Can medical bills affect your credit rating in Canada?

Yes, but only if a bill goes unpaid and is sent to a collection agency. A medical bill on its own never touches your credit rating, because Canadian doctors, dentists, hospitals, and pharmacies are not credit grantors and do not report to Equifax Canada or TransUnion Canada. The bill becomes a credit problem only when you leave it unpaid, the provider gives up collecting it directly, and it is assigned to a collection agency, a company that buys or is hired to recover overdue debts and does report to the bureaus (FCAC).

That single distinction is the whole answer, and it is also where every US-based article gets Canada wrong. The pages that rank for this question describe a $500 reporting threshold, a 365-day grace period, and state bans on medical debt in credit files. None of those rules exist in Canada. This page answers the question for the Canadian system: how a bill actually reaches your file, which health costs Canadians pay out of pocket (with Statistics Canada figures), one bill walked from invoice to collection with real numbers, and why the American rules do not protect you.

The 30-second version

- A medical bill you pay, or settle with the provider: never reported, no effect on your rating.

- A bill paid with a credit card: a normal card purchase, harmless unless you miss the card payment.

- An unpaid bill still with the clinic or hospital: not yet on your credit report.

- An unpaid bill sent to a collection agency: this is the event that damages your rating, and it stays six years.

How does an unpaid medical bill reach your credit report?

An unpaid medical bill reaches your credit report through one path only: the provider sends it to a collection agency, and the agency reports a collection account to the bureaus, where it usually appears rated 9, the worst status on the Canadian R-scale. Nothing about the original invoice is on your file. The reporting party is the collection agency, not the clinic.

Here is where each event in the life of a medical bill lands.

| Medical-bill event | Reported to Equifax / TransUnion? | Typical credit impact | How long it lingers |

|---|---|---|---|

| Receiving a bill from a clinic, dentist, or hospital | No | None | Not applicable |

| Paying the bill by its due date | No | None | Not applicable |

| Paying the bill with a credit card | Only your card is reported, not the bill | None if you pay the card | Normal card history |

| A bill that is late but still with the provider | No | None yet | Not applicable |

| An unpaid bill sent to a collection agency | Yes, as a collection account | Severe drop, rated 9 | 6 years from first delinquency |

| A missed credit card payment because you paid a medical bill instead | Yes, reported by the card issuer | 30-day late mark or worse | 6 years from the missed payment |

The pattern mirrors every other kind of Canadian debt: the invoice is invisible to lenders, and only a default that turns into a reported collection becomes a credit event.

How a medical collection is coded on a Canadian file

When a collection lands on your report, it carries a rating code. Equifax Canada pairs a letter with a number: the letter is the account type and the number is the payment status. R is revolving credit, I is an installment loan, and O is open credit; the number runs from 1 (paid as agreed) to 9 (written off as bad debt or placed for collection) (Equifax Canada Consumer Credit Report User Guide). A medical collection typically shows as a 9. If you want the full breakdown of how these codes are built, our guide on how credit ratings are calculated walks through the R-scale in detail.

That 9-rated entry stays on your Equifax Canada and TransUnion Canada files for six years from the date of first delinquency, the date the account first went overdue and was never brought current. Paying it later does not reset the clock (Equifax Canada).

Which medical bills do Canadians actually pay out of pocket?

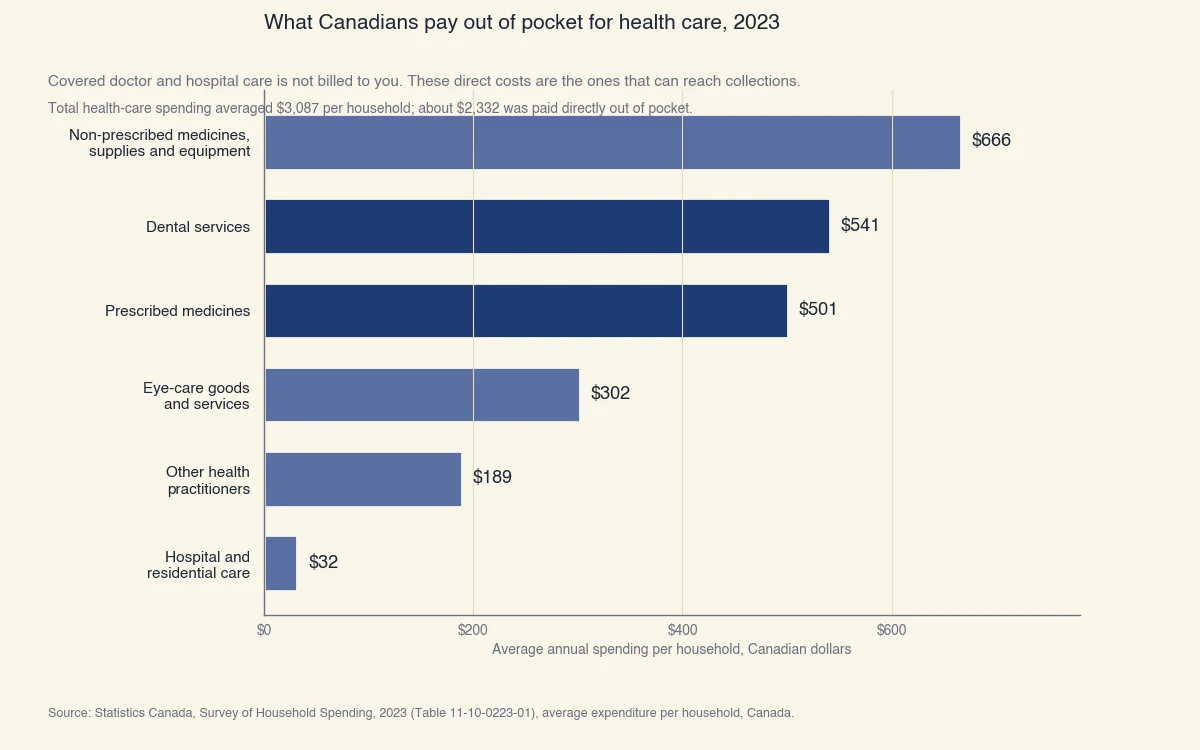

Because provincial health insurance covers medically necessary doctor and hospital care, the bills that can reach a Canadian's credit file are the ones public plans do not cover: dental work, prescription and non-prescription drugs, health supplies, eye care, and other practitioners. In 2023, the average Canadian household spent $3,087 on health care, of which about $2,332 was paid directly out of pocket rather than through insurance premiums (Statistics Canada).

Those direct costs are exactly the invoices that can be left unpaid and sent to collections. The chart below breaks down where the money goes.

Source: Statistics Canada, Survey of Household Spending, 2023 (Table 11-10-0223-01), average expenditure per household, Canada.

Dental services ($541) and drugs ($501 prescribed, plus $666 in non-prescribed medicines and supplies) are the largest direct costs, which is why a dental invoice or a pharmacy balance is the medical bill most likely to end up in collections. Household health spending also rose 11.2% from 2021 to 2023, faster than general inflation, so more Canadians are carrying larger out-of-pocket balances than a few years ago (Statistics Canada).

A worked example: one unpaid dental bill from invoice to collection

The realistic worst case is a routine dental bill you dispute or forget, which ages past the provider's patience, gets assigned to a collection agency after about 90 days, and drops a good score by 60 to 130 points when it posts as a 9-rated collection. Here is the full chain with numbers.

Imagine Maxime, a 29-year-old in Sherbrooke with an Equifax Canada score of 715. A crown that his group insurance only partly covers leaves him a $541 balance, the 2023 national average for dental services.

- Day 0 to Day 30. Maxime receives the $541 invoice. He believes his insurer should have paid more and sets it aside to argue later. Nothing is on his credit file. His score is still 715.

- Day 31 to Day 90. The clinic sends two reminders. Maxime keeps meaning to call. The bill is overdue, but it is still with the dentist, so no bureau sees it. His score is still 715.

- Day 91 onward. The clinic gives up and assigns the $541 to a collection agency. The agency reports a 9-rated collection to Equifax Canada. A single collection on a previously healthy file commonly costs 60 to 130 points, so Maxime's 715 falls to roughly 610. A sudden drop like this is one of the most common reasons a credit score falls.

- The six-year tail. Even after Maxime pays the $541, the collection stays on his file for six years from that first delinquency (Equifax Canada).

Run the same story with one change. If Maxime had called the clinic in the first month and either paid the $541 or agreed to a payment plan, the bill would never have reached a collection agency and his rating would never have moved. The entire difference between a non-event and a six-year mark is whether the bill is resolved before it is assigned to collections. Because that collection also shows up when he next applies to borrow, it can raise his rate or sink an application, the same lending consequences covered in our guide on getting a mortgage with an R7 rating.

Canada versus the United States: why the US rules do not apply to you

Almost every article that ranks for this question describes American rules that have no force in Canada. There is no $500 medical-debt floor, no national 365-day grace period before reporting, and no provincial equivalent of the US state bans on medical debt in credit files. A Canadian who trusts the top US search results will draw the wrong conclusions.

| Rule | United States | Canada |

|---|---|---|

| Sub-$500 medical debt kept off reports | Yes, since 2023 | No such threshold |

| Paid medical collections removed | Yes, since 2022 | No, a paid collection stays 6 years |

| National grace period before reporting | 365 days | No fixed national rule; set by provider and agency |

| Blanket ban on medical debt in credit files | A 2025 federal rule was vacated by a court in July 2025; some states ban it | No ban; a medical collection is treated like any other |

| Who reports the debt | Collection agency (providers rarely report) | Collection agency (providers are not credit grantors) |

The one point both systems share is the most important: in neither country does the original medical provider usually report to the bureaus. The damage comes from the collection agency. The difference is that Canada gives you no automatic dollar threshold and no removal-on-payment relief, so preventing the hand-off to collections matters more here, not less.

How to keep a medical bill from ever hurting your credit

Resolve the bill before it can be assigned to a collection agency, and the question of credit impact never arises. A short checklist keeps every medical bill in the invisible column.

- Open the envelope. Most medical collections start as a bill someone set aside. Read it and diarize the due date the day it arrives.

- Contest it with the provider first, in writing. If an insurer should have paid, dispute the charge with the clinic and your insurer while the bill is still with the provider, not after it reaches an agency.

- Ask for a payment plan. Clinics, dentists, and hospitals routinely accept installments. A plan you are keeping is not a default and is not reported.

- Do not ignore a collection call, but know your rights. Collection agencies in Canada must follow provincial rules on how and when they can contact you (FCAC).

- Dispute an inaccurate collection. If a medical collection is not yours, is the wrong amount, or was already paid, file a dispute with Equifax Canada and TransUnion Canada. The bureau must investigate and correct genuine errors.

- Use new public coverage to shrink the exposure. The federal Canadian Dental Care Plan now covers eligible residents for many dental services, and national pharmacare is expanding drug coverage, which reduces the dental and drug bills that most often become collections (Government of Canada).

If you are not sure whether an old medical bill ever reached your file, request your free Equifax Canada or TransUnion Canada report and read the collections section. Our guide on how to check your credit score in Canada shows where to get it, and if a collection did land, how to increase your credit score covers the rebuild. Checking your own report is a soft pull and never lowers your rating (FCAC).