How do you better your credit score?

You better your credit score by paying every bill on time, keeping your reported credit card balance below 30% of the limit, leaving old accounts open, and spacing out new credit applications. These four behaviours feed the factors that Canadian scoring models weigh most heavily, according to the Financial Consumer Agency of Canada and Equifax Canada.

A credit score in Canada is a number from 300 to 900 that Equifax Canada and TransUnion Canada calculate from your credit report. Both models reward the same five inputs, so every effective tactic maps to one of them:

| Action | Factor it moves | Approximate weight | Typical time to first effect |

|---|---|---|---|

| Pay at least the minimum on time, every account | Payment history | ~35% | 1 to 2 statement cycles; gains compound over 6 to 12 months |

| Pay card balances down before the statement closing date | Utilization (amounts owed) | ~30% | 30 to 60 days |

| Keep your oldest no-fee card open and active | Length of credit history | ~15% | Ongoing; protects existing gains |

| Hold both revolving and installment credit | Credit mix | ~10% | Several months |

| Apply for new credit rarely, and cluster rate shopping | New credit (inquiries) | ~10% | Inquiries fade over 3 to 12 months |

Payment history is the record of every on-time, late, or missed payment on your file. It carries the most weight, which is why a single skipped payment undoes months of careful utilization work. If money is tight, the FCAC's guidance is direct: make at least the minimum payment, and contact the lender before you miss a bill, not after.

Credit utilization is your reported balance divided by your credit limit. The FCAC recommends staying under 30% of your total available credit. The section below on the 90-day plan shows why the word "reported" matters more than most people think.

How do you see your credit score in Canada?

You can check your credit report for free from both Equifax Canada and TransUnion Canada, and checking never lowers your score. Free score access is also available through bank apps and services like Borrowell and Credit Karma, which use soft inquiries: checks that only you can see. Reviewing both reports first is the right opening move, because a surprise error or an account you don't recognize can be disputed at no cost, and a successful dispute often does more than any repayment tactic. Our guide to checking your credit score in Canada walks through each access route.

What does a 90-day credit improvement plan look like?

A realistic 90-day plan attacks the two heaviest factors in order: automate payments so nothing is ever late, then cut the balance the bureaus actually see below 30% of your limit, one statement at a time. Here is the arithmetic for a concrete case: one card with a $6,000 limit carrying a $3,300 balance, which is 55% utilization, plus one 30-day late payment from last year.

- Days 1 to 7: stop new damage. Set up pre-authorized minimum payments on every account so payment history only accumulates positives. Find your card's statement closing date (the day the balance is reported, not the payment due date) on your statement or app.

- Days 1 to 30: first utilization cut. Pay $1,650 before the statement closes. The bureaus now see $1,650 on a $6,000 limit: 28% utilization, under the FCAC's 30% line for the first time.

- Days 31 to 60: second cut. Pay the balance down to $550 before the next close. Reported utilization drops to 9%. Utilization has no memory in Canadian scoring models, so the improvement registers as soon as the lower balance is reported.

- Days 61 to 90: lock the structure. Keep the old card open (its age supports your file), keep the balance under 10%, and apply for nothing. If your issuer offers a credit limit increase without a hard inquiry, accepting it lowers utilization further: the same $550 on an $8,000 limit is 7%.

The late payment from last year keeps fading as new on-time months stack on top of it, and it disappears entirely 6 years after the miss under Canadian reporting rules (Equifax Canada).

What this plan deliberately avoids: applying for new credit. Each application creates a hard inquiry, which can trim a few points and stays visible on your report. The FCAC notes one exception worth using: when you shop for a car loan or mortgage, quotes gathered within a two-week window count as a single inquiry, so comparison shopping is not penalized.

Which credit score myths actually slow you down?

The three most expensive myths are paying in full and assuming your utilization is zero, carrying a balance to build credit, and closing old cards to clean up your file. Each one fails because of how reporting actually works, not because the intention is wrong.

- Myth 1: "I pay in full every month, so my utilization is zero." The bureaus receive your statement balance: the amount owing on the day the statement closes, before your payment arrives. Spend $2,700 on a $3,000-limit card and pay it in full a week later, and your file still shows 90% utilization. The FCAC flags this directly: heavy use of available credit can mark you as higher risk even when you pay in full. The fix costs nothing: pay most of the balance a few days before the close, then pay the remainder by the due date.

- Myth 2: "Carry a small balance so the card reports activity." Interest-bearing balances build nothing. Scoring models reward on-time payments and low reported balances; they do not distinguish a card paid in full from a card carrying $50 at 21% interest, except that the second one costs you money. A card used for one small purchase and paid on time gives the model everything it needs.

- Myth 3: "Close the cards you no longer use." Closing an old card usually hurts twice. Your total available credit shrinks, which raises utilization on every remaining balance, and your average account age eventually falls. The FCAC recommends keeping an older no-fee account open with occasional activity. Closing makes sense mainly when an annual fee outweighs the scoring benefit.

The pattern behind all three myths is the same: the score reacts to what lenders report, on the dates they report it, not to your intentions between statements.

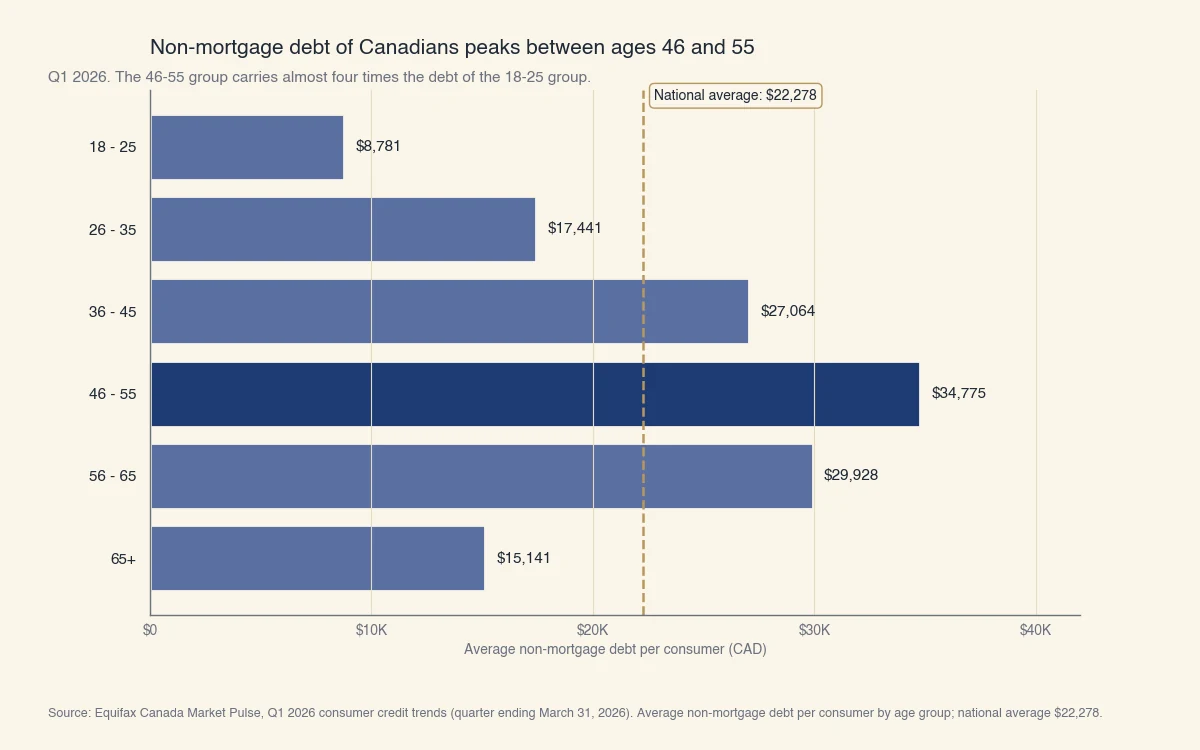

How much non-mortgage debt do Canadians carry at your age?

The average Canadian held $22,278 in non-mortgage debt in Q1 2026, and the load peaks between ages 46 and 55 at $34,775, according to Equifax Canada's Market Pulse report. Knowing where you stand against your age group puts a utilization target in context: the debt you carry relative to your limits, not the dollar amount itself, is what the score reacts to.

Source: Equifax Canada Market Pulse, Q1 2026 consumer credit trends. Average non-mortgage debt per consumer by age group.

Two details from the same report sharpen the picture. About 1.5 million Canadians, roughly 1 in 21 credit users, missed at least one payment in Q1 2026, and consumers aged 65 and over paid off their full card balance 62.6% of the time, the highest of any group. The behaviours that better a score are the same ones the lowest-delinquency groups already practice: balances paid down, limits used lightly, payments never missed.

If your debt sits well above your age group's average and minimum payments are a struggle, the highest-value move may be structural rather than tactical: a lower-rate consolidation or a repayment plan changes the inputs the score reads. What counts as a good credit score in Canada also varies by lender, so a mid-tier score often qualifies for more than people assume.

How do you build a credit score from zero?

If you have no credit history, you build a score by opening one reportable product, using it lightly, and letting on-time months accumulate: a secured credit card is the standard starting point in Canada. A secured credit card is backed by a refundable deposit that typically sets the limit, which is why issuers accept applicants with no file. Newcomers to Canada, students, and anyone rebuilding after insolvency follow the same path:

- Open a secured card (or ask your bank about a low-limit starter card) and confirm it reports to both Equifax and TransUnion.

- Put one small recurring bill on it, such as a phone plan, and automate full payment.

- Keep the reported balance under 30% of the limit, even if the limit is only $500.

- After 6 to 12 months of clean history, a standard unsecured card or a small installment product adds mix without hurting the file.

Time does the rest. Length of credit history rewards patience, and there is no shortcut that substitutes for months of on-time reporting. The full set of starter options, including credit-builder programs and rent reporting, is covered in our guide to building a credit rating in Canada.

A thin file is not a bad file. Lenders read "no history" and "bad history" very differently, and six months of clean reporting on one small product is often enough to move from unscoreable to the mid-600s.