What is a nominal interest rate?

A nominal interest rate is the stated, advertised percentage that a lender charges or that a bank pays, before any adjustment for inflation, fees, or compounding. When a credit card statement shows 21.99%, a mortgage lock-in shows 6.53%, or a high-yield savings account advertises 4.65%, all three numbers are nominal rates (Federal Reserve).

The nominal rate is the number printed on contracts and ads. It is what borrowers agree to pay and what savers expect to earn in raw dollar terms. It does not tell you how much purchasing power you actually gain or lose, because it ignores three things: the inflation rate eroding the dollar, the compounding frequency expanding the dollar, and the tax owed on whatever is earned.

The relationship to the real rate was first formalized by economist Irving Fisher in 1907 and is taught today as the Fisher equation: nominal rate equals real rate plus expected inflation. The Federal Reserve Bank of San Francisco describes the intuition this way: the nominal rate measures the percentage increase in the dollars a lender receives, while the real rate measures the percentage increase in the purchasing power those dollars buy (San Francisco Fed).

Where the nominal rate fits among the rates you see on paperwork

Lenders and banks quote four numbers that sound similar and mean different things:

| Term | What it adjusts for | Who uses it |

|---|---|---|

| Nominal rate | Nothing (raw quoted rate) | Bond markets, Fed Funds rate, sticker rates on signs |

| Real rate | Inflation | Economists, retirement planners, FRED time series |

| APR (Annual Percentage Rate) | Certain mandatory fees, by law | US closed-end consumer loans under Regulation Z |

| APY (Annual Percentage Yield) | Compounding frequency | US deposit accounts under Regulation DD |

The same loan can have a nominal rate of 6.50%, an APR of 6.78% (with closing costs), and an effective rate of 6.70% (with monthly compounding). Each number answers a different question, so reading "the rate" without knowing which one is being quoted is a recurring source of confusion. The Consumer Financial Protection Bureau standardizes the APR disclosure under Regulation Z so US borrowers can at least compare loans on the same fee-adjusted basis (CFPB). For why that fee-adjusted figure differs from the rate itself, see whether APR is the same as the interest rate.

How does the nominal rate compare with the real and effective rates?

The nominal rate tells you the dollar return; the real rate tells you the purchasing-power return; the effective rate tells you the compounded return. Each adjustment fixes a different blind spot in the raw quoted rate.

The exact Fisher relationship is:

(1 + i) = (1 + r) × (1 + π)

where i is the nominal rate, r is the real rate, and π is the inflation rate. For most practical purposes, the approximation i ≈ r + π is accurate to within a tenth of a point when inflation is below 5%.

A worked Fisher example using the most recent US data:

- Nominal savings rate: 4.65% (typical high-yield savings APY as of May 2026)

- Headline CPI inflation: 3.8% over the 12 months ending April 2026 (BLS)

- Approximate real return: 4.65% − 3.8% = 0.85%

- Exact Fisher real return: (1.0465 / 1.038) − 1 = 0.82%

A saver holding $10,000 at that rate keeps about $82 of real purchasing power per year, not the $465 implied by the nominal number alone. In a 24% federal marginal bracket, with state tax pushing the combined rate to roughly 30%, the after-tax-after-inflation return falls below zero: the saver actually loses real wealth despite earning a positive nominal yield.

The effective rate (also called the effective annual rate or EAR) adjusts for compounding rather than inflation. It answers the question: if I pay this nominal rate but interest accrues daily instead of yearly, what is my true annualized cost? The formula is EAR = (1 + i/m)^m − 1 where m is the number of compounding periods per year. A credit card advertising 21.99% APR with daily compounding produces an effective annual rate of about 24.6%, which is what a revolver carrying a balance actually pays each year. Most consumer-credit disclosures show the nominal APR; the effective rate is implied but rarely printed.

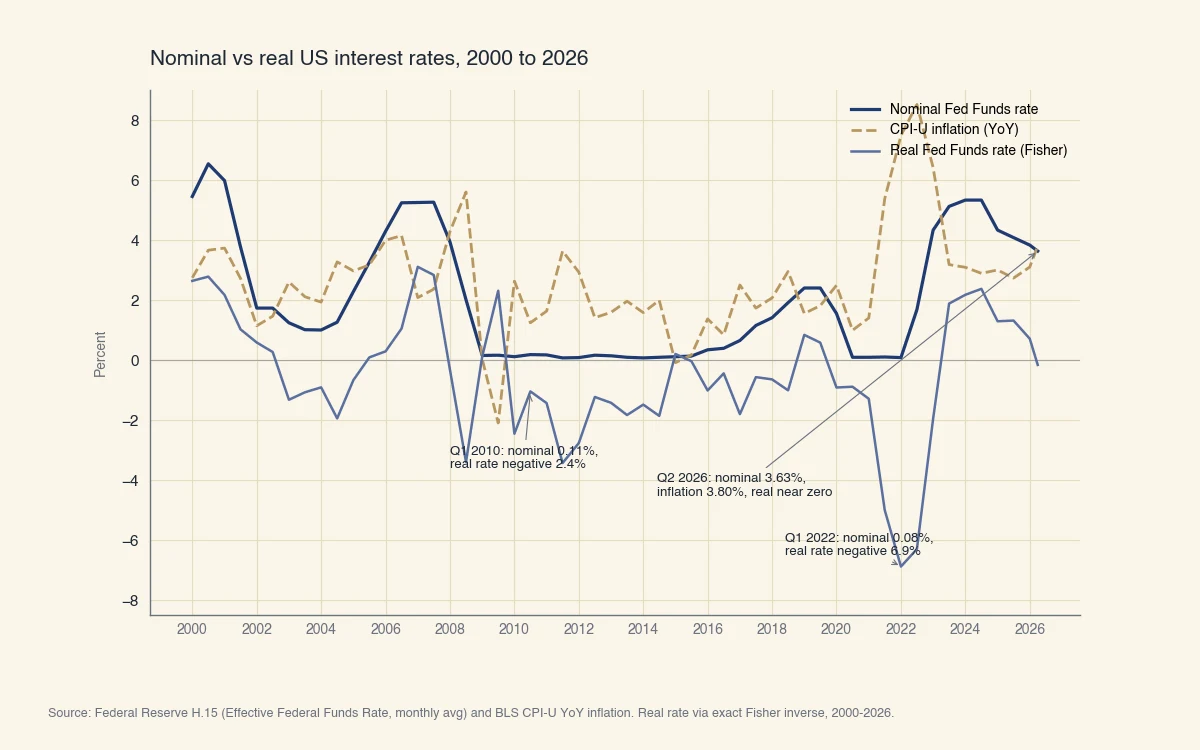

Source: Federal Reserve H.15 (Effective Federal Funds Rate, monthly avg) and BLS CPI-U YoY inflation. Real rate via exact Fisher inverse, 2000-2026.

The chart above shows why nominal rates can be deeply misleading on their own. The Federal Funds rate was 5.25% in 2007 and 0.25% in 2010, yet the real Fed Funds rate was higher in 2010 than in 2007 once inflation collapsed during the financial crisis. The reverse happened in 2022: the Fed raised the nominal rate aggressively, but real rates stayed negative until well into 2023 because CPI inflation ran ahead of nominal hikes.

How nominal rates affect what you actually pay or earn

On a real US mortgage, credit card, or savings account, the nominal rate sets the headline dollar amount, but the rate environment around it determines whether you come out ahead. The numbers below use the rate environment in effect as of June 2026.

Mortgage borrower: 30-year fixed at 6.53%

Freddie Mac's Primary Mortgage Market Survey reported a 30-year fixed-rate average of 6.53% for the week ending May 28, 2026 (Freddie Mac). On a $400,000 mortgage:

- Year one nominal interest paid: about $26,120

- Approximate real interest paid in 2026 dollars: $26,120 minus the 3.8% inflation gain on the borrower's debt, or about $10,920 in real terms

- Difference: inflation effectively transfers about $15,200 from lender to borrower in the first year

Mortgage borrowers benefit when realized inflation runs hotter than the rate the lender priced. This is why the same nominal mortgage rate feels expensive in a 1% inflation environment and cheap in a 5% inflation environment, even though the dollar payment is identical.

Credit-card revolver: 21.99% nominal APR

A $5,000 balance held all year at a 21.99% nominal APR compounded daily costs roughly:

- Nominal annual interest (simple): $1,100

- Effective annual interest (daily compounding): about $1,230

- The 2.6 percentage point spread between nominal APR and effective annual rate is structural, not a one-off

Credit-card APRs are nominal rates by regulatory definition. The CFPB requires disclosure of the APR on each statement under Regulation Z (CFPB), but card issuers compound daily, so the effective rate the consumer pays always exceeds the printed number. A consumer comparing two cards on advertised APR alone is comparing them on the right metric, but the dollars owed each month follow the effective rate.

High-yield saver: 4.65% nominal APY

Savings rates in 2026 are quoted as APY, which is already compounding-adjusted. The remaining adjustments are inflation and tax. A $25,000 savings account at 4.65% APY produces $1,163 of nominal interest the first year. After:

- 3.8% inflation: real interest of about $213

- 30% combined federal and state marginal tax on the nominal $1,163: $349 of tax owed

- Net after-tax-after-inflation outcome: a real loss of about $136 the first year

The IRS taxes the $1,163 of nominal interest reported on Form 1099-INT, not the $213 of real interest the saver actually earned (IRS Publication 550). This is mechanical, not a quirk of any specific bracket: in any environment where inflation plus marginal tax exceeds the nominal yield, after-tax real return goes negative.

Four things people get wrong about nominal interest rates

The most common errors come from treating the nominal rate as if it already accounted for inflation, compounding, or tax. Each one undercounts the true cost or overstates the true return.

1. A positive nominal rate means a positive return

Not necessarily. As the high-yield-saver example above shows, a 4.65% nominal yield can produce a negative real return once inflation and tax are applied. The 1970s in the US are the canonical case: 6-month Treasury bill nominal yields averaged 6.4% over the decade but real returns were negative more than half the time as inflation ran in double digits (San Francisco Fed). The fix is to compute the real rate every time you compare savings products.

2. Higher nominal rates always mean tighter monetary policy

Not necessarily. The Federal Reserve targets a nominal Federal Funds rate, but policy stance is judged on the real rate. The FOMC held the Federal Funds target range at 3.50% to 3.75% as of April 2026 (Federal Reserve). With headline CPI at 3.8%, the implied real Fed Funds rate is roughly zero, which most economists characterize as neutral, not restrictive. A nominal hike from 4% to 5% is contractionary only if expected inflation does not rise by the same amount.

3. The advertised rate and the rate you pay are the same

Not for any product that compounds more often than annually. A 6% nominal rate compounded monthly produces a 6.17% effective annual rate. A 10% nominal rate compounded monthly produces a 10.47% EAR. A 21.99% credit card APR compounded daily produces an EAR near 24.6%. The compounding rule is mechanical: EAR = (1 + i/m)^m − 1, with m equal to the number of compounding periods per year. For a saver, this works in your favor. For a credit-card revolver, it works against you.

4. Tax is owed on the real return

The IRS taxes the nominal interest your bank or broker reports on Form 1099-INT or 1099-OID, not the inflation-adjusted figure (IRS Publication 550). Two consequences:

- In a high-inflation environment, the after-tax real return on cash and short bonds can be deeply negative even when the after-tax nominal return is positive.

- Tax-advantaged accounts (401(k), IRA, Roth IRA) sidestep this by deferring or eliminating tax on the nominal amount. The real value of these accounts compounds untouched.

This is why financial planners treat inflation and tax as separate, sequential adjustments to the nominal yield, not as a single combined haircut. Skipping either step systematically misstates what a saver keeps.

Where the nominal rate sits in US monetary policy

The Federal Reserve sets the Federal Funds target range as a nominal rate, and every other US borrowing rate is built off it through the credit and term structure. The H.15 release publishes the daily effective Federal Funds rate, the prime rate, Treasury yields across the curve, and major bank deposit rates (Federal Reserve H.15). Mortgage rates track the 10-year Treasury yield plus a spread; credit-card APRs track the prime rate plus a margin set by the issuer; savings APYs track competition for deposits plus a margin pulled by Fed Funds.

The Federal Reserve does not set real rates directly. It moves the nominal Federal Funds rate, observes the inflation print, and infers the real stance after the fact. This is why FOMC statements lean so heavily on inflation expectations: the Committee is implicitly choosing a real-rate path through the nominal lever. Readers of the H.15 release can subtract any of the inflation series at BLS to back out the implied real rate at any maturity.