history, credit mix, and new credit. None of them respond to tricks. They respond to time and consistency.

The short version of what actually moves you into the top range:

- Pay every bill on time, every time. Payment history is the single largest factor. One 30-day late payment can cost 60 to 110 points and stays on file for up to seven years.

- Keep credit utilization low. Under 30% is safe, under 10% is ideal, and the borrowers who reach 850 typically report under 5% when the score is pulled.

- Let your accounts age. Do not close your oldest card. Average account age is a factor you can only build by waiting.

- Keep a healthy mix. A blend of revolving credit (cards) and installment credit (a loan) helps, but never open an account you do not need just to add mix.

- Apply for new credit rarely. Each application adds a hard inquiry and lowers your average account age.

For the full step-by-step path and the common myths to avoid, see how to fix your credit score and how to boost your credit score. The reassuring part is that you do not need to run this all the way to 850. Reaching the top pricing tier is enough to borrow at the best rates available, and that tier is well within reach of any borrower with a clean, patient file.

At Sphera Credit we build credit-decisioning systems that read the whole file, not just the headline number, because two borrowers with the same score rarely carry the same risk. The score is a useful signal. It is not the entire story, and chasing its last few points is rarely where your effort pays off.