What is Canada's credit rating?

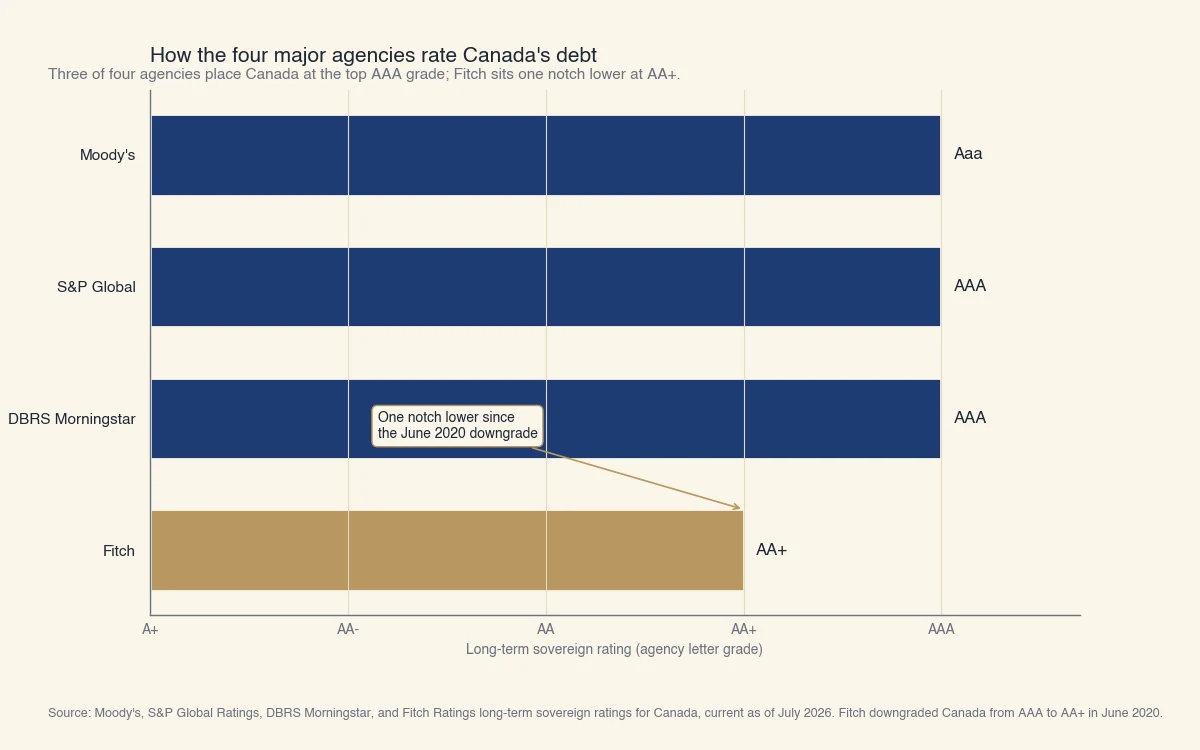

Canada holds a AAA sovereign credit rating from Moody's, S&P Global, and DBRS Morningstar, and a slightly lower AA+ rating from Fitch, all with a stable outlook as of 2026. A sovereign credit rating is a letter grade that independent agencies assign to a country to measure how likely its government is to repay borrowed money on time. AAA is the highest grade available; it means the agency sees almost no risk that Canada will miss a payment on its debt (S&P Global Ratings).

The phrase "Canada's credit rating" carries two different meanings, and searchers use it for both. Most of the time it refers to the country's sovereign rating, the subject of this section. It can also mean your own personal credit rating as a Canadian consumer, which is a completely separate number set by Equifax and TransUnion. The next section explains the difference so you land in the right place.

Here is where each of the four major agencies rates Canada today:

| Agency | Rating | Outlook | Notes |

|---|---|---|---|

| Moody's | Aaa | Stable | Top grade, held since the early 2000s |

| S&P Global | AAA | Stable | Top grade, paired with A-1+ short-term |

| DBRS Morningstar | AAA | Stable | Canadian-based agency, top grade |

| Fitch | AA+ | Stable | One notch below top since June 2020 |

Source: Moody's, S&P Global Ratings, DBRS Morningstar, and Fitch Ratings sovereign ratings for Canada, as of July 2026.

A country does not have a single credit rating. Each agency runs its own model and reaches its own conclusion, which is why Canada sits at the top grade for three agencies and one notch below for Fitch. The letter grades map roughly across agencies: Moody's writes the top grade as "Aaa" while S&P, Fitch, and DBRS write it as "AAA", and everything from AAA down to BBB- counts as investment grade (low credit risk), while ratings below that are speculative grade (Fitch Ratings).

Sovereign credit rating vs your personal credit rating in Canada

Canada's sovereign rating and your personal credit rating are two unrelated systems: the sovereign rating grades the federal government's debt on a AAA-to-D letter scale, while your personal rating grades your own borrowing history on a 300-to-900 score and an R1-to-R9 scale. They share the words "credit rating" and nothing else. A change to Canada's AAA rating does not change your personal score, and improving your own credit has no bearing on the country's rating.

| Sovereign credit rating | Personal credit rating | |

|---|---|---|

| Who is rated | The Government of Canada | You, as an individual |

| Who assigns it | Moody's, S&P, Fitch, DBRS | Equifax and TransUnion |

| Scale used | AAA down to D | 300-900 score; R1-R9 rating |

| What it measures | The government's ability to repay its debt | Your history of repaying credit |

| Who relies on it | Bond investors, pension funds, governments | Lenders, landlords, some employers |

If you searched for "Canada's credit rating" but meant your own file, the number you want is the personal credit score, a three-digit number from 300 to 900 that Equifax and TransUnion calculate from your credit report (FCAC). Our guide on how credit ratings are calculated in Canada walks through the five factors that move that score, and what counts as a good credit score explains the bands lenders use.

What is an R7 or R9 credit rating in Canada?

The R-scale is a separate personal-credit code that runs from R1 to R9 and describes how you are handling a specific account. It appears on your credit report next to each trade line (Equifax Canada):

- R1 is the best rating: you pay the account within 30 days of billing, or as agreed.

- R7 means you are making regular payments through a special arrangement, such as a consumer proposal, an orderly payment of debts, or a debt management program, rather than paying the original creditor on the original terms.

- R9 is the worst rating: the debt has been sent to collections, you cannot be located, or you have declared bankruptcy.

The "R" originally stood for revolving credit, but the scale now applies broadly. None of these codes relate to Canada's sovereign rating. If you are weighing what an R7 means for a home purchase, see can you get a mortgage with an R7 credit rating.

Why does Canada hold a AAA rating?

Canada keeps a top-tier rating because it combines a manageable net debt load, a credible central bank, a strong banking sector, and stable institutions, even though its gross debt looks high at first glance. The most common misconception is that Canada's rating rests on low borrowing. It does not. Gross government debt in Canada is high relative to other AAA countries, but much of that reflects pre-funding future pension obligations. Once you net out the large financial and pension assets the government holds, net public debt is far lower and sits in the middle of the AAA pack (RBC Economics).

Three other pillars support the rating:

- A resilient financial sector. Canada ranks at the top of AAA economies on the IMF's Financial Development Index, and its major banks held tier-one capital ratios above 15% in 2022, well above regulatory minimums.

- Monetary credibility. The Bank of Canada's aggressive rate-hiking cycle to bring inflation back toward its 2% target reinforced its independence, and long-run inflation expectations have stayed anchored (Bank of Canada).

- Political stability. Canada scores around the 90th percentile on the World Bank's governance sub-indices for control of corruption, government effectiveness, and accountability.

There is a cost, though. Because gross debt is high, Canada's public debt-servicing burden runs hotter than its AAA peers. Government interest payments consumed roughly 7% of revenue in 2022, the highest among AAA countries, although still well below the 12% median across the lower AA tier.

Why does Canada's credit rating matter to you?

Canada's sovereign rating matters to you because it helps set the price of nearly all borrowing in the economy, including your mortgage, car loan, and line of credit. Government bonds are treated as the "risk-free" benchmark, and almost every other interest rate is quoted as a spread on top of that benchmark. If a downgrade pushed the government's own borrowing costs up, those higher rates would tend to ripple outward and lift household and business borrowing rates alongside them, tightening financial conditions (RBC Economics).

The rating also reaches down to the provinces. Provincial credit ratings tend to move with the sovereign rating, and more than half of Canada's total general government debt is held by provincial governments, the highest such share among AAA economies. When Fitch cut the national rating in 2020, most provinces were not downgraded immediately, but British Columbia was placed on negative watch and then downgraded the following year.

For a Canadian household, the practical takeaways are simple:

- A strong sovereign rating helps keep the base rates behind your mortgage and loans lower than they would be otherwise.

- The rating is not something you can act on directly; your own credit score is what determines the rate you personally qualify for.

- Watching the sovereign rating is useful for understanding the direction of borrowing costs, not for predicting your individual loan approval.

Is Canada's credit rating at risk in 2026?

Canada's rating is stable at all four agencies as of 2026, but Fitch has flagged rising debt as a medium-term pressure that could weigh on the rating if it continues. After the November 2025 federal budget, Fitch noted that "persistent fiscal expansion and a rising debt burden have weakened its credit profile and could increase rating pressure over the medium term," while keeping the AA+/stable rating in place (Fitch Ratings).

The numbers behind that caution are concrete. Fitch projects Canada's general government debt-to-GDP ratio will climb from 88.6% in 2024 to 91.8% in 2026 and 98.5% in 2027, close to double the 49.6% median for AA-rated countries. A stable outlook means no change is expected in the near term, so a warning is not a downgrade. It signals the metrics agencies watch most closely are trending the wrong way.

For context, Canada is still in a stronger position than many peers. It is one of only a handful of countries that keeps a AAA rating from at least two of the top global agencies, and it fared better than the United States, which lost its last top-tier rating when Fitch cut it to AA+ in August 2023.

The bottom line

Canada's sovereign credit rating is AAA at Moody's, S&P Global, and DBRS Morningstar, and AA+ at Fitch, all with a stable outlook. That top-tier standing rests on manageable net debt, a credible central bank, and strong institutions, and it helps anchor the base interest rates behind everyday borrowing. If you were actually looking for your own credit rating, that is a separate 300-to-900 personal score set by Equifax and TransUnion, and the fastest way to improve it is to understand how it is calculated.

At Sphera Credit, we build AI systems that read a borrower's full credit picture with the same rigour a rating agency applies to a country, so lenders can make accurate, explainable decisions on the applicants who fall outside a simple score cutoff.