When is the next Fed interest rate decision?

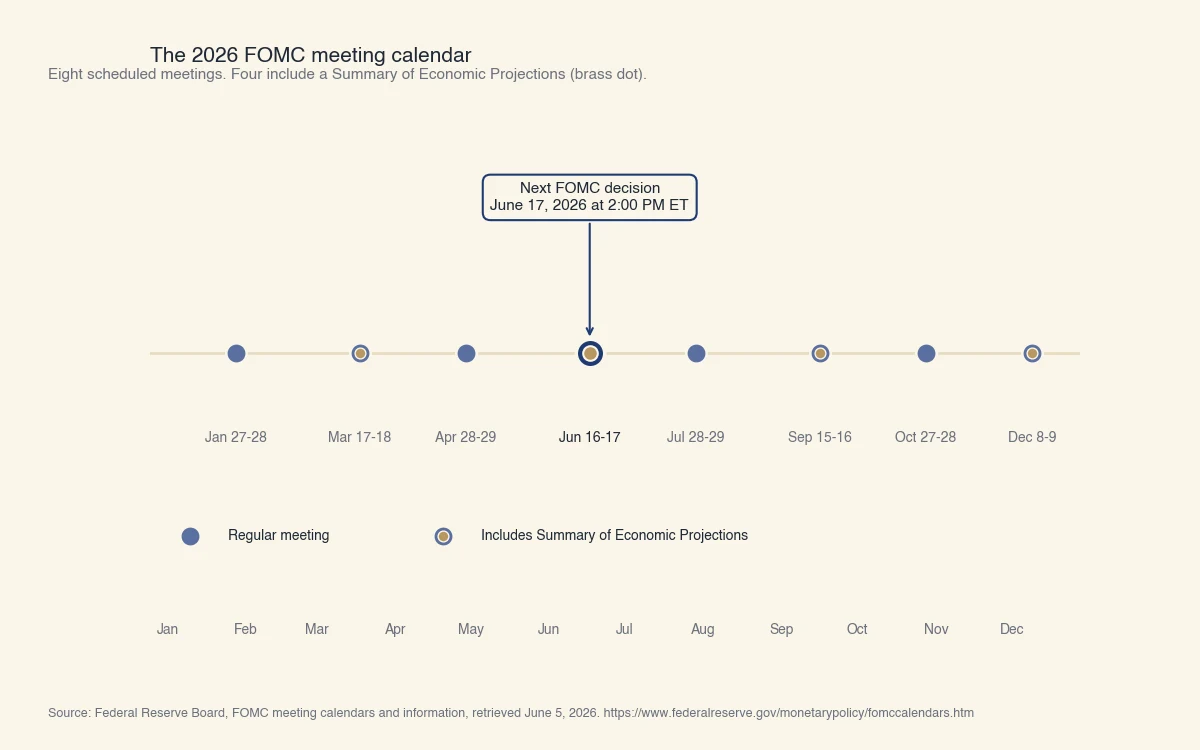

The next Federal Reserve interest rate decision is scheduled for Wednesday, June 17, 2026, at 2:00 PM Eastern Time, on the second day of the Federal Open Market Committee meeting. The June meeting is one of four 2026 meetings that include a Summary of Economic Projections (Federal Reserve). Those projections are the Fed's own answer to whether interest rates are expected to go down.

The current federal funds target range is 3.50% to 3.75%, held steady at the April 28-29, 2026 meeting. The federal funds target range is the band the FOMC sets for the overnight rate at which US banks lend reserves to each other, and it anchors almost every other US short-term rate. That target is quoted as a nominal interest rate, the stated rate before any adjustment for inflation.

The full 2026 FOMC meeting calendar

The eight scheduled FOMC meetings for 2026 are public and posted on federalreserve.gov:

| Meeting dates | Summary of Economic Projections | Press conference |

|---|---|---|

| January 27 - 28 | No | Yes |

| March 17 - 18 | Yes | Yes |

| April 28 - 29 | No | Yes |

| June 16 - 17 | Yes | Yes |

| July 28 - 29 | No | Yes |

| September 15 - 16 | Yes | Yes |

| October 27 - 28 | No | Yes |

| December 8 - 9 | Yes | Yes |

Every regularly scheduled meeting in 2026 includes a Chair press conference at 2:30 PM ET on the second day. Meeting dates are technically tentative until confirmed at the immediately preceding meeting, but the Fed has not moved a date in over a decade.

Source: Federal Reserve Board, FOMC meeting calendars and information, retrieved June 5, 2026.

What a 25-basis-point Fed move means for your loans

A 25-basis-point change in the federal funds target range moves the WSJ prime rate by the same 25 basis points within hours, which immediately changes the interest you accrue on a HELOC and a credit card, but only changes a new mortgage rate indirectly through Treasury yields. Here is what that looks like in dollars on three common consumer loans.

The arithmetic uses the current 3.50 to 3.75% target range, the corresponding WSJ Prime of 7.50% as of June 5, 2026, and standard amortization formulas published by the Federal Reserve and Freddie Mac.

A $300,000 30-year fixed mortgage already locked

A fixed mortgage rate is locked at origination. A Fed cut or hike at the next meeting does not change your monthly payment by a single dollar. What does change is the refinance math: a 25 basis point drop in newly originated 30-year rates (from, say, 6.75% to 6.50%) cuts the monthly payment on a fresh $300,000 loan from approximately $1,946 to $1,896, a $50/month or $600/year savings. That savings has to clear closing costs (typically $4,000 to $8,000 on a $300,000 refinance) before a refinance pays off, so a 25 bp move alone rarely justifies refinancing.

A $20,000 HELOC at WSJ Prime + 1%

A home equity line of credit (HELOC) is a revolving loan secured by your home, with an interest rate that resets each statement to WSJ Prime plus a margin set in your contract (CFPB). At Prime 7.50% + 1.00% = 8.50% APR, the monthly interest accrual on a $20,000 balance is roughly $142.

If the Fed cuts 25 bp at the June meeting, WSJ Prime drops to 7.25% the same afternoon, your HELOC rate falls to 8.25%, and the next statement's interest accrual on the same $20,000 balance drops to roughly $138, saving $4 per month or $48 per year. If the Fed hikes 25 bp instead, accrual rises by the same amount in the opposite direction.

A $5,000 credit card balance at Prime + 16%

Most variable-rate credit cards in the US are also indexed to WSJ Prime, with much wider margins, typically Prime + 11% to Prime + 22% for consumer cards. At Prime 7.50% + 16.00% = 23.50% APR, a revolving $5,000 balance accrues roughly $98 of interest per month.

A 25 bp Fed cut drops the card APR to 23.25% and the monthly interest accrual to roughly $97, saving about $1 per month. A 25 bp hike adds about $1. The headline-grabbing Fed move is barely visible on the credit card. The variable to actually watch is the size of the balance, not the rate.

Why the three loans react differently

The three transmission channels are different:

- Fixed mortgages track the 10-year Treasury yield, not the federal funds rate. Treasury yields move on inflation expectations, not directly on FOMC decisions.

- HELOCs and variable credit cards are contractually indexed to WSJ Prime, which tracks the federal funds rate one-for-one. The pass-through is immediate.

- Auto loans and personal loans typically use a fixed rate set at origination, so they behave like the mortgage example for borrowers already in a contract.

Why the FOMC date may not be the date your mortgage rate actually moves

The market embeds its expectation of the next Fed decision into bond and futures prices weeks in advance, so 30-year mortgage rates often move on the data releases that shift those expectations (CPI, jobs reports), not on the FOMC announcement itself. This is the part of Fed-watching that consumer guides routinely skip.

The mechanism: 30-year fixed mortgage pricing tracks the 10-year US Treasury yield with a relatively stable spread. The 10-year Treasury reflects the market's view of average short-term rates over the coming decade, which depends on the path of inflation and Fed policy. By the time the Fed actually announces a decision at 2:00 PM ET, the median market participant already expects that outcome and has priced it in.

Where the market reads the expectation

The clearest read is the CME FedWatch tool, which converts 30-Day Fed Funds futures prices into the implied probability of each possible decision at the next FOMC meeting (CME Group). If FedWatch shows a 90% probability of a hold and the Fed holds, mortgage rates barely move at the announcement, because there is no new information. If FedWatch shows a 60% probability of a cut and the Fed instead holds, mortgage rates can move sharply within seconds.

The data calendar that actually moves rates

For a household timing a mortgage lock, the underlying data release calendar often matters more than the FOMC calendar:

- CPI release (second Wednesday or Thursday of each month, 8:30 AM ET) shifts inflation expectations and 10-year Treasury yields.

- Employment Situation report / Non-Farm Payrolls (first Friday of each month, 8:30 AM ET) shifts growth expectations and Fed rate-path expectations.

- PCE Price Index (released near the end of each month, 8:30 AM ET) is the Fed's preferred inflation gauge.

A Freddie Mac Primary Mortgage Market Survey reading in the days after a CPI surprise often moves more than the same survey in the days after an FOMC meeting that held to expectations (Freddie Mac).

What this means for timing a loan

If the goal is to lock a mortgage rate near a local low, the practical implications are:

- Watch CME FedWatch in the two weeks before the FOMC meeting. The probability you see there is roughly the probability already in your rate quote.

- Watch CPI and NFP release dates between FOMC meetings. Those are the days mortgage rates are most likely to move.

- Treat the FOMC announcement as a confirmation event for variable-rate products (HELOC, credit card) and as a non-event for an already-locked fixed mortgage.

How a Fed decision becomes your loan rate

The transmission from a Federal Reserve decision to a household interest rate runs through three distinct channels with three different timelines: WSJ Prime resets within hours, variable consumer loan rates reset on the next billing cycle, and new mortgage rates reset continuously through Treasury markets.

The sequence on an FOMC announcement day:

- 2:00 PM ET: FOMC releases the statement and the updated target range. Fed funds futures, Treasury yields, and the dollar reprice within seconds.

- 2:00 to 4:00 PM ET: The largest US banks (JPMorgan Chase, Bank of America, Citi, Wells Fargo, US Bank, PNC, and others) update their internal prime rate.

- Same business day: The Wall Street Journal publishes the new WSJ Prime once at least 70% of the 10 largest banks have changed theirs (WSJ Money Rates).

- Next statement cycle: Variable-rate consumer products (HELOC, credit card) recompute interest at the new WSJ Prime plus the contractually fixed margin.

- Continuous: Newly originated fixed mortgages reprice through the 10-year Treasury channel. Existing fixed mortgages are not affected.

The Fed itself does not call your bank or your credit card issuer. The transmission happens because banks fund themselves at the federal funds rate, so a change in that rate changes their cost of money, which they pass to variable-rate products through the WSJ Prime index that almost every variable consumer contract references.

Where to verify the next decision date

The single authoritative source for the next Fed interest rate decision date is the FOMC calendar at federalreserve.gov. Every secondary source ultimately quotes that page.

The Fed posts the meeting calendar at federalreserve.gov/monetarypolicy/fomccalendars.htm. The page lists meeting dates for the current and following calendar year, indicates which meetings include a Summary of Economic Projections, and links the post-meeting statement after each decision is released. For market-implied probability of the next decision outcome, the CME FedWatch tool is the standard reference.

If a meeting date moves (which is rare), the change is confirmed at the meeting immediately preceding the affected one. Calendar applications and economic-event aggregators sometimes lag the official page by several weeks, so for a high-stakes decision (locking a HELOC draw, timing a refinance application), going directly to federalreserve.gov is the safer reference.